A Distributor in Surat Gave ₹18 Lakh in Year-End Discounts to 47 Dealers. His CA Said He Could Not Reduce GST on Any of It.

The discounts were real. The savings given to dealers were documented. The invoices were all there. But when the CA looked at the agreements, none of the year-end performance bonuses had been committed in writing before the original sales were made. No pre-agreement. No invoice linkage. Under Section 15(3)(b) of the CGST Act as it stood before 2026, those discounts could not reduce his output GST liability.

Result: ₹2.88 lakh in GST paid on discounts that were genuinely not income.

This has been the reality for manufacturers, brand owners, distributors, and retailers running dealer incentive programs in India for the past eight years. Volume bonuses decided at year-end. Scheme discounts announced mid-season. Cashback deals structured after sales were already booked. All of them blocked from reducing GST liability because of one rigid condition: the discount had to be pre-agreed before the supply.

Finance Act 2026 changed that condition. The 56th GST Council meeting recommended it. Parliament enacted it. The amendment to Section 15(3)(b) effective upon gazette notification removes the pre-agreement and invoice-linkage requirements entirely.

But removing that condition does not make everything automatic. The new rule comes with its own process, its own compliance risk, and one unchanged condition that, if missed, wipes out the entire tax benefit: the buyer must reverse the ITC attributable to the discount.

This guide covers what changed, what still applies, how to issue the credit note correctly, and what happens if your buyer does not reverse ITC.

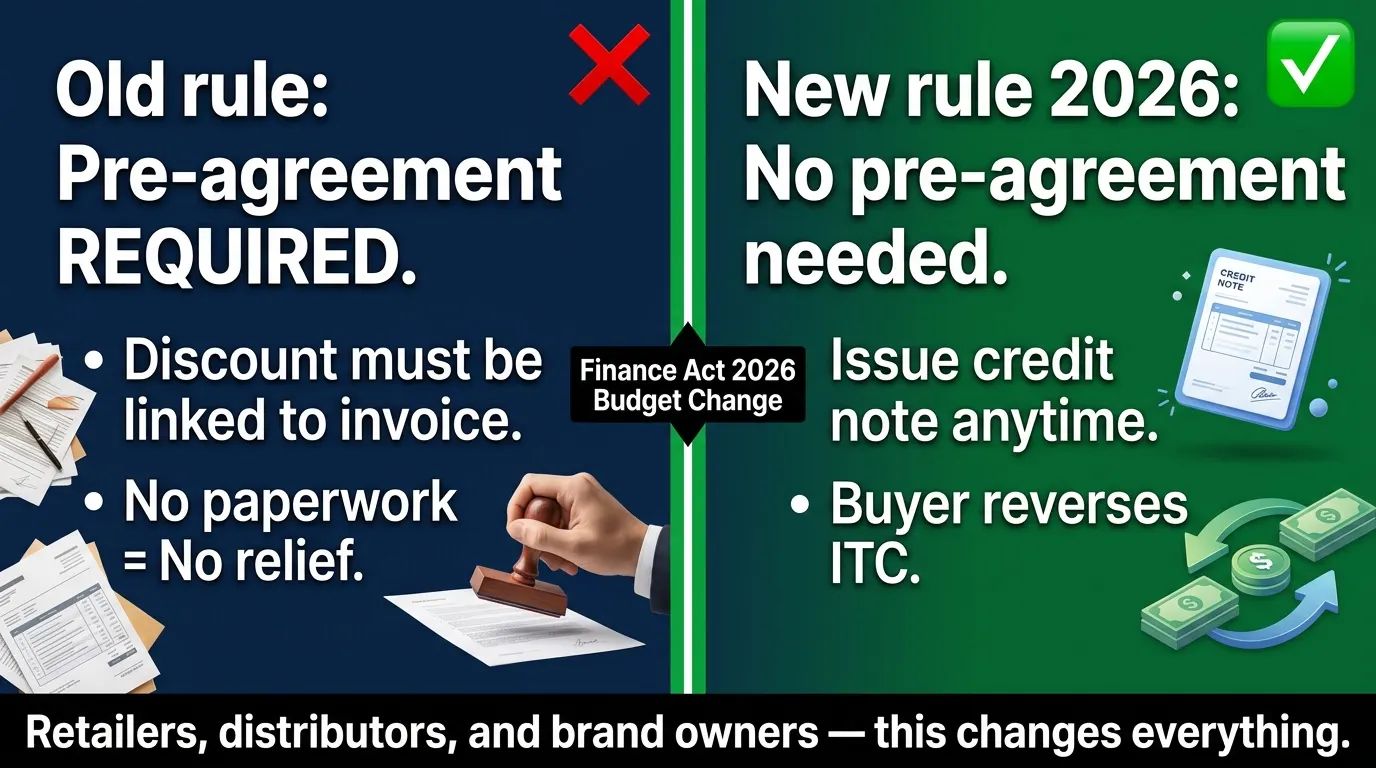

What Section 15(3)(b) Said Before Budget 2026 and Why It Created So Many Disputes

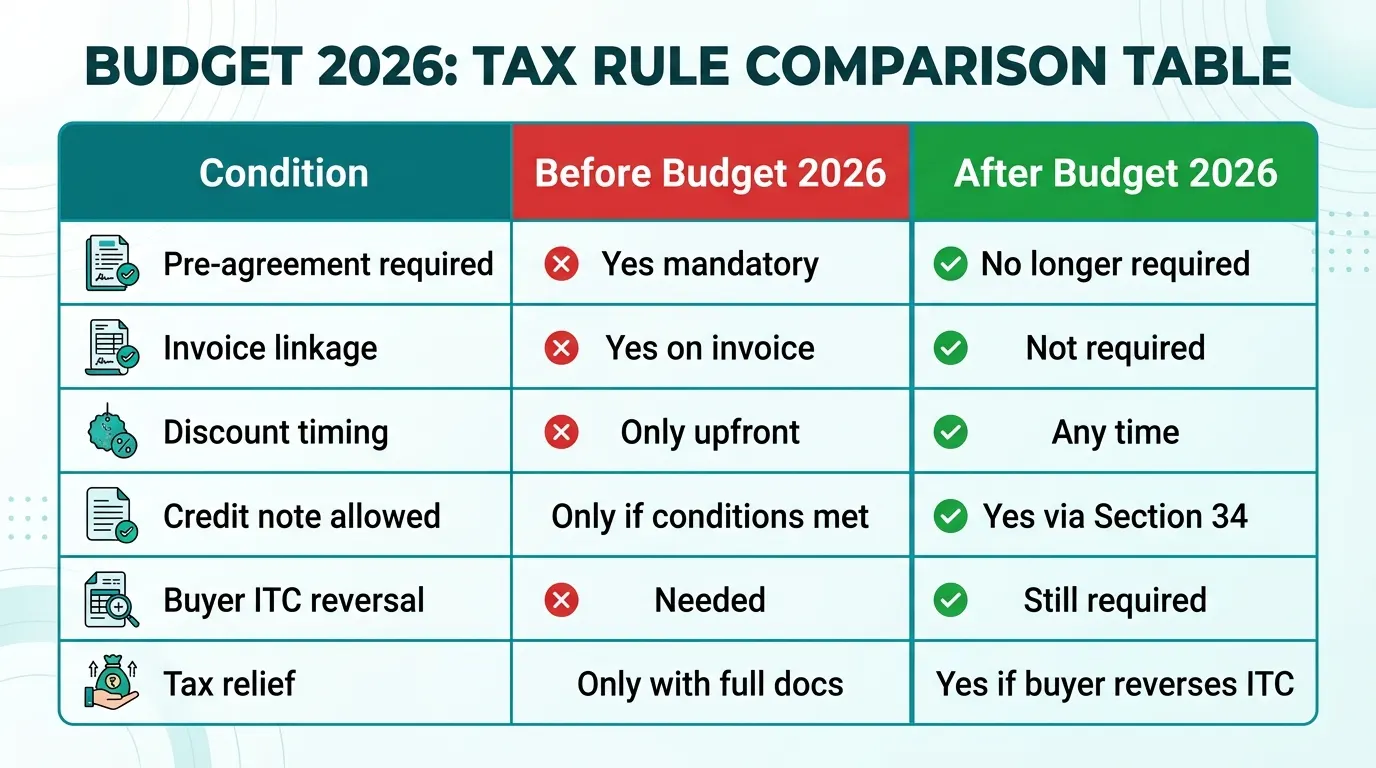

Under the original GST framework, post-sale discounts were governed by Section 15(3)(b) of the CGST Act. The section allowed a supplier to reduce the taxable value of supply for post-sale discounts but only if two conditions were both satisfied:

Condition 1➡️ Pre-existing agreement: The discount must have been established in an agreement entered into at or before the time of supply. A verbal commitment, an email after the sale, or a policy announced mid-year did not qualify.

Condition 2 ➡️ Invoice linkage: The discount must be specifically linked to relevant invoices. A blanket year-end discount across all purchases did not satisfy this condition easily because individual invoice-level linking was required.

These two conditions reflected a compliance philosophy from 2017 that assumed all commercial arrangements were pre-documented. In practice, that is not how trade works in India.

Manufacturers announce quarterly schemes after assessing market conditions. Distributors negotiate performance bonuses based on actual sales achieved. Brand owners design dealer incentive programs that depend on how much stock dealers actually move which can only be known after the fact. Linking each post-sale discount to pre-existing written agreements and specific invoice numbers created a documentation burden that most mid-market businesses simply could not sustain at volume.

The result: eight years of disputes. GST authorities routinely disallowed credit notes for post-sale discounts. Suppliers who issued credit notes anyway and reduced their output tax accordingly — faced demands, interest, and audit proceedings.

What Budget 2026 Changed The New Section 15(3)(b)

The 56th GST Council meeting in September 2025 recommended removing the pre-agreement requirement. Budget 2026, presented on February 1, 2026, gave effect to this recommendation through amendments to Section 15(3)(b) and Section 34(1) of the CGST Act via the Finance Act 2026.

The amended provision works as follows:

A post-sale discount can be excluded from the taxable value of supply meaning the supplier reduces their output GST liability if:

The supplier issues a valid GST credit note under Section 34 of the CGST Act within the permitted time period.

The recipient reverses the Input Tax Credit (ITC) attributable to the discount amount.

That is it. No pre-agreement required. No invoice-by-invoice linkage required.

A manufacturer can decide in March 2026 to give a 5% volume bonus on all purchases made by a dealer between April 2025 and March 2026, issue a credit note in March or April 2026, and reduce their output GST liability as long as the dealer reverses the proportionate ITC.

This change matters most for:

FMCG manufacturers and distributors running quarterly and annual scheme discounts

Electronics brands with performance-based dealer incentive programs

Retail chains giving retrospective trade discounts to suppliers

Any business where post-sale negotiations are a routine part of commercial relationships

What Has NOT Changed The Conditions That Still Apply

The removal of the pre-agreement requirement does not mean post-sale discounts under GST are now unrestricted. Two fundamental conditions remain, and one of them is more strictly enforced than the old pre-agreement rule ever was.

Condition 1 A Valid Credit Note Must Still Be Issued

You cannot reduce your output GST without a proper credit note. The credit note must comply with Section 34 of the CGST Act and Rule 53 of the CGST Rules:

Supplier's name, address, and GSTIN

Credit note serial number and date

Name, address, and GSTIN of the recipient

Original invoice number and date that this credit note relates to

Taxable value and the GST amount being reversed

Signature or digital signature

The credit note must be uploaded in your GSTR-1 in the month it is issued. Once uploaded, it reduces your output tax in that period.

Condition 2 The Buyer Must Reverse ITC (Non-Negotiable)

This condition existed before Budget 2026 and it exists after. It is now the central mechanism of the entire framework. Without ITC reversal by the buyer, the supplier's tax relief does not hold.

Under the amended framework, the credit note is linked to Section 34, and Section 34 requires recipient ITC reversal. If the buyer claims full ITC on the original supply and then does not reverse ITC when you issue the discount credit note, your reduction in output tax is technically not supported by the corresponding buyer-side compliance.

GST authorities can and in practice do scrutinise whether the buyer reversed ITC. If the buyer is large and audited, a mismatch between your credit note and their GSTR-3B ITC reversal is a live risk.

Condition 3 ➡️ Time Limit for Credit Notes

Credit notes under GST must be issued within the permitted time limit. Under Section 34 read with Section 16(4), the credit note must be issued before:

September 30 of the following financial year, or

The date of filing the annual return (GSTR-9) for that year

whichever is earlier.

So for a discount on a sale made in FY 2025-26, the credit note must be issued before September 30, 2026, or before you file GSTR-9 for FY 2025-26 whichever comes first.

Missing this window means the credit note cannot reduce your output GST liability. Issue credit notes promptly, not at year-end.

How to Issue the Credit Note Correctly Step by Step

Step 1: Confirm the discount amount with the buyer

Agree on the exact discount figure. Get written confirmation email is sufficient. This is now a commercial practice recommendation, not a legal requirement. But having it documented protects you in any future dispute with the GST department.

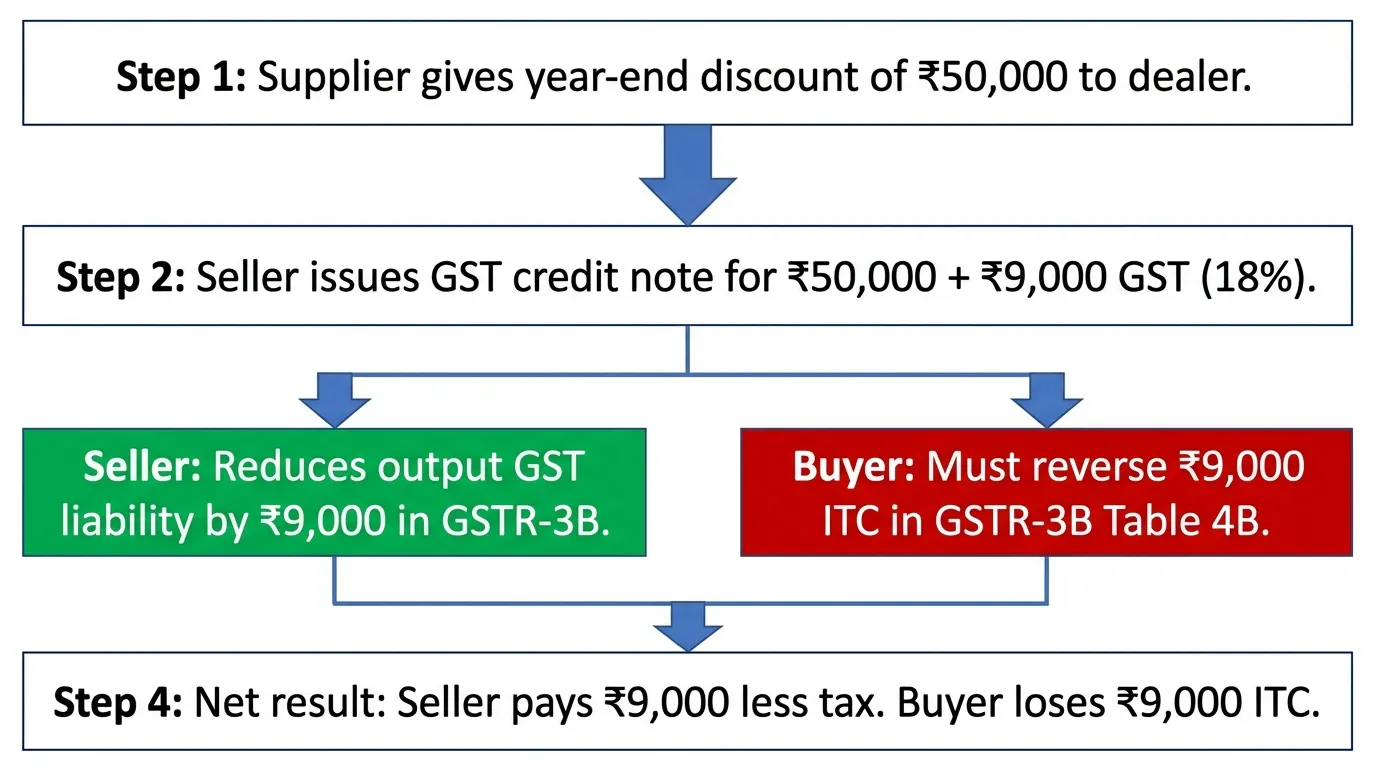

Step 2: Calculate the GST component on the discount

The credit note must show the base discount amount and the corresponding GST. Use the same rate that applied on the original supply.

Example:

Dealer bought goods worth ₹10 lakh + ₹1.8 lakh GST (18%) = ₹11.8 lakh total. You are giving a 5% year-end discount = ₹50,000 on base value. GST on discount = ₹50,000 × 18% = ₹9,000. Credit note shows: Base discount ₹50,000 + GST reversed ₹9,000 = ₹59,000 total.

Step 3: Issue the credit note with all mandatory fields

Include the original invoice references. If the discount spans multiple invoices, either reference all of them or state the period clearly (some practitioners reference the financial year in bulk discount credit notes check with your CA for current department guidance on format).

Step 4: Upload the credit note in GSTR-1

Report the credit note in your GSTR-1 for the period in which it is issued. The portal reduces your output tax for that period automatically.

Step 5: Confirm ITC reversal with the buyer

Follow up with your dealer or distributor to confirm they have reversed the ITC attributable to the discount in their GSTR-3B. Get a written confirmation or a copy of their GSTR-3B extract showing the reversal in Table 4B.

This step is not legally required for you to file but it protects you if the department asks for evidence that the framework was followed completely.

Use the SmartGST GSTIN Validator to verify your dealer's GSTIN is active before issuing the credit note. A credit note to an inactive GSTIN creates problems at the portal level.

GST vs Financial Credit Notes A Critical Distinction

Not every discount needs to be structured as a GST credit note. This distinction matters because the tax treatment is fundamentally different.

GST Credit Note (Tax Credit Note):

Issued under Section 34 of the CGST Act

Reduces the supplier's output GST liability

Requires the buyer to reverse proportionate ITC

Must be reported in GSTR-1 and flows into buyer's GSTR-2B

Example: Giving a ₹50,000 discount and reducing GST on it

Financial or Commercial Credit Note:

Issued under commercial practice, not under GST law

Does NOT reduce output GST liability

Buyer does NOT need to reverse ITC

Not reported in GSTR-1

Example: Giving a cashback or rebate where you absorb the discount without changing the GST amount on the original invoice

The choice between the two depends on your business intent and accounting treatment. If you want to reduce your output GST on the discount issue a GST credit note. If you are fine absorbing the cost and not adjusting the tax issue a financial credit note.

Many distributors running high-volume schemes find it simpler to issue financial credit notes (especially for small amounts), avoiding the ITC reversal coordination with multiple dealers. The tax cost is the GST on the discount absorbed which may be acceptable at small volumes but material at scale.

Evaluate this on a case-by-case basis for your scheme design. The SmartGST ITC Reversal Calculator helps you calculate the exact GST and ITC impact of each approach before you decide.

When the Buyer Does Not Reverse ITC The Risk You Must Manage

This is the real operational challenge with the new rule. The legal condition is clear: buyer must reverse ITC. The enforcement reality is that you the supplier cannot force your buyer to reverse ITC. You can only request and follow up.

What happens if the buyer receives your credit note, continues claiming full ITC, and does not reverse the attributable amount?

From a legal standpoint: the condition under Section 34 is not fully met. GST authorities can question your output tax reduction. If this comes up in an audit, the department may demand the reversed GST from you, plus interest.

From a practical standpoint: the IMS (Invoice Management System) now provides visibility. When you upload the credit note in GSTR-1, it appears in the buyer's IMS dashboard. The buyer must act on it accept or reject. If the buyer accepts the credit note in IMS, their GSTR-2B is automatically updated, and the system nudges them to reverse ITC in GSTR-3B.

This IMS linkage makes the reversal more trackable than before. But it does not make it automatic the buyer still has to file their GSTR-3B with the reversal.

For bulk dealer schemes, keep a register of credit notes issued and corresponding buyer ITC reversal confirmations. This is your audit defence document.

Read the SmartGST IMS Complete Guide to understand how credit notes flow through IMS and how buyers process them.

Industry-Wise Examples of How This Works Now

FMCG Manufacturer Running Quarterly Dealer Schemes

A soap manufacturer offers a 3% volume bonus to distributors who achieve ₹50 lakh in quarterly purchases. The bonus is announced at the start of the quarter but the exact amount depends on actual sales. Before Budget 2026: this structure was risky because the discount rate was stated upfront but invoice-level linkage across hundreds of invoices was impractical. After Budget 2026: issue a single credit note at quarter-end for the total bonus amount, reference the quarter, and ensure distributors reverse ITC. Full GST relief on the discount.

Electronics Brand Running Year-End Dealer Performance Bonuses

A TV brand gives dealers between 1% and 5% year-end bonus based on sales achievement. The bonus percentage is not known until March results are tallied. Before Budget 2026: no pre-agreement existed at the time of individual sales credit notes issued were routinely disputed. After Budget 2026: the brand can issue credit notes in March-April for the achievement amounts with no pre-agreement required. Dealers reverse ITC. Brand reduces output GST.

Retail Chain Renegotiating Supplier Margins Post-Season

A supermarket chain negotiates retrospective margin support from a supplier after assessing season performance. Before Budget 2026: the lack of pre-season written agreement made GST relief very difficult. After Budget 2026: supplier issues a credit note, chain reverses ITC, transaction is clean from a GST compliance standpoint.

Small Trader Giving Festival Discounts

A garment trader gives 10% festival discounts to B2B buyers after seeing competitor pricing. He had not committed to any specific discount in the original agreement. Before Budget 2026: these discounts were hard to take as GST-deductible without retroactive documentation. After Budget 2026: issue credit note, buyer reverses ITC, trader reduces output GST. Simple.

The Effective Date When Does This Apply?

The Finance Act 2026 received Presidential assent and was published in the Official Gazette in April 2026. However, Section 15(3)(b) amendment takes effect from a date to be separately notified by the Central Government through a gazette notification.

As of June 13, 2026, this specific effective date notification has not yet been published for Section 15(3)(b). The amendment has been enacted but is not yet in force.

This is an important point. Do not restructure your ongoing discount scheme documentation or withdraw pre-agreement practices until the effective date notification is published. Once it is notified, the new framework applies to credit notes issued on or after that date.

Watch the SmartGST Latest GST Updates page the effective date notification will be covered within 24 hours of CBIC publishing it.

Tools to Manage Your Credit Note Compliance

GSTR Mismatch Checker ➡️ After issuing credit notes, use this tool to verify your GSTR-1 credit note entries match your GSTR-3B output tax reduction before filing.

ITC Reversal Calculator ➡️ Calculate the exact ITC reversal amount your buyer must make on a given credit note. Share this figure with your dealer to avoid disputes.

GSTIN Validator ➡️ Verify buyer GSTIN status before issuing any credit note. An inactive GSTIN creates portal issues.

GST Rate Checker 2026 ➡️ Confirm the correct GST rate for the goods on which you are giving the post-sale discount.

Penalty Calculator ➡️ If you issued a credit note incorrectly in an earlier period and need to understand the interest implications, this tool calculates the cost.

Related Articles on SmartGST

GSTR-2B Mismatch 2026: Why Your ITC is Blocked and How to Fix It ➡️ When your buyer reverses ITC on your credit note, it shows up in their GSTR-3B. If they do it wrongly, it creates a GSTR-2B mismatch. This guide explains how those mismatches work.

IMS Complete Guide 2026: How Invoice Management System Works ➡️ Credit notes you issue appear in your buyer's IMS dashboard. Understanding IMS is essential for tracking whether buyers have processed your credit notes correctly.

GST 2.0 New Rate Structure 2025-26 ➡️ Rate changes affect the GST component in your credit notes. Confirm the applicable rate under the post-September 2025 structure before calculating credit note amounts.

GST for Amazon, Flipkart and Meesho Sellers 2026 ➡️ E-commerce platforms also run discount schemes and cashback programs. This guide explains the GST treatment for marketplace sellers in the context of seller-funded discounts.

GST Composition Scheme 2026➡️ Composition dealers cannot issue GST credit notes. If your buyer is a composition taxpayer, the post-sale discount must be structured as a financial credit note, not a GST credit note.

References

Section 15(3)(b), CGST Act, 2017 ➡️ as amended by Finance Act 2026 (Clause 137 of Finance Bill 2026)

Section 34(1), CGST Act, 2017 ➡️ as amended by Finance Act 2026 (Clause 138 of Finance Bill 2026)

Rule 53, CGST Rules, 2017 ➡️ Credit note format and mandatory fields

56th GST Council Meeting Recommendations, September 3, 2025 Rate rationalisation and Section 15 amendment

Finance Act 2026 ➡️ Presidential assent and gazette publication, April 2026

Section 50(3), CGST Act ➡️ Interest at 24% on wrongly availed ITC

CBIC Circular on post-sale discounts ➡️ existing departmental clarifications (pre-amendment)

GSTN Advisory on IMS and credit note processing, October 2025

Mondaq Analysis ➡️ "Has the Hydra of Post Sale Discounts Under GST Finally Been Subdued?" (February 2026)

Finance Act 2026 Notification ➡️ taxreply.com reference, April 2026

The Effective Date Is Coming. Get Your Scheme Structure Ready Now.

The Section 15(3)(b) amendment is enacted. The effective date notification is the only thing pending. When it lands possibly in the next gazette notification the entire post-sale discount framework changes overnight.

If you run dealer incentive programs, quarterly schemes, or year-end trade discounts: review how your commercial agreements are structured. Decide now whether you want to move to the new framework or keep existing documentation in place for FY 2025-26 discounts.

Get the notification the same day it drops:

Content verified against Section 15(3)(b) of the CGST Act as amended by Finance Act 2026, Section 34(1) CGST Act, 56th GST Council recommendations (September 2025), and Finance Act 2026 gazette notification. Last updated: 13 June 2026. Consult a CA before restructuring your discount scheme documentation or issuing credit notes under the amended provisions.