A Pune Manufacturer Filed GSTR-3B Like Clockwork for 3 Years. Then January 2026 Happened.

Every month, his accounts team would download GSTR-2B, run a quick eye over it, and file GSTR-3B claiming the ITC from their purchase register. They were 90% accurate. The 10% gap — invoices their suppliers had filed late, or not filed at all — they simply claimed anyway. It had always gone through.

In January 2026, it stopped going through.

GSTN pushed a portal update that hard-blocks ITC claims exceeding GSTR-2B by more than a defined threshold. No override. No manual adjustment. No "we'll fix it next month." The GSTR-3B filing was rejected. The 20th deadline passed. Late fees started accumulating.

Three years of accounting habits, built around a system that was forgiving, collided with a system that is no longer forgiving at all.

If your business claims ITC monthly, this guide tells you exactly what changed, why mismatches happen across five distinct scenarios, and the precise fix for each one — before a notice arrives.

What Changed in January 2026 The Hard Block

Before January 2026, GSTR-3B allowed you to claim ITC beyond what appeared in GSTR-2B. The portal would flag a mismatch but it would still let you file. The mismatch would sit in GSTN's analytics engine and sometimes trigger a scrutiny notice under Section 61 or Rule 88C, sometimes not. Many businesses relied on this tolerance window month after month.

Since January 2026, the portal actively blocks filing if your ITC claim doesn't match GSTR-2B. The update introduced a hard ceiling: if your ITC claim in GSTR-3B exceeds the GSTR-2B figure by more than the permitted variance, the system rejects the return. Sellers who skip the reconciliation step now don't get a warning they get a blocked return, a missed deadline, and a late fee.

This is not a temporary measure. It is the foundation for ITC hard-locking a direction GSTN has been moving toward since IMS launched in October 2024. With the IMS fully operational and the new "Rejected Records" tab rolled out on 18th February 2026, the direction is clear ITC hard-locking is next.

The old workflow of claiming ITC from your purchase register and hoping GSTR-2B catches up is permanently broken.

Understanding GSTR-2B What It Is and Is Not

GSTR-2B is your auto-drafted Input Tax Credit statement, generated on the 14th of every month. It pulls data from:

Your suppliers' GSTR-1 filings (forward charge invoices)

e-Invoice data uploaded to the IRP

ICEGATE (for import-related ITC from Bills of Entry)

ISD (Input Service Distributor) distributions

GSTR-2B is a snapshot in time. It reflects only what your suppliers filed and what the system processed by the 13th of the month. Invoices your supplier files after the 13th appear in the following month's GSTR-2B, not the current one.

GSTR-2B is not GSTR-2A. This distinction still confuses many businesses:

GSTR-2A | GSTR-2B | |

|---|---|---|

Nature | Dynamic updates in real-time | Static fixed snapshot on 14th |

Updates after 14th? | Yes | No |

Used for ITC claim? | Not applicable from April 2022 | Yes mandatory basis |

Legal basis | Advisory/reference | Rule 36(4) mandatory |

Since April 2022, GSTR-2B not GSTR-2A is the mandatory basis for ITC claims. Claiming ITC that doesn't appear in GSTR-2B leads to mismatches. The GST system automatically flags differences between your GSTR-3B claims and GSTR-2B data, triggering notices, interest charges (18% p.a.), and potential penalties.

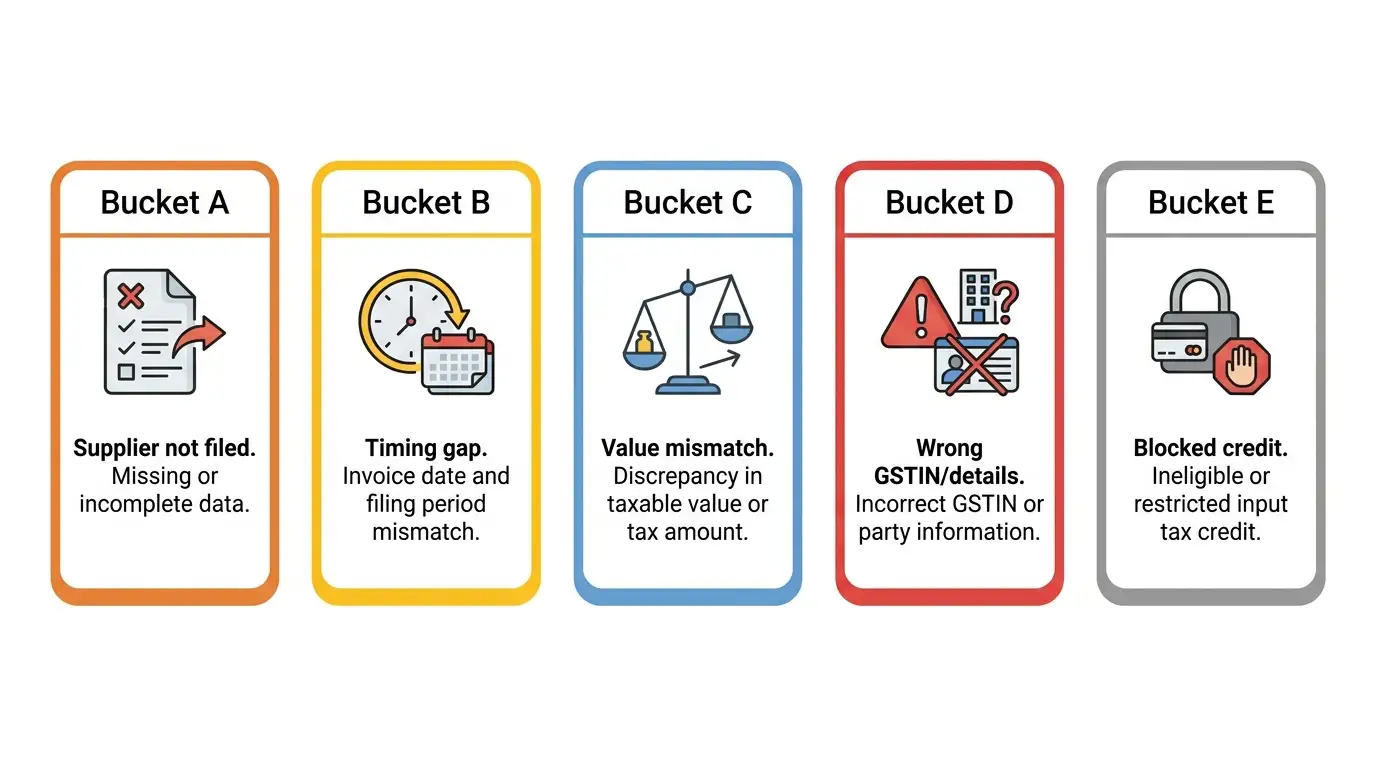

The Five Types of GSTR-2B Mismatches And the Fix for Each

Not all mismatches are the same. Each has a different cause, a different fix, and different legal consequences. Misidentifying the type wastes time and can result in either wrong reversal or missed ITC.

Mismatch Type 1 Supplier Has Not Filed GSTR-1

What it looks like: You have an invoice from a vendor. It is not in your GSTR-2B at all. Your purchase register shows GST paid. GSTR-2B shows nothing.

Why it happens: Your supplier missed their GSTR-1 filing deadline. Their invoice was never uploaded to the system.

What the law says: Section 16(2)(c) requires that the supplier has actually paid the tax. Where the supplier has filed GSTR-1 and the invoice is reflected in GSTR-2A, ITC cannot be denied to the recipient merely because the supplier has not paid the tax to the government. But if they have not filed GSTR-1 at all, even this protection does not fully apply.

The fix:

Contact the supplier immediately. Ask them to file GSTR-1 or amend it to include your invoice.

Do not claim this ITC in the current month's GSTR-3B.

The invoice will appear in a future month's GSTR-2B once the supplier files. Claim it then.

If the supplier repeatedly misses filings, switch suppliers or stop claiming ITC from them.

Timeline risk: Unmatched ITC for FY 2025-26 can be claimed until the due date of the September 2026 GSTR-3B return, or the date of filing GSTR-9 annual return whichever is earlier. After this, the ITC lapses permanently.

Use the SmartGST GSTR-2B Reconciliation Tool to identify exactly which supplier invoices are missing from your GSTR-2B each month.

Mismatch Type 2 Timing Gap (Invoice Filed After 13th)

What it looks like: Your supplier filed GSTR-1 for the month, but your specific invoice is missing from GSTR-2B. GSTR-2A shows the invoice. GSTR-2B does not.

Why it happens: Your supplier filed GSTR-1 after the 13th of the month possibly on the actual due date of the 11th but the system processed it after the GSTR-2B snapshot. Or they filed an amendment after the 13th.

What the law says: This is a timing mismatch, not a genuine non-compliance issue. The invoice exists and the supplier has filed. The ITC is legitimately yours just in the wrong month's GSTR-2B.

The fix:

Do not claim this ITC in the current month. The invoice will appear in next month's GSTR-2B automatically.

Maintain a "carry-forward ITC" tracker for these invoices amounts that are coming in the next period.

When it appears in next month's GSTR-2B, claim it normally.

Prevention: Ask your key suppliers to file GSTR-1 by the 9th of the month instead of the 11th. A two-day buffer ensures their invoices are processed before the 13th snapshot.

Mismatch Type 3 Value or Rate Mismatch

What it looks like: The invoice appears in GSTR-2B but the taxable value or GST amount is different from what you have in your purchase register.

Why it happens: Your supplier made a data entry error in GSTR-1 wrong invoice amount, wrong tax rate, wrong HSN code and the system populated GSTR-2B with the supplier's incorrect figure, not the figure on the physical invoice you received.

What the law says: The department cannot demand reversal of ITC based on auto-generated system mismatches without independent application of mind and verification. But in practice, you can only claim what is in GSTR-2B not what the physical invoice says.

The fix:

Contact your supplier with the discrepancy details. Ask them to amend the invoice in GSTR-1A before the IMS/GSTR-2B generation deadline.

If the GSTR-2B value is lower than the actual invoice (supplier understated): claim only the GSTR-2B amount. The balance appears when the supplier amends.

If the GSTR-2B value is higher than the actual invoice (supplier overstated): claim only the actual eligible ITC. Do not claim the inflated GSTR-2B figure it creates excess ITC that must be reversed later.

Key rule: Match GSTR values exactly taxable value, GST rate, and GST vs CGST/SGST must be identical across returns.

Mismatch Type 4 Wrong GSTIN or Invoice Details

What it looks like: The invoice from your supplier does not appear in your GSTR-2B at all. When you check the supplier's GSTR-1, the invoice exists but it was filed against a different GSTIN (possibly a different branch of your company, or a typo).

Why it happens: Your supplier entered the wrong GSTIN when filing their GSTR-1. This is more common in multi-branch operations where the supplier has multiple GSTIN records for your business.

The fix:

Identify the GSTIN under which the invoice was filed. Check the supplier's GSTR-1 directly if you have access, or ask them.

Ask the supplier to amend the GSTIN in their GSTR-1A.

If the amendment cannot be done (past amendment window): the invoice will not appear in your GSTR-2B and the ITC cannot be formally claimed. Maintain documentary evidence of the error for any future scrutiny response.

Verify your own GST registration details use SmartGST GSTIN Validator to confirm all your branch GSTINs are active and correctly formatted.

Mismatch Type 5 Blocked Credit Appearing in GSTR-2B

What it looks like: An invoice appears in GSTR-2B and the ITC is technically available but the purchase is actually a blocked credit under Section 17(5) of the CGST Act.

Why it happens: GSTR-2B does not filter for Section 17(5) automatically. If your supplier files an invoice for food and beverages, club membership, motor vehicle (personal use), or any other blocked credit category, it shows up in GSTR-2B as available ITC. The system does not block it.

What the law says: Section 17(5) is your responsibility to apply. Claiming ITC shown in GSTR-2B for a blocked credit category is still wrong and still subject to reversal with 24% interest.

The fix:

Review your GSTR-2B line by line for Section 17(5) categories.

Do not claim ITC on blocked credit invoices even if they appear in GSTR-2B.

In IMS, reject these invoices proactively so they do not auto-populate into your GSTR-3B.

Use the SmartGST ITC Eligibility Checker to verify each purchase category before claiming.

The Rule 88C Notice What Happens If You File With a Mismatch

If a mismatch slips through (possible in edge cases where the variance is within the portal's tolerance), GSTN's automated analytics engine generates a Rule 88C notice a system-generated alert asking you to explain the discrepancy between your GSTR-3B ITC claim and your GSTR-2B.

This is not a full-blown scrutiny notice. It is an automated system flag. But ignoring it converts it into a formal proceeding.

How to respond to a Rule 88C notice:

Do not panic. Do not pay immediately.

Download the mismatch report attached to the notice.

Classify each mismatch line into one of the five types above.

For Type 1 and 2 (timing/supplier filing issues): prepare a reconciliation statement showing the invoice exists, the supplier has filed (or will file), and the ITC is legitimate.

For Type 3 (value mismatch): prepare a supplier communication trail showing the amendment request.

For Type 4 (wrong GSTIN): document the supplier error with email evidence.

For Type 5 (blocked credit already claimed): reverse the ITC voluntarily with interest before responding this dramatically reduces your penalty exposure.

Use the SmartGST GST Notice Reply Generator to draft a structured DRC-01A or Rule 88C response with proper reconciliation annexures.

Don't ignore DRC-01A it's an opportunity, not a formality. Don't pay without verification verify the demand computation before making any payment. Don't submit without reconciliation a bare reply saying "mismatch is due to timing" without a reconciliation statement is insufficient.

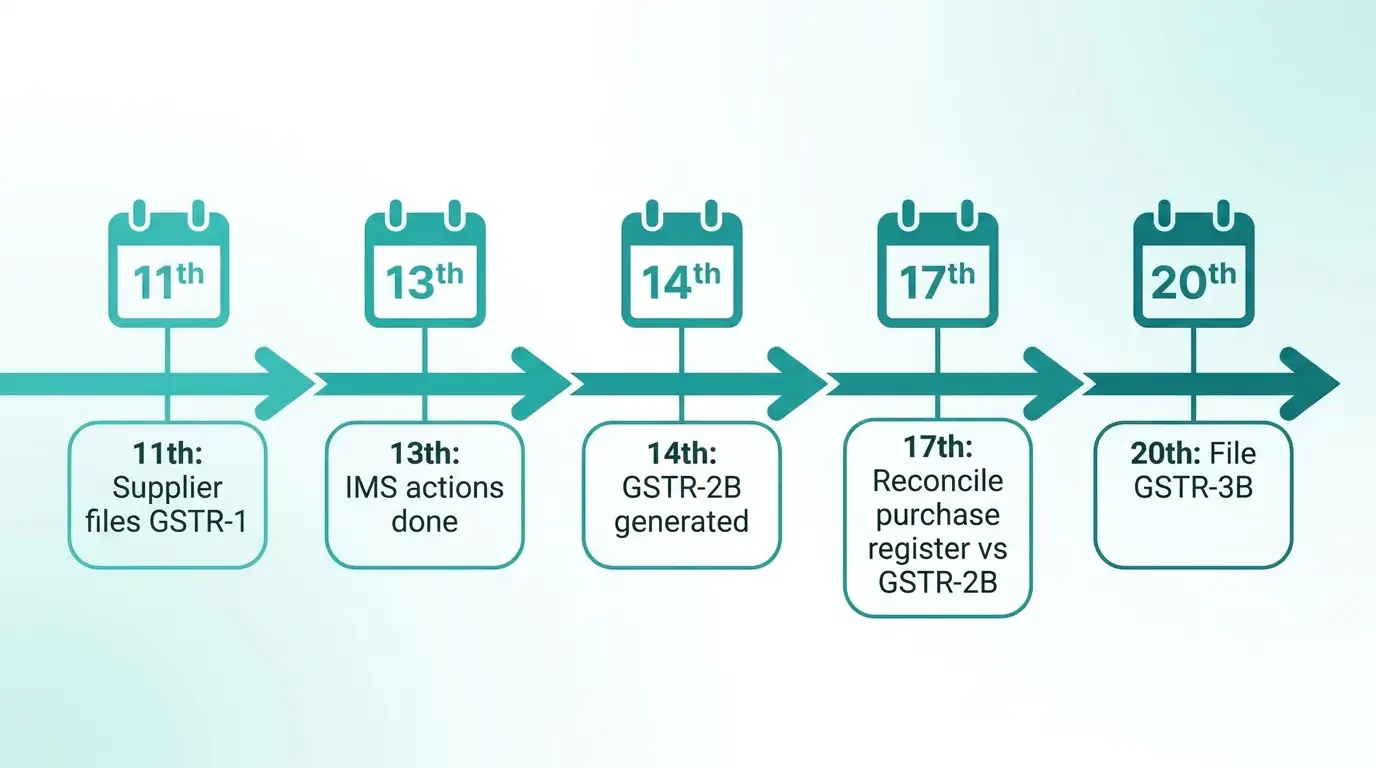

The Correct Monthly Reconciliation Workflow Five Steps

The correct sequence is fixed. Do not file GSTR-3B before completing each step in order.

Step 1 ➡️ By the 11th: Ensure your key suppliers have filed GSTR-1 Chase non-filers before the 13th snapshot. A supplier who files on the 11th makes the 13th cutoff. A supplier who files on the 14th does not.

Step 2 ➡️ By the 13th: Complete IMS actions Review your IMS dashboard. Accept valid invoices. Reject blocked credits and unrecognised invoices. Mark genuinely disputed invoices as Pending. Do not leave everything for auto-acceptance especially for high-value or unusual invoices.

Step 3 ➡️ On the 14th: Download GSTR-2B After GSTR-2B generates, download both the PDF summary and the Excel/JSON detail. Do not rely on the portal's on-screen display for reconciliation the downloadable file has full invoice-level detail.

Step 4 ➡️ By the 17th: Reconcile GSTR-2B against your purchase register Match every line in GSTR-2B against your purchase register. Classify each unmatched item into one of the five mismatch types. Resolve what can be resolved before the 20th. For genuine Type 1/2 mismatches where the ITC is coming next month, maintain a carry-forward tracker.

Step 5 ➡️ By the 19th: Prepare and verify GSTR-3B The safest practice: file GSTR-1 by the 9th, reconcile both statements by the 17th, file GSTR-3B by the 19th. Filing one day before the due date gives you a buffer for portal errors and processing delays.

The 180-Day ITC Reversal Rule One More Thing to Track

Beyond GSTR-2B mismatches, there is a time-based ITC reversal that many businesses forget entirely.

Under Rule 37 of the CGST Rules: if you have claimed ITC on a purchase invoice but have not paid the supplier within 180 days of the invoice date, you must reverse that ITC in the month when the 180-day period expires.

If you bought ₹1L of inventory in October 2025, claimed ₹18,000 ITC, and still haven't paid the vendor by April 2026 (180 days later), you must reverse the ₹18,000 ITC in your April 2026 GSTR-3B.

Once you pay the vendor even after the 180-day period you can re-claim the ITC in the month of payment. But the reversal must happen on time. Missing it means the reversal is treated as incorrect ITC claiming, with interest from the original claim date.

Use the SmartGST ITC Reversal Calculator to track which invoices are approaching the 180-day mark each month.

Tools for GSTR-2B Reconciliation

GSTR-2B Reconciliation Tool ➡️ Upload your purchase register and match it against GSTR-2B data line by line. Identifies each type of mismatch automatically.

ITC Eligibility Checker ➡️ Before claiming any ITC line from GSTR-2B, verify it is not a blocked credit under Section 17(5).

ITC Reversal Calculator ➡️ Track invoices approaching the 180-day payment deadline and calculate the exact reversal amount for each.

GSTR Mismatch Checker ➡️ Cross-validate GSTR-1, GSTR-2B, and GSTR-3B data to catch discrepancies before filing.

GST Notice Reply Generator ➡️ If a Rule 88C or DRC-01A notice has already arrived, use this to draft a structured response with proper reconciliation annexures.

GSTIN Validator ➡️ For Type 4 mismatches (wrong GSTIN), verify the correct GSTIN before requesting supplier amendments.

GST Health Score ➡️ Get an overall picture of your compliance risk including ITC reconciliation gaps, filing consistency, and mismatch history.

Related Articles

GST Invoice Management System (IMS) Complete Guide 2026 ➡️ IMS is the step before GSTR-2B. Master IMS first and most GSTR-2B mismatches will not occur in the first place.

How to Verify a Fake GST Invoice 5 Checks in 30 Seconds ➡️ Many GSTR-2B mismatches trace back to suppliers who are not genuinely compliant. Verify before buying.

How to File GSTR-3B Complete Guide 2025-26 ➡️ The complete GSTR-3B filing process with updated IMS and GSTR-2B workflow.

GSTAT Appeal Deadline 30 June 2026 ➡️ If an older ITC mismatch has resulted in a formal demand order, GSTAT is your appeal forum.

GST Notice How to Check and Respond ➡️ Full guide for responding to GST scrutiny notices including Rule 88C, DRC-01A, and Section 61.

References

Section 16(2), CGST Act, 2017 ➡️ Conditions for ITC eligibility

Section 16(2)(c), CGST Act, 2017 ➡️ Supplier tax payment requirement

Rule 36(4), CGST Rules, 2017➡️ ITC restricted to GSTR-2B amounts

Rule 37, CGST Rules, 2017 ➡️ Reversal of ITC on non-payment to supplier (180-day rule)

Rule 88C, CGST Rules, 2017 ➡️ Automated mismatch notice procedure

Section 73, CGST Act, 2017 ➡️ Determination of tax and limitation period (3 years)

Section 74, CGST Act, 2017 ➡️ Fraud and wilful misstatement (5 years)

CBIC Circular No. 183/15/2022-GST ➡️ Clarification on GSTR-2B and ITC reconciliation

GSTN Portal Update Notes ➡️ January 2026 ITC hard-block implementation

CA Club India ➡️ CA Survival Guide to ITC Reconciliation Post GSTR-3B Hard-Locking, March 2026

Stop Reconciling on the 19th. Start on the 1st.

The businesses that sleep well on the 20th of every month are not the ones with perfect suppliers. They are the ones that reconcile continuously a little every week, not everything the night before the deadline.

Every GSTN advisory, portal update, and compliance change that affects your ITC workflow explained in plain English, within 24 hours:

Content verified against Section 16(2) of CGST Act 2017, Rule 88C of CGST Rules, and GSTN portal updates effective January 2026. Last updated: 9 June 2026. Consult a qualified CA for case-specific ITC dispute advice.