⚠️ This Is Not a Routine GST Update

GSTAT India's GST Appellate Tribunal is now operational after 8 years.

Over 4.8 lakh GST demand orders sit in a backlog with no second appeal filed. If one of those orders is yours, you have one window left: 30 June 2026.

After that date, the only path is the High Court which costs 5x more, takes 3x longer, and rejects most GST petitions on jurisdiction grounds. Miss this deadline by even one day and your right to a second appeal is gone permanently.

This guide tells you exactly who qualifies, how to calculate the pre-deposit correctly, what documents you need, and how to file step by step.

What Is GSTAT and Why Does It Matter Now?

The GST Appellate Tribunal (GSTAT) is the second-tier appellate body under Section 109 of the CGST Act, 2017. When a GST officer raises a demand against you for ITC reversal, a rate mismatch, or an input credit claim you first fight it before the Adjudicating Authority. If you lose there, you go to the First Appellate Authority (Commissioner Appeals). If you lose there too, the next stop is GSTAT.

That second stop did not exist for eight years.

From July 2017 to September 2025, GSTAT existed in law but never became operational. No benches. No judges. No hearings. Taxpayers who lost at the first appeal stage had only one option: the High Court. For most small and mid-sized businesses, that meant ₹5–10 lakh in legal costs per case, multi-year timelines, and judges who were not GST specialists.

The result was an appellate vacuum. Over 5.82 lakh first-appeal orders were passed with no GSTAT remedy. Disputed amounts across these cases exceed ₹1 lakh crore.

The 56th GST Council meeting on 3 September 2025 changed this. The Council recommended GSTAT operationalisation and fixed 30 June 2026 as the universal deadline for all backlog appeals. Finance Minister Nirmala Sitharaman formally launched the GSTAT e-filing portal on 24 September 2025. The Principal Bench in New Delhi began adjudicatory hearings on 16 February 2026.

The clock is running.

Who Can File a GSTAT Appeal And Who Cannot

Before you spend time on documentation, confirm you meet the basic eligibility criteria.

You CAN file if:

You received an adverse order from the First Appellate Authority (Form GST APL-04) under Section 107 of the CGST Act

OR you received an adverse order from the Revisional Authority under Section 108

The order was communicated to you before 1 April 2026 → file before 30 June 2026

The order was communicated on or after 1 April 2026 → normal 3-month window applies from communication date

The disputed tax amount exceeds ₹50,000 (Section 112(2) minimum threshold)

You are a registered taxpayer company, LLP, partnership firm, or proprietorship

You CANNOT file if:

Your disputed amount is below ₹50,000 GSTAT can refuse admission

You already have a High Court writ petition on the same matter you must withdraw it first

Your order was from the Adjudicating Authority directly that goes to Commissioner Appeals (first appeal), not GSTAT

Important: The date that matters is the date the order was communicated to you not the date printed on the order. These can differ. Check your Form GST APL-04 for the communication date.

If you are unsure whether your case qualifies, use the SmartGST GST Notice Tracker to log and monitor your pending orders.

The Numbers Behind the Deadline

Understanding the scale of this situation explains why the government has not extended and will not extend this deadline:

Metric | Number |

|---|---|

First-appeal orders passed (2017–2026) | 5.82 lakh |

Appeals expected at GSTAT by 30 June 2026 | ~2 lakh |

Total disputed amount in backlog | > ₹1 lakh crore |

GSTAT benches operational (June 2026) | Principal Bench + 31 state benches |

Minimum pre-deposit per case | 10% of disputed tax |

Maximum pre-deposit cap (CGST) | ₹20 crore |

High Court threshold for further appeal | ₹1 crore |

GSTAT President Justice Sanjaya Kumar Mishra has publicly urged taxpayers not to wait. With 4.8 lakh backlog cases competing for portal bandwidth and CA availability in the final weeks, filing in the last 10 days is a genuine operational risk not a theoretical one.

Calculating Your Pre-Deposit Get This Right or Your Appeal Is Rejected

The pre-deposit is the most misunderstood part of GSTAT filing. Getting it wrong means your appeal is not admitted no hearing, no arguments, no refund of whatever you already deposited.

Under Section 112(8) of the CGST Act, the pre-deposit structure works in two stages:

Stage 1 → First Appeal (Section 107(6)): You already paid 10% of the disputed tax when you filed at the Commissioner Appeals level.

Stage 2 → GSTAT Appeal (Section 112(8)): You pay an additional 10% of the remaining disputed tax at the GSTAT stage.

The total cumulative pre-deposit across both stages is 20% of the disputed tax amount, capped at ₹20 crore for CGST and ₹20 crore for SGST.

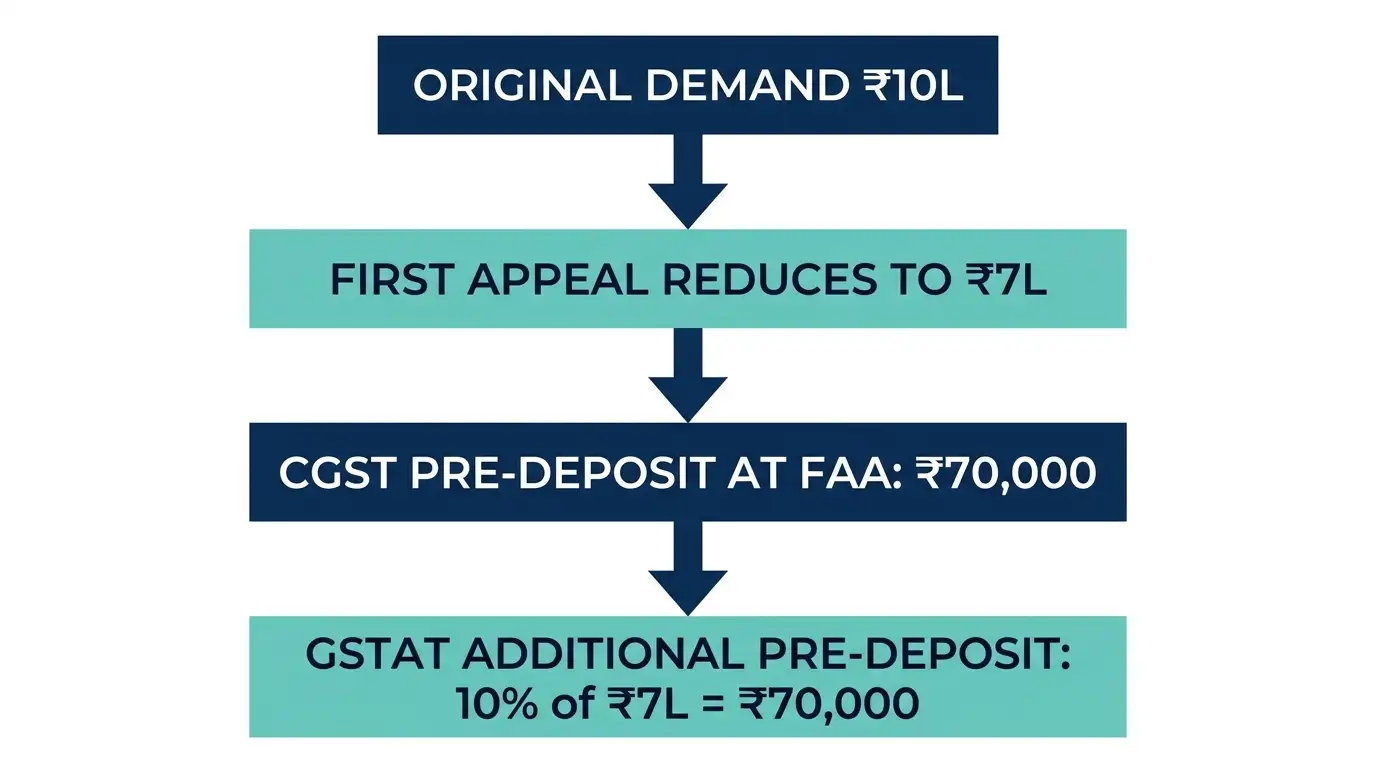

Worked Example:

Imagine a textile business in Surat received a GST demand for a disputed ITC reversal.

Original demand confirmed by Adjudicating Authority: ₹10 lakh CGST

Pre-deposit paid at first appeal stage (10%): ₹1 lakh

First Appellate Authority reduced demand to: ₹7 lakh CGST

Remaining disputed tax at GSTAT stage: ₹7 lakh

GSTAT pre-deposit required (additional 10%): ₹70,000

Total pre-deposit paid across both stages: ₹1,70,000 (17% of original demand)

Three critical rules:

Pre-deposit is calculated only on tax in dispute not on interest or penalty (unless it is a penalty-only order, in which case 10% of penalty applies separately from Finance Act 2025)

Payment must come from the Electronic Cash Ledger only ITC credit cannot be used for pre-deposit

If you won a partial reduction at first appeal, your GSTAT pre-deposit is on the reduced amount, not the original demand

Use the SmartGST Penalty Calculator to estimate your outstanding tax and interest before computing the pre-deposit base.

If you over-deposited at the first appeal stage (because the demand was later reduced), you may not need to pay fresh amounts at GSTAT. The excess from Stage 1 can be set off against Stage 2 requirements. Get this checked by a GST practitioner before paying.

Step-by-Step: How to File Your GSTAT Appeal

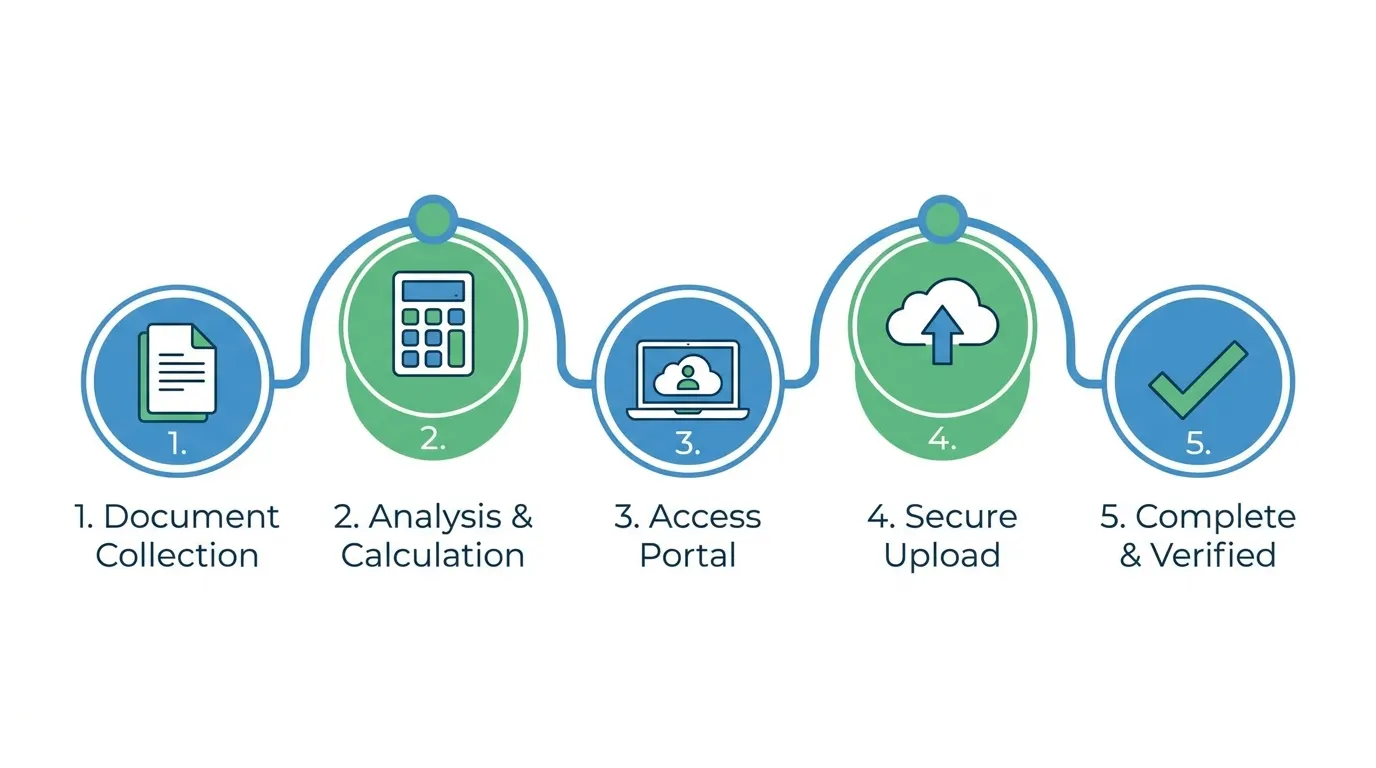

Filing is entirely online. There is no physical submission. Here is the exact sequence:

Step 1 → Gather Your Documents

Collect these before you open the portal:

Certified copy of the First Appellate Authority order (Form GST APL-04)

Original demand order from the Adjudicating Authority (Form GST DRC-07 or equivalent)

Proof of pre-deposit payment at first appeal stage

Your company/firm registration documents and authorised signatory details

Digital Signature Certificate (DSC) mandatory for companies; optional but recommended for others

Grounds of appeal memo drafted specifically (see Section 6 below on common mistakes)

Any supporting evidence: invoices, GSTR-2B data, e-way bills, contracts

Step 2 → Pay the Pre-Deposit

Before opening the portal, complete the payment:

Login to the main GST portal at gst.gov.in

Go to Services → Payments → Create Challan

Select "CGST" under tax head, mention "Pre-deposit for GSTAT appeal under Section 112(8)"

Pay through net banking or UPI

Download the DRC-03 acknowledgement you will upload this at GSTAT

Step 3 → File on GSTAT e-Filing Portal

Go to efiling.gstat.gov.in

Login using your GSTIN and DSC

Select "File New Appeal" → choose Form GST APL-05

Enter your order details, disputed amounts, and grounds of appeal

Upload all documents certified order copy, DRC-03 payment proof, appeal memo

Submit with DSC signature

Step 4 → Upload Remaining Documents Within 7 Days

After submission, you get a Provisional Acknowledgement immediately. You have 7 days to upload any remaining supporting documents and translations (if any documents are in a regional language).

Step 5 → Get Your Final Acknowledgement

The GSTAT registry reviews your filing for defects. If the filing is complete, they issue the Final Acknowledgement (Form GST APL-02A, Part B).

This is the most missed step. Your appeal is legally valid only from the date of the Final Acknowledgement not from submission. A provisional acknowledgement alone does not protect you. If the registry returns your filing as defective after 30 June 2026, you lose your window even if you submitted before the deadline.

File early. Leave time to fix defects.

Three Mistakes That Get Appeals Rejected

Based on patterns in early GSTAT filings (September 2025 to April 2026), these are the most common errors:

Mistake 1: Calculating pre-deposit on the original demand instead of the remaining disputed amount

A business received a ₹20 lakh demand. First appeal reduced it to ₹12 lakh. They calculated their GSTAT pre-deposit on ₹20 lakh (10% = ₹2 lakh) instead of ₹12 lakh (10% = ₹1.2 lakh). Overpaid, but more critically they did not correctly identify the "remaining disputed tax" in the portal entry. Filing was returned as defective. They lost 11 days fixing it.

Mistake 2: Writing vague grounds of appeal

"The demand order is incorrect and excessive" is not a valid ground of appeal. GSTAT's registry returns these filings. Each ground must state:

Which specific provision of the CGST/SGST Act the authority misapplied

What the correct interpretation is, with case law if available

What specific relief you are seeking

Example of a valid ground: "The First Appellate Authority erred in reversing ITC amounting to ₹3.8 lakh under Section 16(2)(c) without examining GSTR-2B data for the relevant tax period, which demonstrates supplier tax payment. Relief sought: restoration of ITC of ₹3.8 lakh."

Mistake 3: Stopping at the Provisional Acknowledgement

Multiple filers treated the provisional acknowledgement as confirmation of a valid filing. When the GSTAT registry found defects and returned the filings in late May 2026, some had already missed the practical window to resubmit quality documentation before 30 June. The Final Acknowledgement is the only valid proof of a filed appeal.

Frequently Asked Questions

Q: Will the 30 June 2026 deadline be extended?

No indication of any extension exists. The original deadline of September 2025 was already an extension from the standard 3-month window. The government has been explicit: 30 June 2026 is a hard cutoff under Notification S.O. 4220(E). GSTAT President Justice Sanjaya Kumar Mishra has publicly stated this is firm. If you miss it, the only remedy is the High Court under Article 226/227 of the Constitution, with a monetary threshold of ₹1 crore.

Q: Can I use ITC from my Electronic Credit Ledger to pay the pre-deposit?

No. Section 112(8) requires pre-deposit payment only through the Electronic Cash Ledger. ITC is not accepted for this purpose. You need actual cash in your GST cash ledger. Plan your liquidity accordingly, especially if you have multiple appeals to file.

Q: My order came after 1 April 2026 what is my deadline?

The 30 June 2026 deadline applies specifically to backlog cases orders communicated before 1 April 2026. For orders on or after 1 April 2026, the standard 3-month limitation period under Section 112(1) applies from the date of communication of the FAA order. Section 112(6) allows an additional 3-month condonation on sufficient cause.

Q: Can I file a GSTAT appeal if I already filed a High Court writ petition on the same matter?

You must withdraw the High Court petition before filing at GSTAT. High Courts across India have begun declining jurisdiction in GST matters where GSTAT is the appropriate forum, so the writ petition may not help you anyway. Speak to a GST advocate before taking any steps here, as the sequence of withdrawal and GSTAT filing matters for limitation.

Q: What happens to my case if I win at GSTAT do I get the pre-deposit back?

Yes. Under Section 115 of the CGST Act, if GSTAT decides in your favour and the demand is reduced or deleted, you are entitled to a refund of the pre-deposit with interest at the rate prescribed under Section 56 (currently 9% per annum) from the date of payment until the date of refund. The refund is not automatic you must apply for it after the GSTAT order.

Q: What is the minimum disputed amount required to file at GSTAT?

Section 112(2) sets a minimum threshold. GSTAT may refuse to admit appeals where the disputed amount is below ₹50,000. If your case is near or below this threshold, assess carefully whether the cost of filing (pre-deposit + professional fees) makes commercial sense.

What GSTAT Means for Your Business Going Forward

The operationalisation of GSTAT changes the GST dispute landscape permanently not just for the backlog, but for all future disputes.

For the first time, Indian businesses have a cost-effective, technically specialized forum for GST disputes. A GSTAT bench handles only GST matters. Judges are GST specialists. Filing is digital. Orders must be passed within 30 days of the final hearing.

Compare this to High Courts where a GST petition competes for hearing time with criminal matters, civil suits, constitutional challenges, and thousands of other cases. High Court timelines for GST matters routinely run to 5–8 years. GSTAT targets 12 months.

For businesses with ongoing GST compliance, this tribunal changes the risk calculus of GST litigation. With a functioning second appeal forum, fighting a disputed demand is now financially viable for mid-sized businesses that previously could not absorb High Court costs.

Stay current on all GST dispute and compliance updates using the SmartGST Compliance Checklist and GST Notice Tracker.

Key Dates Quick Reference

Date | Event |

|---|---|

3 September 2025 | 56th GST Council recommends GSTAT operationalisation |

17 September 2025 | Notification S.O. 4220(E) 30 June 2026 deadline notified |

24 September 2025 | GSTAT e-filing portal launched by Finance Minister |

16 December 2025 | Staggered filing restrictions lifted all appeals can now be filed |

16 February 2026 | GSTAT Principal Bench begins adjudicatory hearings |

1 April 2026 | Cut-off orders before this date fall under backlog deadline |

30 June 2026 | Hard deadline all backlog appeals must be filed by this date |

Useful Tools to Help You Prepare

Before filing your GSTAT appeal, use these free SmartGST tools to check your GST standing and prepare your case:

GST Notice Reply Generator →Understand the notice or demand order you received and draft a structured reply

GST Notice Tracker → Track all your pending GST notices and appeal deadlines in one place

Penalty Calculator → Calculate outstanding tax, interest, and penalty before computing your pre-deposit base

GSTIN Validator → Verify your GSTIN and supplier GSTINs are active before compiling your documents

GST Health Score → Get an overview of your overall GST compliance risk profile

GSTR-2B Reconciliation Tool → If your dispute involves ITC claims, reconcile your purchase data against GSTR-2B before drafting appeal grounds

Related Guides on SmartGST

How to Check and Respond to a GST Notice If you have received a demand order, start here before filing any appeal How to Claim a GST Refund Relevant once your GSTAT appeal succeeds and you are entitled to a refund with interest

GST Late Fee and Penalty Guide 2026 Understand the penalty structure that may be part of your disputed demand

How to File GSTR-3B If your dispute arose from a GSTR-3B mismatch, this guide covers the filing process correctly

References

Section 112, Central Goods and Services Tax Act, 2017 → View on India Code

Ministry of Finance Notification S.O. 4220(E) dated 17 September 2025 → GSTAT backlog deadline notification

56th GST Council Meeting Press Release, 3 September 2025 → PIB

GSTAT e-Filing Portal → efiling.gstat.gov.in

CBIC Official Website → cbic.gov.in

Finance Act 2024 → Amendment to Section 112(8) reducing pre-deposit cap to ₹20 crore

Finance Act 2025 → Introduction of 10% pre-deposit for penalty-only orders (Section 112(8)(b))

Presidential Order No. 315/2025 dated 16 December 2025 Lifting of staggered filing restrictions

M/s Evergreen Construction & Anr. v. Commissioner of Commercial Taxes, Calcutta HC, MAT 424 of 2024, Pre-deposit confined to tax in dispute, not interest

Stay Updated Never Miss a GST Deadline

GST rules change fast. The GSTAT transition is ongoing new bench operationalisation notifications, portal updates, and CBIC circulars will continue through 2026.

Join the SmartGST WhatsApp Channel for instant updates: Every GST circular, deadline, and rate change explained in plain English, within 24 hours of notification.

No spam. No promotional content. Just GST updates that matter to your business.

Content verified against CBIC Notification S.O. 4220(E) dated 17 September 2025 and Section 112 of the CGST Act, 2017. Last updated: 5 June 2026. This article is for informational purposes only. Verify with gst.gov.in or consult a qualified CA before filing any appeal.