A Ludhiana Hardware Dealer Pays ₹72,000 in GST Per Year. His Neighbour With the Same Turnover Pays ₹3,24,000.

Both run hardware shops on the same street. Same type of goods. Same annual turnover ₹1.08 crore. Both are fully GST compliant.

The difference is one decision made every March: one is on the GST Composition Scheme and one is not.

The composition dealer pays 1% of turnover ₹1,08,000 per year split quarterly. But because he buys from manufacturers who pay GST, he gets no ITC. His effective cost after accounting for input prices works out to about ₹72,000 in net tax impact.

The regular GST dealer pays 18% on all sales and claims ITC on purchases. His monthly ITC roughly offsets much of his output tax. But his net GST liability after all ITC adjustments, CA fees, and reconciliation costs works out to ₹3,24,000 per year.

The composition scheme saved this dealer ₹2.5 lakh per year. Or it could have destroyed him if most of his customers were other businesses who needed ITC from him which they cannot get from a composition dealer.

This is the guide that tells you which side of that story your business falls on.

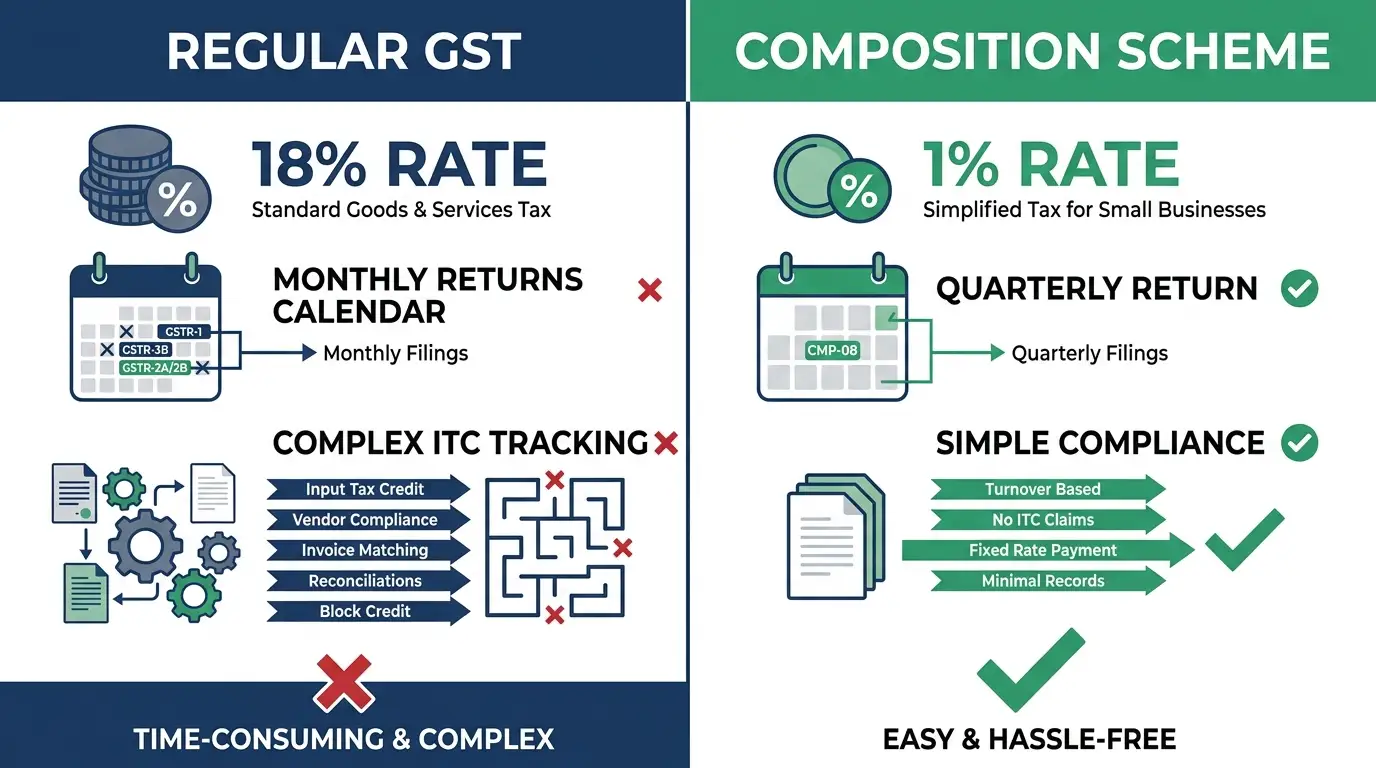

What Is the GST Composition Scheme?

The GST Composition Scheme is a simplified taxation option under Section 10 of the CGST Act, 2017, designed for small businesses. Instead of calculating output GST on every invoice and claiming ITC on every purchase, a composition dealer:

Pays GST at a flat percentage of their total turnover

Cannot collect GST separately from customers (no "GST charged" line on invoices)

Cannot claim ITC on any purchases

Files returns quarterly instead of monthly

Cannot supply goods across state borders

It is a trade-off: simplicity and lower compliance cost in exchange for no ITC and no interstate sales.

The scheme was introduced because the standard GST regime with monthly GSTR-1, GSTR-3B, ITC reconciliation, and the entire compliance machinery was genuinely unmanageable for small businesses with limited accounting capacity. A vegetable seller or a local grocery store was not designed to run a monthly GST compliance cycle.

Who Can Use the Composition Scheme Eligibility in Full

Turnover Limits for FY 2026-27

Business Category | Turnover Limit |

|---|---|

Manufacturers of goods | ₹1.5 crore aggregate annual turnover |

Traders and retailers | ₹1.5 crore aggregate annual turnover |

Restaurants (not serving alcohol) | ₹1.5 crore aggregate annual turnover |

Service providers (including mixed supply) | ₹50 lakh aggregate annual turnover |

Special category states (8 states including NE + Himachal) | ₹75 lakh for goods, ₹50 lakh for services |

Important: "Aggregate turnover" is calculated at the PAN level across all GST registrations. If you have two businesses under the same PAN one with ₹80 lakh turnover and one with ₹90 lakh turnover your combined aggregate is ₹1.7 crore, which exceeds the limit. The scheme is not available to you even if each business is individually below ₹1.5 crore.

Who Is Specifically Excluded

Even below the turnover limit, these businesses cannot use the composition scheme:

Businesses making inter-state supplies (selling to buyers in other states)

Businesses supplying goods through e-commerce platforms on which TCS is collected (Amazon, Flipkart, Meesho sellers specifically those covered under Section 52 TCS)

Manufacturers of pan masala, tobacco, ice cream, and certain notified goods

Non-resident taxable persons

Casual taxable persons

Persons supplying goods not leviable to GST (but who also supply taxable goods)

Tax Rates Under the Composition Scheme

Business Type | CGST Rate | SGST Rate | Total Rate |

|---|---|---|---|

Manufacturers of goods | 0.5% | 0.5% | 1% |

Traders (buying and selling goods) | 0.5% | 0.5% | 1% |

Restaurants (without liquor licence) | 2.5% | 2.5% | 5% |

Service providers / mixed supply | 3% | 3% | 6% |

These rates apply on total turnover, not on the margin. A trader who buys goods for ₹80 lakh and sells for ₹1 crore pays 1% on ₹1 crore (₹1 lakh) not on the ₹20 lakh margin.

This is where the ITC trade-off becomes critical: if your suppliers charge you significant GST on your purchases, that GST is a dead cost under the composition scheme because you cannot claim it back.

Use the SmartGST Composition Scheme Calculator to model the exact tax under both schemes for your specific turnover and purchase mix.

The Real Calculation Composition vs Regular GST

This is the decision most businesses get wrong because they look at rates in isolation instead of doing the net calculation.

Scenario: A saree trader in Varanasi

Annual purchases: ₹80 lakh (GST on purchases: ~₹4 lakh at 5%)

Annual sales: ₹1 crore (GST at 5% on sales: ₹5 lakh)

Customers: 70% end consumers, 30% retailers who need ITC

Under Regular GST:

Output tax: ₹5 lakh

ITC on purchases: ₹4 lakh

Net GST payable: ₹1 lakh

But: monthly GSTR-1, GSTR-3B filing, ITC reconciliation, CA fees ~₹36,000/year

Plus: 30% of customers happy (they can claim ITC from you)

Total effective cost: ~₹1.36 lakh per year

Under Composition Scheme:

Tax at 1% on ₹1 crore: ₹1 lakh

No ITC on ₹4 lakh purchases this ₹4 lakh is a real cost absorbed in pricing

Quarterly CMP-08 + annual GSTR-4 filing CA fees ~₹12,000/year

But: 30% of customers (retailers) cannot buy from you because they need ITC invoices

Potential revenue loss if those retailers switch suppliers

Total effective cost: potentially ₹1.12 lakh in direct tax + significant business impact

For this trader, if the 30% retailer customers represent critical business relationships composition scheme would hurt his business even though it saves tax on paper.

This is the calculation that determines the right choice for your business.

Returns Under the Composition Scheme What You Actually File

This is where the simplicity advantage is most visible.

CMP-08 (Quarterly Self-Assessment)

What it is: A quarterly challan-cum-statement where you declare your total turnover for the quarter and pay the applicable tax.

Due dates FY 2026-27:

Quarter | Period | Due Date |

|---|---|---|

Q1 | April–June 2026 | 18 July 2026 |

Q2 | July–September 2026 | 18 October 2026 |

Q3 | October–December 2026 | 18 January 2027 |

Q4 | January–March 2027 | 18 April 2027 |

What to declare: Total outward supply (your sales turnover), inward supplies on reverse charge (if any), and tax payable.

Late fee: ₹200 per day (₹100 CGST + ₹100 SGST), capped at ₹5,000 per return. Plus 18% interest per annum on unpaid tax.

GSTR-4 (Annual Return)

What it is: A comprehensive annual summary return covering the entire financial year.

Due date: 30 June 2027 for FY 2026-27.

What it covers: Consolidated outward supplies, inward supplies, and tax paid across all four quarters. Reconciliation of CMP-08 payments against annual turnover.

Important: Do not confuse the GSTR-4 due date with regular taxpayer due dates. GSTR-4 for FY 2025-26 is due 30 June 2026. Use the SmartGST Due Date Calendar to track both CMP-08 and GSTR-4 deadlines.

Compare this to a regular GST taxpayer: 12 GSTR-1s + 12 GSTR-3Bs + 1 GSTR-9 = 25 returns per year. A composition dealer files 4 CMP-08s + 1 GSTR-4 = 5 returns per year. The compliance reduction is real and significant.

How to Switch to the Composition Scheme

New Businesses (At Time of Registration)

When applying for GST registration via Form GST REG-01 on the GST portal, select "Yes" for the question "Whether applying for registration as Composition Taxable Person." Your registration is granted under the composition scheme directly.

Existing Regular Taxpayers (Switching to Composition)

Form CMP-02 is the declaration filed to opt into the composition scheme for the next financial year.

Filing window: CMP-02 must be filed by March 31 of the preceding year. For FY 2026-27, the deadline was 31 March 2026. If you missed it, you cannot opt into composition for FY 2026-27 you must continue under the regular scheme and reapply before 31 March 2027 for FY 2027-28.

Step-by-step CMP-02 filing:

Login to gst.gov.in

Go to Services → Registration → Application to Opt for Composition Levy

Read and confirm the terms of the scheme

Submit Form CMP-02 with DSC or EVC

Reference number generated immediately no approval waiting period

Effective from April 1 of the next FY

Critical: File ITC-03 within 60 days of switching

When you switch from regular to composition, you must reverse all ITC on your closing stock inputs held in stock, semi-finished goods, finished goods, and capital goods as of the switchover date.

This is the biggest financial shock when switching. A trader with ₹25 lakh in closing stock on March 31 and ₹2.25 lakh in accumulated ITC on that stock must reverse the entire ₹2.25 lakh. That is a cash outflow before the composition scheme starts saving you money.

Calculate this reversal using the SmartGST ITC Reversal Calculator before committing to the switch.

How to Exit the Composition Scheme

Voluntary Exit (Form CMP-04)

If your business grows beyond the composition threshold or you decide the regular scheme works better, file Form CMP-04 to voluntarily exit.

Effect: Immediately treated as a regular taxpayer from the date of CMP-04 filing. Must begin issuing tax invoices, collecting GST from customers, and filing monthly returns from the next tax period.

On exit: You become eligible for ITC on your closing stock from the date of exit. However, you cannot re-enter the composition scheme in the same financial year once you exit.

Mandatory Exit (Turnover Breach)

If your turnover crosses the composition limit (₹1.5 crore for goods, ₹50 lakh for services) at any point during the year, you must exit the composition scheme from the date of the breach.

This mid-year exit creates the most complexity: two different compliance regimes in the same financial year, ITC adjustments, stock valuation changes. If you are growing rapidly and expect to cross the threshold during the year, it is better to opt out proactively at the start of the year than to be forced out mid-year.

Five Things Composition Dealers Get Wrong

1. Charging GST separately on invoices

A composition dealer cannot issue a tax invoice. They must issue a "Bill of Supply" which is similar but does not show GST charged. If a composition dealer writes "GST: ₹X" on their invoice and collects it from the customer, they have collected GST illegally and are liable to pay it to the government even though they are not eligible to collect it.

2. Not writing "Composition Taxable Person" on invoices

Every bill of supply issued by a composition dealer must prominently state: "Composition Taxable Person, not eligible to collect tax on supplies." Omitting this is a compliance violation under Rule 8 of CGST Rules.

3. Making any inter-state supply without realising it disqualifies them

If a composition dealer sells goods to a buyer in another state even once they are disqualified from the scheme from that day. A furniture manufacturer in Rajasthan who takes one order from a hotel in Mumbai has technically breached the composition scheme condition. The disqualification is not just for that transaction it applies from the date of the breach.

4. Assuming composition scheme applies to all registrations separately

The composition scheme applies at the PAN level. If you have three GST registrations under the same PAN (say, in three different states), all three must be on the composition scheme or none. You cannot selectively put one registration on composition.

5. Forgetting CMP-08 when there are no sales

Even if you had zero sales in a quarter, CMP-08 must be filed as a nil return. Failing to file attracts ₹200/day late fee. There is no "nil = no obligation" exception under the composition scheme.

Composition Scheme Decision Framework Which Side Are You On?

Choose the composition scheme if:

Your customers are mostly end consumers (B2C) they don't need ITC from you

Your business operates in a single state no interstate sales

Your annual turnover is comfortably below ₹1 crore (well clear of the ₹1.5 crore limit)

Your ITC claims are small relative to your tax liability (low input GST)

You want to reduce compliance burden significantly

Stay on regular GST if:

A significant portion of your customers are GST-registered businesses they need ITC from your invoices

You have inter-state sales or plan to expand to other states

Your turnover is growing rapidly and may cross ₹1.5 crore within 18 months

You have a large ITC balance that you would need to reverse on switching

You sell through e-commerce platforms covered under Section 52 TCS

The one calculation that decides everything:

(Your output GST - Your ITC) vs. (1% or 6% of turnover)

If the regular scheme net tax (output minus ITC) is lower than the composition flat rate, stay regular. If the composition rate is lower, switch. Do this calculation before every financial year.

Tools for Composition Scheme Compliance

Composition Scheme Calculator ➡️ Enter your annual turnover, purchase amount, and customer type breakdown. Get a side-by-side comparison of your tax liability under composition vs regular GST to make the right decision for your business.

GST Calculator ➡️ Calculate the exact tax under both schemes on any transaction amount.

Due Date Calendar ➡️ CMP-08 due dates for all four quarters plus GSTR-4 annual return deadline, all in one place.

ITC Reversal Calculator ➡️ Before switching to composition, calculate the exact ITC you must reverse on your closing stock under Rule 44 and ITC-03.

GST Registration Limit Calculator ➡️ Check whether you are below or above the threshold for your state and business type.

GSTIN Validator ➡️ Verify your GSTIN is correctly registered under the composition scheme after CMP-02 filing.

Penalty Calculator ➡️ Calculate late fees and interest for missed CMP-08 deadlines.

Related Articles on SmartGST

GSTR-2B Mismatch: Why Your ITC Is Blocked and How to Fix It ➡️ If you are evaluating regular GST vs composition, this article shows the full complexity of ITC reconciliation that composition dealers completely avoid.

GST 2.0 New Rate Structure 2025-26 ➡️ Rate changes under GST 2.0 affect the input cost calculation for composition dealers. Check whether your purchase costs changed.

GST for Freelancers India 2026 ➡️ If you are a freelancer or service provider, understand how the ₹50 lakh service composition threshold applies to you.

How to Download GST Certificate ➡️After registering under the composition scheme, download your updated GST registration certificate.

GST Registration Complete Guide ➡️ If exiting composition means upgrading your registration, this guide covers the amendment process.

References

Section 10, CGST Act, 2017 ➡️ Composition Levy

Section 10(2A), CGST Act, 2017 ➡️Composition scheme for service providers (amendment effective January 2020)

Rule 7, CGST Rules, 2017 ➡️ Tax rates under composition scheme

Rule 8, CGST Rules, 2017 ➡️ Intimation for composition levy (CMP-02)

Rule 9, CGST Rules, 2017 ➡️Validity of composition levy

Rule 44, CGST Rules, 2017 ➡️ ITC reversal on switching to composition (ITC-03)

CBIC Circular No. 77/51/2018-GST ➡️ Clarification on composition scheme issues

GSTN Portal Advisory on CMP-02 deadline, March 2026

GST Council 32nd Meeting Minutes, January 2019 ➡️ Service provider composition scheme introduction

Binary Semantics ➡️ GST Composition Scheme Complete Guide FY 2026-27, May 2026

One Decision Every March That Could Save You ₹2 Lakh a Year

The GST Composition Scheme is not the right choice for every business. But for a local retailer, a small manufacturer, or a neighbourhood restaurant with mostly walk-in customers, it is the most underused tax saving available under Indian law.

The catch is timing. You can only switch at the start of a financial year by filing CMP-02 before March 31. Miss that window and you wait another year.

Get the next CMP-02 deadline and every GST update that affects your business straight to your phone:

Content verified against Section 10 of CGST Act, 2017, CGST Rules 2017, and CBIC Circular No. 77/51/2018-GST. Last updated: 9 June 2026. Consult a CA before switching GST schemes — individual business circumstances vary significantly.