You Are Running a Business The GST Department Agrees

India has over 15 million freelancers. Most of them think of themselves as individuals earning from their skills. The GST law thinks of them as service providers running a business.

That distinction matters more than most freelancers realise. Once your annual income from freelancing crosses ₹20 lakh, GST registration is not optional it is mandatory. Miss that threshold and you owe back taxes, penalties, and interest from the day you crossed it.

But here is what the same GST law also gives you: if any of your clients are outside India, every rupee they pay you can be completely GST-free at 0% and you can still claim Input Tax Credit on your laptop, internet bill, and software subscriptions.

This guide covers every GST rule that applies to freelancers in India for FY 2025-26: registration thresholds, applicable rates, SAC codes for every major service category, how to file LUT for foreign clients, which expenses qualify for ITC, and how to file your returns without hiring a CA for every step.

Are You Actually Required to Register for GST?

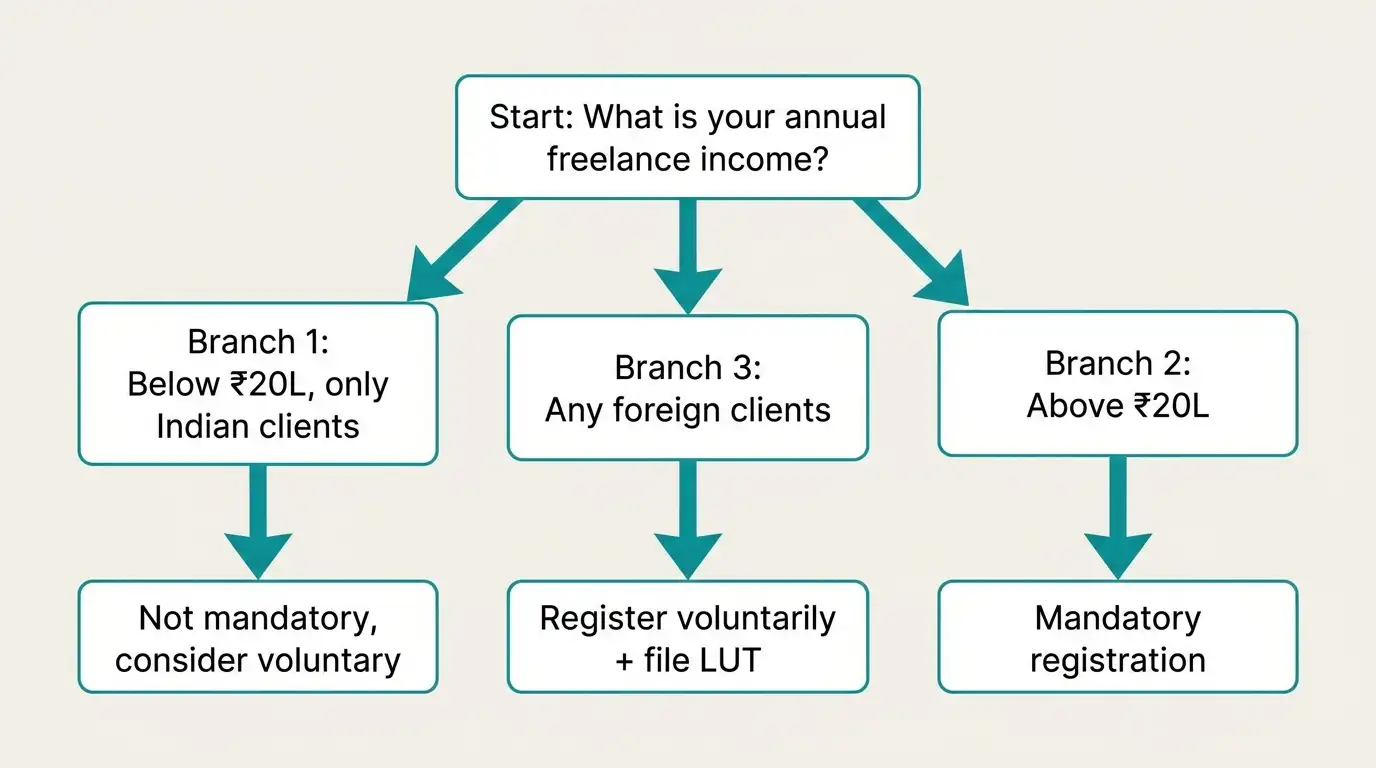

The answer depends on three things: your annual turnover, where your clients are, and which state you are in.

The ₹20 Lakh Threshold (Most Freelancers)

Under Section 22 of the CGST Act, 2017, GST registration becomes mandatory when your aggregate annual turnover from services exceeds ₹20 lakh in a financial year.

This threshold applies if:

All your clients are in India

You are based in most Indian states

Special category states have a lower threshold of ₹10 lakh these include Manipur, Mizoram, Nagaland, and Tripura. If you are based in these states, the lower limit applies to you.

Aggregate turnover includes all taxable services, zero-rated exports, and exempt supplies under the same PAN across India. It does not deduct expenses it is total receipts, not profit.

The Exception: If You Have Foreign Clients

Here is the rule that confuses most freelancers: even if your annual income is below ₹20 lakh, you may still need to register if you provide services to clients outside India.

Under Section 24 of the CGST Act, mandatory registration requirements apply to certain suppliers regardless of turnover. However, the export of services by freelancers below the ₹20 lakh threshold falls into a nuanced area and practically, voluntary registration is strongly recommended even below the threshold if you have foreign clients, because:

You cannot file a Letter of Undertaking (LUT) without registration which means you cannot export services as zero-rated without paying IGST upfront and waiting for a refund

Many international clients particularly US and UK companies require a GSTIN on your invoice for their own accounting

You can claim ITC on business expenses only if you are registered

Should You Register Voluntarily?

If your income is below ₹20 lakh and all clients are in India voluntary registration is optional. Weigh the ITC benefits against the compliance cost (monthly/quarterly returns) before deciding.

If you earn anything from foreign clients register voluntarily, immediately. The LUT benefit alone justifies it.

GST Rate for Freelance Services 18% on Most Everything

The GST rate on most professional and technical services is 18% split as 9% CGST + 9% SGST for services to Indian clients in the same state, or 18% IGST for services to clients in other states or outside India.

Under GST 2.0 (effective September 2025), this 18% rate remained unchanged for most service categories. The major rate overhaul affected goods more than services.

The exception: export of services to foreign clients

If your client is outside India and payment is received in convertible foreign currency, your service qualifies as an export of services under Section 2(6) of the IGST Act and is treated as zero-rated meaning GST rate is 0%. More on this in the LUT section below.

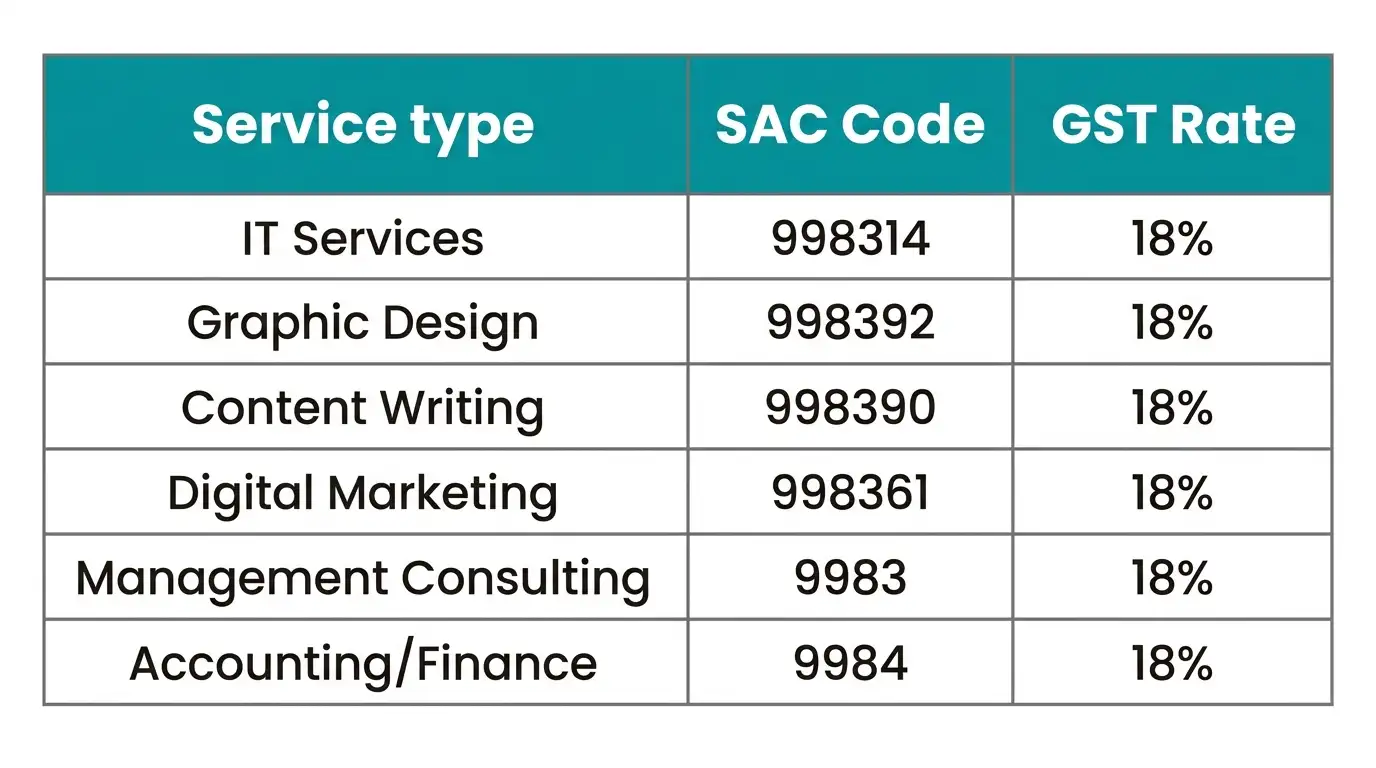

SAC Codes Which One Does Your Service Fall Under?

SAC (Service Accounting Code) is a 6-digit code you must declare on your GST invoice and in your GST returns. Using the wrong SAC code can trigger classification disputes during audits.

Here are the codes for the most common freelance service categories:

Service Type | SAC Code | GST Rate |

|---|---|---|

Software development, IT consulting | 998314 | 18% |

Website design and development | 998313 | 18% |

Graphic design and visual communication | 998392 | 18% |

Content writing, copywriting, editing | 998390 | 18% |

Digital marketing, SEO, social media | 998361 | 18% |

Management consulting, business advisory | 998311 | 18% |

Accounting and financial services | 998222 | 18% |

Video editing and production | 999612 | 18% |

Photography services | 999614 | 18% |

Training and coaching | 999293 | 18% |

Translation services | 998393 | 18% |

Legal consulting (non-CA/CS) | 998211 | 18% |

Market research | 998361 | 18% |

Architecture and engineering | 998311 | 18% |

Use the SmartGST HSN Finder to search your specific service by name if you do not see your category above the tool covers both HSN codes for goods and SAC codes for services.

The Most Valuable Rule for Freelancers With Foreign Clients LUT

A Letter of Undertaking (LUT) is the single most important GST document for Indian freelancers who work with international clients.

What LUT Does

Without LUT: You export services → you must either charge 18% IGST on the invoice (which a foreign client will not pay) or pay IGST yourself from your pocket → then claim a refund from GSTN, which takes 2–6 months.

With LUT: You export services → 0% GST on the invoice → no IGST paid upfront → no refund process.

LUT effectively makes your service exports completely tax-free and you can still claim ITC on your business expenses.

Who Can File LUT

Any registered GST taxpayer who has not been prosecuted for tax evasion exceeding ₹2.5 crore in the preceding year. For most freelancers, this is a formality you will almost certainly qualify.

How to File LUT Step by Step

Step 1: Login to gst.gov.in with your GSTIN.

Step 2: Navigate to Services → User Services → Furnish Letter of Undertaking (LUT).

Step 3: Select the financial year (file a fresh LUT for each FY it is not automatically renewed).

Step 4: Fill Form GST RFD-11 your GSTIN, tax period, details of witnesses (2 witnesses required, typically you and your CA or any two adults).

Step 5: Sign with DSC or EVC and submit. You receive a reference number immediately.

That's it. No physical submission. No approval waiting period. The LUT is valid for the entire financial year from the date of filing.

LUT must be filed every April for the new financial year. If you missed FY 2025-26 LUT, file immediately it can be filed any time during the year and is backdated to April 1.

How to Invoice Foreign Clients Under LUT

Your export invoice under LUT must include this mandatory line:

"Supply meant for export under LUT without payment of IGST."

The invoice should show:

Your GSTIN

Your LUT reference number

Client details (foreign address)

Service description and SAC code

Invoice amount in the agreed currency (USD, GBP, EUR, etc.)

Equivalent INR value (use RBI reference rate on invoice date)

GST: 0% (zero-rated export)

When you receive payment, keep the FIRC (Foreign Inward Remittance Certificate) from your bank this is proof that foreign currency payment was received, which is required if any ITC refund claim is ever scrutinized.

Input Tax Credit What Freelancers Can Claim

This is the hidden benefit of GST registration that most freelancers miss. Every GST-registered freelancer can claim ITC on business expenses reducing their effective tax cost.

What Qualifies for ITC

Expense | ITC Eligible? | Condition |

|---|---|---|

Laptop / desktop | Yes | Used exclusively for work |

Software subscriptions (Adobe, Figma, etc.) | Yes | Business use |

Internet / broadband bill | Yes | Business use |

Mobile phone and plan | Yes (50% for dual use) | Proportionate if personal too |

Office furniture (if dedicated home office) | Yes | Exclusively for work |

Professional development courses | Yes | Directly related to services provided |

Accountant / CA fees | Yes | Business expense |

Co-working space rent | Yes | If supplier is GST registered and charges GST |

Books, reference materials | Yes | Business-related |

What Does NOT Qualify for ITC

Expense | Why Not Eligible |

|---|---|

Personal travel | Section 17(5) blocked credit |

Gym membership, club fees | Section 17(5) blocked credit |

Food and beverages | Section 17(5) blocked credit |

Personal mobile expenses | Non-business use |

Home rent (unless exclusively a registered office) | Mixed personal/professional use |

Key rule: ITC is claimable only if the supplier is GST-registered and has uploaded the invoice in their GSTR-1, making it visible in your GSTR-2B. A receipt from an unregistered vendor or a personal expense carries no ITC.

Use the SmartGST ITC Eligibility Checker to verify before claiming any input credit in your return.

Which GST Returns Do Freelancers File?

Once registered, your filing obligations depend on your turnover and whether you are on the regular scheme or the QRMP scheme.

Regular Monthly Filers

GSTR-1 → Filed by the 11th of every month. Lists every invoice you raised to Indian clients that month with GST. For zero-rated exports under LUT, report in the Exports section.

GSTR-3B → Filed by the 20th of every month (or 22nd/24th depending on your state for turnover below ₹5 crore). Self-declaration of total taxable supply, output GST liability, ITC claims, and net tax payable.

QRMP Scheme (Quarterly Return Monthly Payment)

If your annual turnover is below ₹5 crore, you can opt for the QRMP (Quarterly Return, Monthly Payment) scheme:

File GSTR-1 quarterly instead of monthly

Pay tax monthly through a fixed payment (PMT-06) or self-assessment

File GSTR-3B quarterly

For most freelancers with relatively stable monthly income and few invoices, QRMP reduces your filing workload by 2/3rds. Check the SmartGST Due Date Calendar for exact dates under both schemes.

GSTR-9 (Annual Return)

If your annual turnover exceeds ₹2 crore, you must file GSTR-9 (annual reconciliation return) by December 31 of the following financial year. Below ₹2 crore, GSTR-9 is optional but recommended for clean records.

The Complete GST Invoice Format for Freelancers

A valid GST invoice from a freelancer must contain:

For Indian clients:

Your name, address, and GSTIN

Invoice number (sequential, unique per financial year)

Invoice date

Client name, address, and GSTIN (for B2B if client is GST registered)

Description of service and SAC code

Taxable value

GST rate (18%) and amount (CGST 9% + SGST 9% for same-state, or IGST 18% for inter-state)

Total invoice amount

Place of supply (must be stated for IGST/interstate transactions)

Your bank details (optional but standard practice)

For foreign clients (under LUT): All of the above except GST amount, plus:

Currency (USD/GBP/EUR etc.) and INR equivalent

LUT reference number

Line: "Supply meant for export under LUT without payment of IGST"

Port code (if applicable for specific FIRC linking)

FIRC reference (added once payment is received)

Use the SmartGST Invoice Generator to create GST-compliant invoices for both Indian and foreign clients without manual formatting.

Your GST Calendar as a Freelancer

Deadline | What to Do |

|---|---|

April 1 every year | File fresh LUT for new financial year (if you have foreign clients) |

11th of every month | File GSTR-1 (or quarterly under QRMP) |

20th/22nd/24th of every month | File GSTR-3B and pay any net GST |

14th of every month | Review GSTR-2B and reconcile with ITC claims |

December 31 | File GSTR-9 annual return (if turnover above ₹2 crore) |

Never miss a due date even if your tax liability is zero, nil returns must be filed to avoid late fees of ₹50 per day per return. Use the SmartGST Due Date Calendar to track all deadlines.

Tools That Make GST Compliance Easy for Freelancers

GST Calculator ➡️ Calculate your GST liability on any invoice instantly. Add or remove GST from quoted amounts.

Invoice Generator ➡️ Create GST-compliant invoices for Indian and foreign clients. Correct format, SAC codes, and tax calculation built in.

HSN Finder (SAC Codes for Services) ➡️ Search your service category by name and get the correct SAC code and applicable GST rate.

ITC Eligibility Checker ➡️ Verify which of your business expenses qualify for Input Tax Credit before filing.

GSTR-2B Reconciliation Tool ➡️ Match your vendor invoices against GSTR-2B to ensure only eligible ITC is claimed.

Due Date Calendar ➡️ All GST filing deadlines for FY 2025-26 in one place. Monthly and quarterly schedules.

GST Registration Limit Calculator ➡️ Enter your state and projected annual turnover to check whether registration is mandatory for your situation.

Penalty Calculator ➡️ Calculate late filing fees and interest if you have missed any return deadlines.

Related Articles

How to Verify a Fake GST Invoice 5 Checks in 30 Seconds ➡️ As a freelancer receiving payments, also verify any GST-registered vendors you pay (CA, co-working space, software vendors) to ensure your ITC claims are valid.

GST 2.0 New Rate Structure 2025-26 ➡️ While most freelance services remain at 18%, understand how GST 2.0 affects costs of services and products you buy as business inputs.

GST Invoice Management System (IMS) 2026 Guide ➡️ If you are registered and claiming ITC, IMS is now a mandatory monthly step before filing GSTR-3B.

How to File GSTR-3B ➡️ Step-by-step guide to the monthly return that every registered freelancer must file.

How to Claim a GST Refund ➡️ If you paid IGST on exports without LUT, this guide covers the refund claim process.

References

Section 22, CGST Act, 2017 Registration threshold for service providers

Section 24, CGST Act, 2017 Mandatory registration regardless of threshold

Section 2(6), IGST Act, 2017 Definition of export of services

Section 16, IGST Act, 2017 Zero-rated supply

Rule 96A, CGST Rules, 2017 LUT filing procedure

Form GST RFD-11 Letter of Undertaking format

CBIC Circular No. 161/17/2021-GST Clarification on export of services conditions

Section 17(5), CGST Act, 2017 Blocked credits

CBIC FAQ on QRMP Scheme ➡️ cbic.gov.in

Freelancing India Report 2025 NASSCOM 15 million freelancers, ₹20,000 crore market size

Get Every GST Update Before It Affects Your Next Invoice

GST rules for service exporters, LUT filing procedures, and ITC rules change. The CBIC issued 4 circulars specifically clarifying export of services rules in FY 2024-25 alone. Staying current means the difference between a clean return and an unexpected notice.

The SmartGST WhatsApp Channel explains every CBIC circular, GSTN advisory, and filing deadline in plain English within 24 hours.

Content verified against Section 22 of CGST Act, 2017, Section 16 of IGST Act, 2017, and CBIC clarifications on export of services. Last updated: 8 June 2026. Consult a CA for advice specific to your income structure and client mix.