If You Were Panicking About the 15 June E-Way Bill Deadline You Just Got 47 More Days

On 9 June 2026, GSTN issued Advisory No. 663 with a single operative line that thousands of businesses, GST Suvidha Providers, and ERP vendors had been waiting for:

"The mandatory capture of 'Ship To GSTIN' in Bill-To/Ship-To transactions and the Voluntary Closure of E-Way Bill functionality shall be implemented with effect from 1st August, 2026, instead of 15th June, 2026."

The two most significant changes to India's E-Way Bill system since 2018 have been postponed. The June 15 deadline which would have caused EWB generation to fail for any Bill-To/Ship-To transaction with a missing Ship-To GSTIN is no longer operative.

The new deadline is 1 August 2026.

This is not a full reprieve. It is 47 additional days to do what should have been done in May. Businesses, ERPs, and GSPs that used the June 15 urgency as motivation and completed their system updates can relax. Those who hadn't started yet should not treat this extension as permission to wait until July 30.

Here is everything you need to know about what changed, why it changed, and the exact actions required before the new deadline.

What Exactly Got Postponed The Two Features

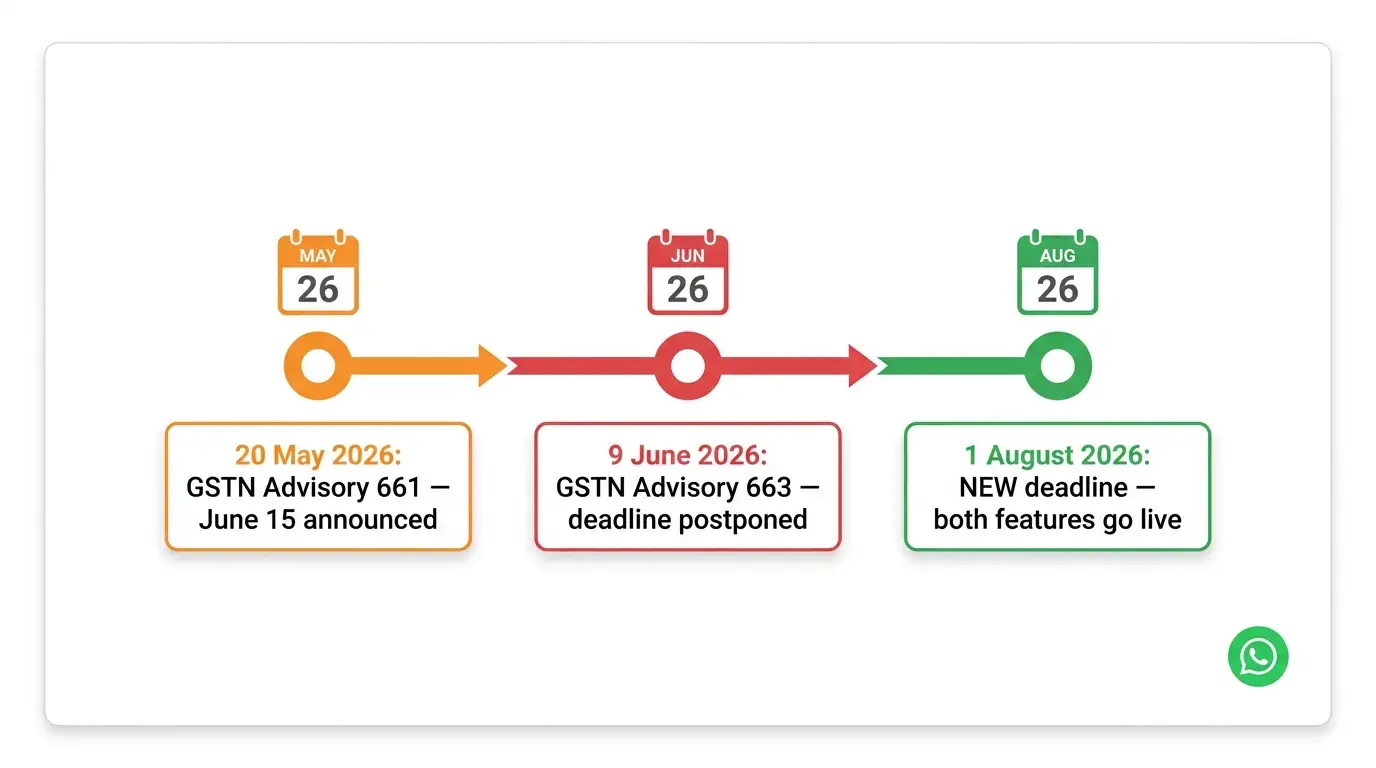

For context, both features were originally announced through GSTN Advisory No. 661 dated 20 May 2026 and were scheduled to go live on June 15, 2026. Both have now been moved to 1 August 2026 via Advisory No. 663 dated 9 June 2026.

Feature 1: Mandatory Ship-To GSTIN in Bill-To/Ship-To Transactions

What it is: In any e-Way Bill where the invoice party and the delivery party are different entities, the Ship-To GSTIN field will become mandatory. Until now it was optional.

Why it matters: If you generate EWBs for Bill-To/Ship-To transactions and leave the Ship-To GSTIN blank, your EWB generation will fail from 1 August 2026. Goods cannot move without a valid EWB. No EWB = delivery halted.

Who is affected:

Manufacturers who invoice Head Office but deliver to warehouse branches

Distributors who invoice a central buying entity but ship to individual retail outlets

E-commerce sellers using fulfillment center models

Construction material suppliers billing contractor HQ but delivering to project sites

URP rule: If the Ship-To party has no GSTIN (unregistered person), enter "URP" in the field. The portal accepts this. Do not leave blank.

Feature 2: Voluntary E-Way Bill Closure Facility

What it is: A new feature allowing the supplier, recipient, transporter, or driver to digitally "close" an EWB after goods are delivered creating a delivery confirmation record inside the GST system.

Why it matters: Currently, once an EWB is generated it stays active until expiry regardless of whether delivery happened. The closure feature creates an end-to-end digital trail: dispatch (EWB generated) → delivery (EWB closed).

Key rules that remain unchanged for 1 August:

Closure allowed on day of delivery or the immediately following day only (2-day window)

Once closed, EWB cannot be reopened or amended

This feature is voluntary no penalty for not using it, but GSTN has indicated future compliance requirements may build on this data

Why Was the Deadline Extended? The Real Reason

The decision came after GSTN received representations from trade bodies, industry associations, GST Suvidha Providers (GSPs), ERP vendors, and taxpayers highlighting the need for additional time to make necessary system modifications and complete testing activities.

Three specific readiness gaps were cited:

Gap 1 ➡️ ERP vendor API updates not complete The GSTN released updated Sandbox API specifications in May 2026. But ERP software vendors Tally, SAP, Oracle, Zoho, and dozens of smaller platforms needed time to build, test, and push updates to their production environments. Many vendors were not ready by June 15.

Gap 2 ➡️ Master data incomplete across large enterprises Businesses with hundreds of delivery locations needed to collect and verify the GSTIN of each Ship-To location and update it in their customer master data. For companies with 500+ Ship-To locations, this is not a one-day task.

Gap 3 ➡️ GSP system readiness GST Suvidha Providers who power bulk EWB generation for large industries needed additional testing time to validate that their bulk-generation flows correctly capture and transmit Ship-To GSTIN data for each transaction.

GSTN stated that both functionalities will be effective from the new date and urged all stakeholders to take advantage of the extended timeline for readiness and compliance.

The extension is not an indication that the requirement itself has changed or softened. Both features will become mandatory on 1 August 2026. The expectation is that the extra time is used for preparation not postponement of preparation.

What This Means for Your Business Right Now

If You Had Already Completed Your System Updates

The changes are active in the Sandbox testing environment for ERP networks. If your ERP vendor has already deployed the production update and your Ship-To GSTIN master data is complete, there is nothing further to do before August 1. Your system will work correctly when the portal goes live.

You may, however, want to use the extended period to:

Do a trial run of EWB generation with Ship-To GSTIN populated

Train your billing and logistics teams on the new mandatory field

Set up the EWB Closure process in your delivery workflow

If You Had Not Started

The extension gives you 47 days. Taxpayers, GSPs, ERP providers and other stakeholders should ensure all required system updates, testing, and operations are completed in time for the revised implementation date of August 1, 2026.

Here is a realistic timeline for what still needs to happen:

Week | Action | Who |

|---|---|---|

Now ➡️ 20 June | Identify all Bill-To/Ship-To transaction patterns in your business | Finance/Operations |

20 June ➡️ 5 July | Collect Ship-To GSTINs for all delivery locations. Mark "URP" for unregistered. | Accounts team |

5 July ➡️ 15 July | Update customer master in ERP with Ship-To GSTINs | IT/System admin |

15 July ➡️ 22 July | Contact ERP vendor confirm API update is deployed in production | IT/Finance head |

22 July ➡️ 28 July | Test EWB generation with Ship-To GSTIN field populated generate 5-10 sample EWBs | Finance team |

28 July ➡️ 31 July | Train billing staff. Set up EWB Closure post-delivery workflow. | Operations |

1 August 2026 | System goes live. Ship-To GSTIN mandatory. | All |

The Penalty Clock Does Not Reset

The extension is for preparation time, not penalty forgiveness. From 1 August 2026, if an EWB is generated for a Bill-To/Ship-To transaction without a Ship-To GSTIN, the portal will reject generation entirely.

If goods move without a valid EWB:

Detention of goods and conveyance under Section 129 of CGST Act

Penalty: ₹10,000 or tax sought to be evaded, whichever is higher

Interest at 18% per annum on the tax value of intercepted goods

There is no warning period, no grace window, no "advisory mode" post-August 1. The hard block goes live on the new date just as it would have on the old one.

How This Affects the Earlier SmartGST E-Way Bill Article

If you read our earlier guide published before this extension E-Way Bill New Rules June 2026: Ship-To GSTIN Mandatory the complete technical content of that article remains accurate. The compliance requirements, penalty provisions, step-by-step filing process, and action checklist are unchanged.

The only update is the date: 15 June 2026 → 1 August 2026 for both features.

All businesses that were preparing should continue preparing. All businesses that had not started should use this article as the updated starting point.

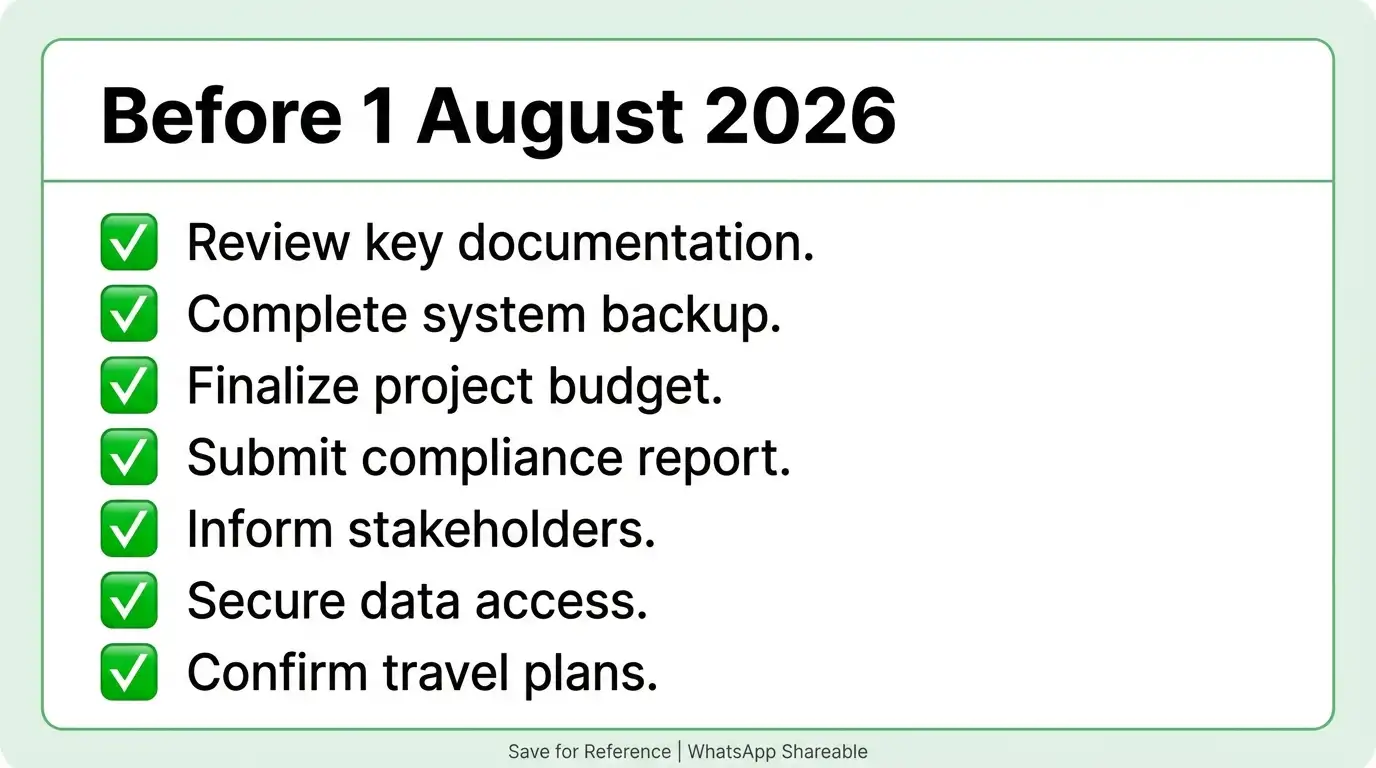

Complete Updated Action Checklist Before 1 August 2026

Tick these off over the next 7 weeks:

☐ Identify Bill-To/Ship-To transactions ➡️ Pull last 3 months of EWBs and identify any where the "Ship To" address and "Bill To" address are different entities

☐ List all Ship-To locations ➡️ For each delivery location that is a different entity from the invoice party, collect their GSTIN. For unregistered locations, mark "URP"

☐ Update customer/vendor master ➡️ Add Ship-To GSTIN to the relevant records in your ERP or billing software

☐ Contact ERP/GSP vendor ➡️ Confirm the updated API for Ship-To GSTIN is deployed in your production environment, not just Sandbox

☐ Test EWB generation ➡️ Generate 5 test EWBs with the new mandatory Ship-To GSTIN field populated before August 1. Verify the portal accepts them

☐ Set up EWB Closure workflow ➡️ Create an internal process where the delivery confirmation step includes closing the EWB on the portal or via mobile app. Train the team or driver responsible

☐ Update supplier/partner communication ➡️ Notify any vendors or logistics partners who generate EWBs on your behalf that Ship-To GSTIN is mandatory from August 1

Tools for E-Way Bill Compliance

E-Way Bill Validity Calculator ➡️ Calculate EWB validity period based on distance and transport mode. Updated for 2026 rules.

Bulk GSTIN Validator➡️ Validate all your Ship-To GSTINs in one batch before updating your master data. Catch inactive or cancelled GSTINs before they cause EWB rejection.

GSTIN Validator ➡️ Individual GSTIN verification for any specific Ship-To party.

GST Registration Status ➡️ Check Active/Suspended/Cancelled status of a GSTIN before adding it to your Ship-To master.

GST Compliance Checklist ➡️ Full FY 2026-27 compliance checklist including E-Way Bill, IMS, and GSTR-3B filing requirements.

GST Notice Reply Generator ➡️ If an EWB-related interception notice has already been issued, draft your response here.

Related Articles

E-Way Bill New Rules June 2026 Complete Guide ➡️ The complete technical guide to Ship-To GSTIN and EWB Closure. All content remains valid only the date has changed to 1 August 2026.

GST Invoice Management System (IMS) Mandatory Guide 2026 ➡️ IMS and EWB changes are complementary both build end-to-end transaction traceability in the GST system.

GSTR-2B Mismatch: ITC Blocked, How to Fix It ➡️ EWB data feeds ITC reconciliation. Ship-To GSTIN captures directly affect GSTR-2B ITC matching for Bill-To/Ship-To transactions.

How to Verify a Fake GST Invoice ➡️ Before adding Ship-To GSTINs to your master, verify each one is active. A single invalid GSTIN in your master will cause EWB rejection on August 1.

GSTAT Appeal Deadline 30 June 2026 ➡️Another June deadline that was not extended. If you have GST demand orders, that window closes 30 June ➡️ no postponement.

References

GSTN Advisory No. 663 dated 9 June 2026 Extension of E-Way Bill implementation timeline gst.gov.in/newsandupdates/read/663

GSTN Advisory No. 661 dated 20 May 2026 Original announcement of Ship-To GSTIN and EWB Closure

Rule 138, CGST Rules, 2017 ➡️ E-Way Bill generation requirements

Section 129, CGST Act, 2017 ➡️ Detention and penalty for goods moving without EWB

Rule 138E, CGST Rules, 2017 ➡️ Blocking of EWB generation for GSTR-3B defaulters

GSTN Sandbox API Documentation ➡️ Ship-To GSTIN field specifications, May 2026

47 Days Is Enough. But Only If You Start Today.

Industry bodies won the extension by arguing that businesses needed more time. GSTN gave it. Now the obligation is on every business that was not ready to use these 47 days properly.

August 1 will not be extended again. The representations that worked for June 15 will not work twice. The API is already in Sandbox. The specification is published. The only remaining variable is whether your system is updated and your team is trained.

Every GST portal update, CBIC advisory, and compliance change explained in plain English within 24 hours:

Content verified against GSTN Advisory No. 663 dated 9 June 2026 and GSTN Advisory No. 661 dated 20 May 2026. Last updated: 12 June 2026.