You Have 7 Days to Update Your E-Way Bill Process Or Face Failed EWB Generation

On 15 June 2026, two significant changes go live on India's e-Way Bill portal. One is mandatory. The other is voluntary but introduces a feature that has been missing from the system since 2017.

If your business moves goods across India as a manufacturer, trader, transporter, or distributor and you use Bill-To/Ship-To transactions (invoice raised on one party, goods delivered to another), you have seven days to update your process.

Miss the 15 June deadline and e-Way Bills for your Bill-To/Ship-To transactions will fail to generate on the portal. No EWB, no movement. Goods stuck at the warehouse.

This guide tells you exactly what is changing, who is affected, what URP means for unregistered consignees, and the precise steps to update your billing system before the deadline.

Background Why GSTN Is Making This Change

The e-Way Bill system has been operational since April 2018. In those eight years, one gap persisted: in Bill-To/Ship-To transactions, the portal had no way to verify where goods actually went. The invoice party and the delivery party could be completely different entities and as long as the EWB was generated with the invoice party's GSTIN, the system had no record of who actually received the goods.

This created a real compliance and fraud risk. Goods could be diverted mid-transit without any GST trail. Classification disputes arose about whether the actual delivery constituted a new taxable supply. ITC claims were filed by the invoice party for goods that physically never entered their premises.

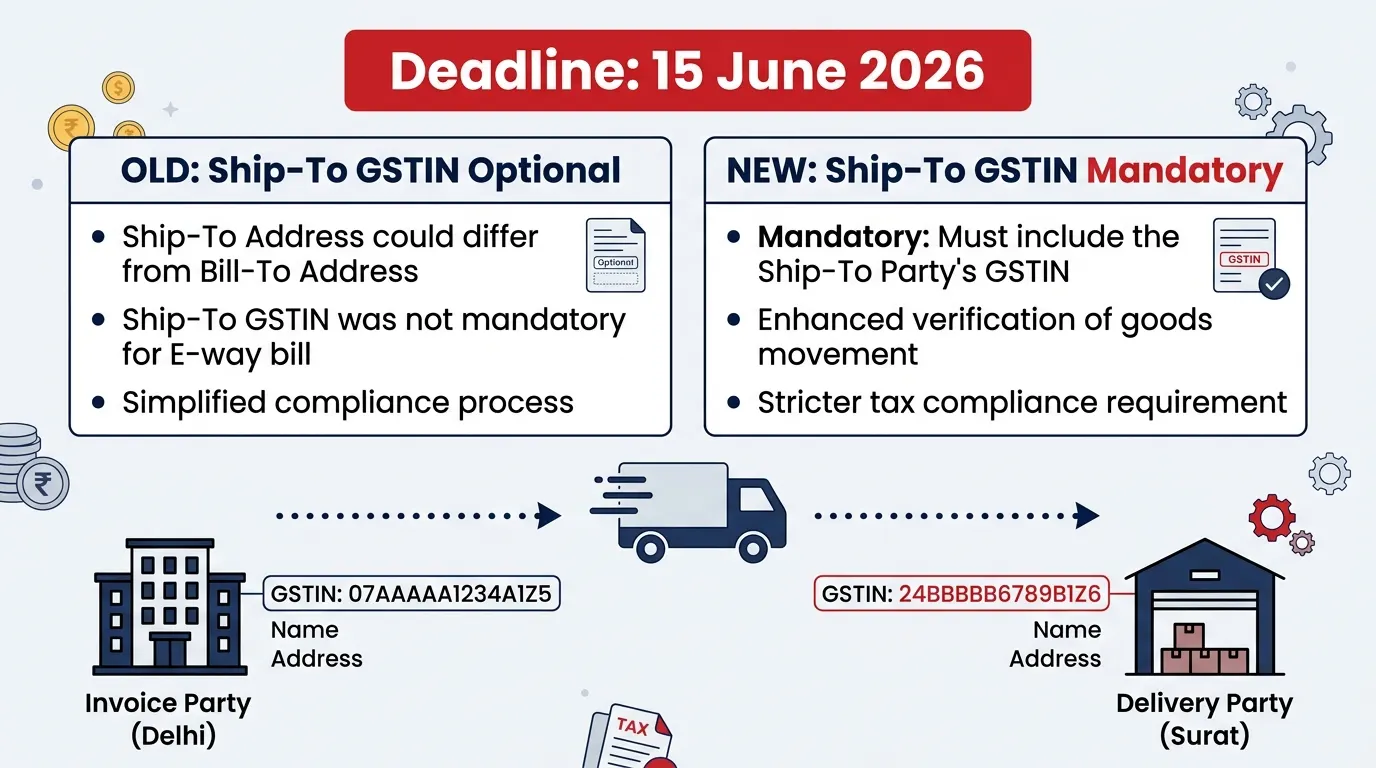

GSTN Advisory No. 661, dated 21 May 2026, addresses this directly. From 15 June 2026, the Ship-To GSTIN is a mandatory field. Every e-Way Bill for a Bill-To/Ship-To transaction must carry the GSTIN of the actual delivery location not just the invoice party.

Change 1 Ship-To GSTIN: Now Mandatory (Not Optional)

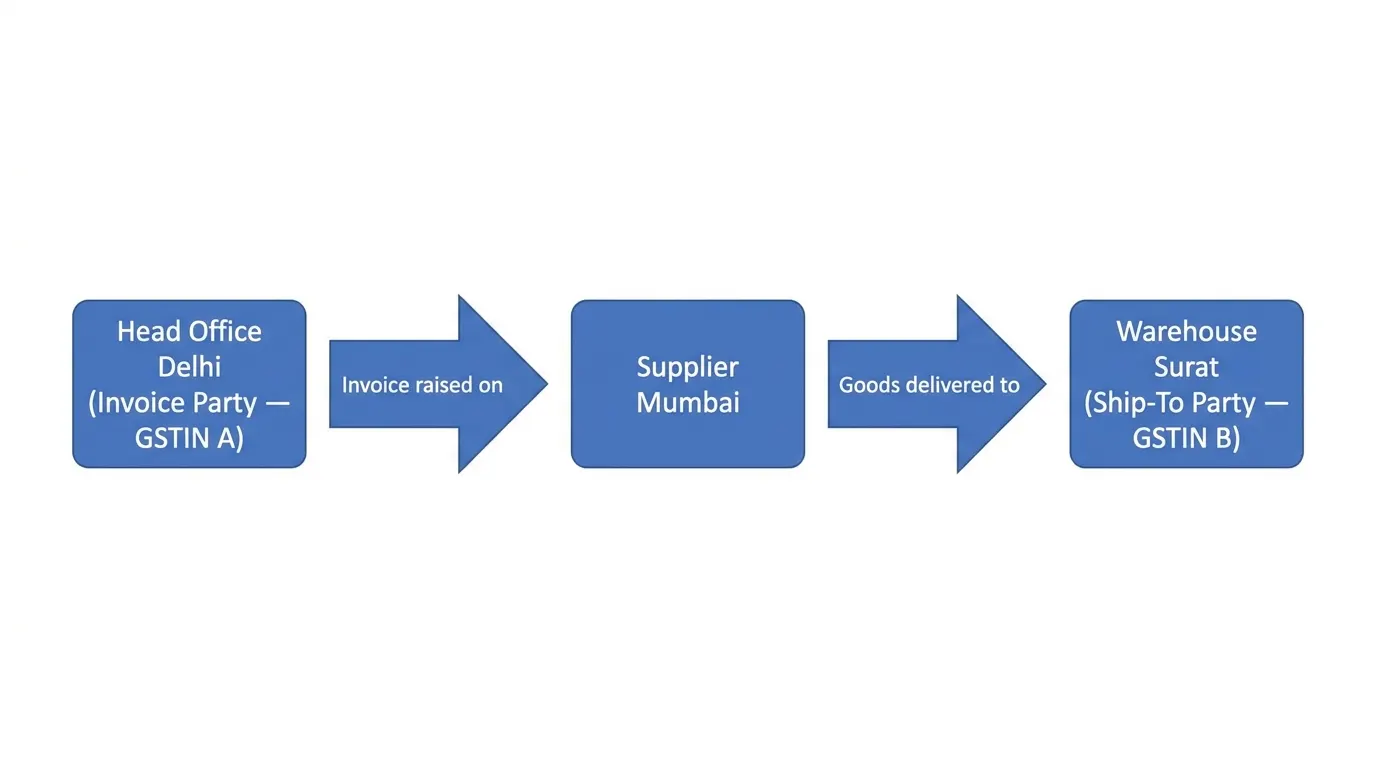

What Is a Bill-To/Ship-To Transaction?

This is any transaction where the party named on the invoice is different from the party that physically receives the goods.

Real-world example: A retail chain's procurement team in Bengaluru places an order and receives the invoice. But the goods say, 500 cartons of packaged foods travel directly to the chain's distribution centre in Nagpur. The supplier raises one invoice (to Bengaluru GSTIN) but generates an e-Way Bill for delivery to Nagpur.

Until now, the Nagpur GSTIN could be left blank in the EWB. From 15 June 2026, it cannot.

What Exactly Must You Enter?

Scenario | What to Enter in Ship-To GSTIN Field |

|---|---|

Ship-To party is GST registered | Enter their valid 15-digit GSTIN |

Ship-To party is unregistered (no GSTIN) | Enter "URP" (Unregistered Person) |

Ship-To is your own branch (same PAN, different state) | Enter the branch's GSTIN |

Ship-To is your own warehouse (same GSTIN) | Enter the same GSTIN as Bill-To |

Ship-To is a government entity exempt from registration | Enter "URP" |

The URP clarification is critical. Many businesses panicked when GSTN first announced this change because their consignees small retailers, individual buyers, government warehouses do not have GST registrations. GSTN explicitly addressed this: where the consignee is unregistered, enter "URP" and the portal will accept it.

Penalty for Non-Compliance

Incorrect declaration in the Ship-To GSTIN field is treated as a misstatement under Section 122 of the CGST Act. The penalty is ₹10,000 or the tax sought to be evaded, whichever is higher.

More immediately: if the field is left blank after 15 June 2026, the portal will reject EWB generation entirely. Your goods cannot move without a valid EWB.

What Businesses Must Do Right Now

If you generate EWBs manually on the portal: No system change needed. Simply train your team to enter the Ship-To GSTIN when filling EWB Part A. The field will become mandatory the portal will not let you proceed without it.

If you use ERP or accounting software (Tally, Zoho, SAP, Oracle): Contact your software vendor immediately. The API specifications have been updated by NIC and are live in the Sandbox environment. Your vendor must deploy the updated API integration before 15 June 2026. If they have not already sent you an update notification, call them today.

If you use a GSP (GST Suvidha Provider) or ASP for bulk EWB generation: Your GSP should have already tested against the updated Sandbox API. Confirm with them in writing that the Ship-To GSTIN field is mapped in their system and that production deployment is scheduled before 15 June.

Use the SmartGST E-Way Bill Validity Calculator to check validity periods on EWBs generated before 15 June any EWBs generated with the old format (Ship-To GSTIN blank) will still be valid for their original validity period.

Change 2 E-Way Bill Closure Facility (Voluntary, But Use It)

This is the more operationally interesting change and one that most businesses have not fully understood yet.

What Problem Does EWB Closure Solve?

Until now, once an e-Way Bill was generated, it served one purpose: to accompany the goods in transit. Once delivery was complete, the EWB simply expired after its validity period. There was no way to officially record on the GST system that the goods had actually been delivered.

This created a documentation gap. If a tax officer later questioned a transaction, you had the EWB showing goods were dispatched but no system record of delivery completion. You had to rely on physical delivery receipts, which could be challenged.

The EWB Closure feature creates a digital delivery confirmation record inside the GST system itself.

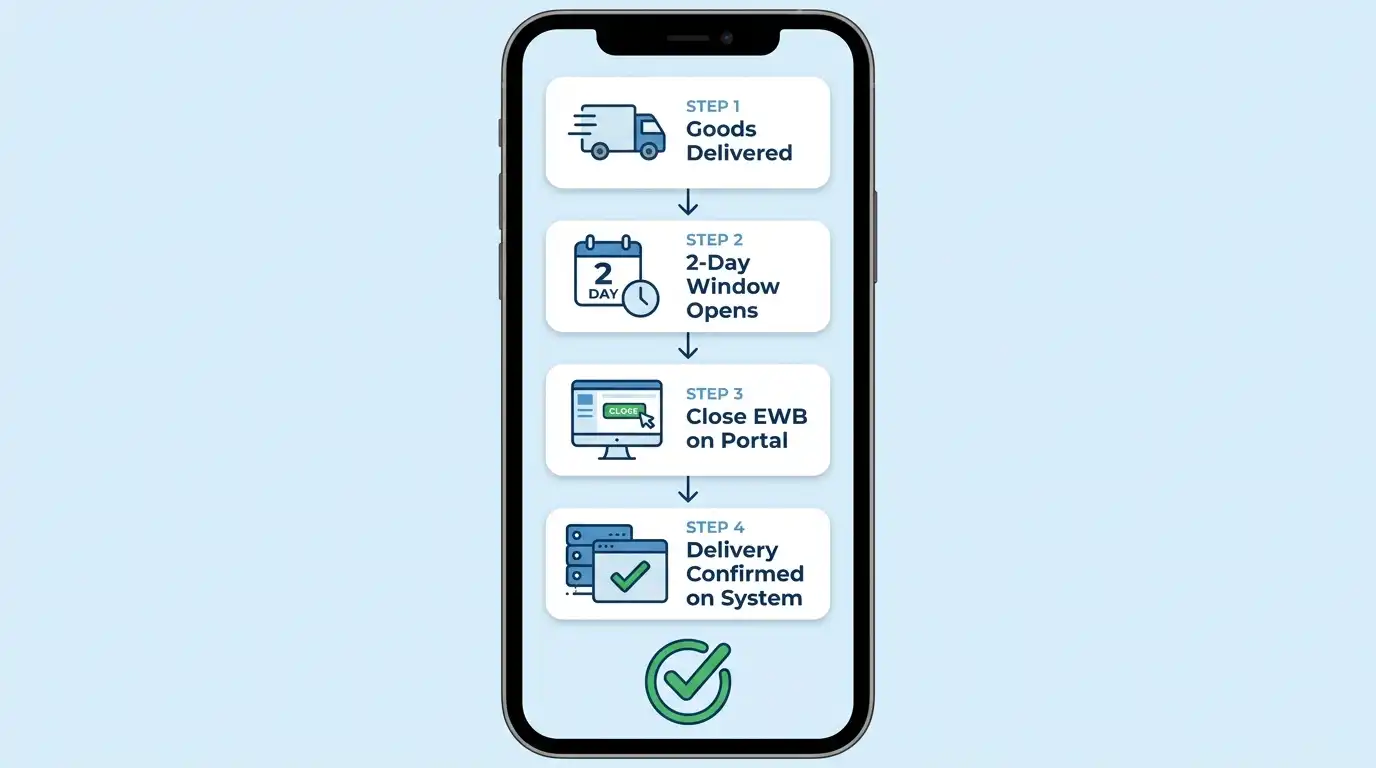

How EWB Closure Works

Once goods are delivered, any of the following parties can close the EWB:

The supplier who generated it

The recipient who received the goods

The transporter

The driver (whose mobile number was registered on the EWB)

Any authorized person nominated during EWB generation

The 2-day window rule: You can only close an EWB on the same day of delivery or the next day. The system locks closure after 48 hours. This is not a generous window it requires your delivery confirmation process to be near-real-time.

Closure is permanent: Once closed, the EWB cannot be reopened or amended. If you close it in error, you will need to generate a fresh EWB for any further movement of the same goods.

Closure is different from cancellation: Cancellation means the EWB was wrongly generated (before movement started). Closure means delivery is successfully complete (after movement ended).

Why You Should Use It Even Though It Is Voluntary

GSTN Advisory 661 includes a line that most people skipped: "the data generated from the voluntary closure facility may form the basis for future compliance requirements or investigations."

That sentence is telling you something. The government is building a delivery confirmation database. Today it is voluntary. The pattern with GST compliance features e-invoicing, IMS, GSTR-2B is that voluntary features become mandatory within 12–18 months of launch.

Start using EWB Closure now. Build the process into your delivery workflow. When it becomes mandatory, you will already be compliant and your competitors who ignored it will be scrambling.

Who Is Affected And Who Is Not

Affected:

Manufacturers who supply goods directly to distributors' branch locations or warehouses while invoicing the head office

Traders and distributors who deliver to multiple retail points but bill a central buying entity

E-commerce sellers who ship to customer addresses while invoicing marketplace entities

Pharmaceutical distributors delivering to hospital branches or government health centres while invoicing state health departments

Construction material suppliers delivering to project sites while invoicing contractor head offices

Not Affected by Ship-To GSTIN Change:

Businesses where the invoice party and the delivery address are always the same entity (standard transactions)

Transactions below the ₹50,000 e-Way Bill threshold

Job work transactions though separately note that job work has its own EWB rules under Rule 55A

If you are unsure whether your business does Bill-To/Ship-To transactions, pull your last 10 EWBs and check whether the "Ship To" state and "Bill To" state or GSTINs are ever different. If yes, this change applies to you.

Step-by-Step: Generating an E-Way Bill After 15 June 2026

For businesses that do Bill-To/Ship-To transactions, here is the updated flow:

Step 1 ➡️ Log into the EWB portal Go to ewaybillgst.gov.in and log in with your GST credentials.

Step 2 ➡️ Select "Generate New EWB" Navigate to e-Waybill → Generate New.

Step 3 ➡️ Fill Part A Transaction Details

Transaction Type: Select "Bill To / Ship To"

Bill To: Enter invoice party GSTIN and address

Ship To: Enter actual delivery GSTIN (or "URP" if unregistered)

HSN, product details, value same as before

Step 4 ➡️ Enter Ship-To GSTIN (NEW Mandatory Field) This field is no longer optional. Enter the 15-digit GSTIN of the actual delivery location. If unregistered, type "URP".

Step 5 ➡️ Fill Part B Transporter Details Vehicle number, transporter ID unchanged from current process.

Step 6 ➡️ Generate and Download EWB number generated. Share with transporter and driver.

Step 7 ➡️ After Delivery: Close the EWB (Optional but Recommended) Within the same day or next day of delivery, log back into the portal → EWB number → Close EWB → Confirm delivery. Screenshot the closure confirmation for your records.

The Bigger Picture Where E-Way Bill Compliance Is Heading

The Ship-To GSTIN change and EWB Closure feature are part of a broader GSTN effort to build end-to-end traceability of goods movement. When both are fully operational and the closure data starts flowing, the government will have, for the first time, a complete digital trail: goods dispatched (EWB generated) → goods delivered (EWB closed) → ITC claimed (GSTR-2B) → tax paid (GSTR-3B).

Gaps in this trail goods dispatched but no delivery confirmation, ITC claimed without matching EWB closure will become visible as discrepancy signals. Businesses that use the closure feature from Day 1 will have cleaner compliance records.

The Invoice Management System (IMS), which became mandatory from April 2026, is the other half of this picture it ensures ITC is claimed only on invoices you have explicitly reviewed and accepted. Together, IMS and the new EWB rules build a compliance environment where unverified ITC claims become much harder to sustain.

Check your overall GST compliance health using the SmartGST GST Health Score tool it flags common risk areas including EWB and ITC management gaps.

Action Checklist Before 15 June 2026

Action | Who Does It | Deadline |

|---|---|---|

Identify all Bill-To/Ship-To transactions in your business | Finance / Operations team | Today |

Collect GSTINs of all Ship-To locations | Accounts team | By 10 June |

Update customer master in ERP with Ship-To GSTINs | System admin / ERP vendor | By 12 June |

Confirm API update with GSP / ERP vendor | IT / Finance head | By 13 June |

Train billing staff on new mandatory field | Finance head | By 14 June |

Test one EWB generation on the portal with new field | Finance team | By 14 June |

Set up internal process for EWB Closure post-delivery | Operations team | By 15 June |

Useful SmartGST Tools for E-Way Bill Compliance

E-Way Bill Validity Calculator ➡️ Calculate EWB validity period based on distance and transport mode. Updated for 2025-26 rules.

GSTIN Validator ➡️ Before entering Ship-To GSTINs in your EWBs, verify each one is active and correctly formatted.

Bulk GSTIN Validator ➡️ If you have 50+ delivery locations, validate all Ship-To GSTINs in one go before updating your master data.

GST Registration Status ➡️ Check if a consignee's GSTIN is Active, Suspended, or Cancelled before generating the EWB.

GST Compliance Checklist ➡️ Full GST compliance checklist for FY 2025-26 including EWB and IMS requirements.

GST Notice Reply Generator ➡️ If you have received a notice related to EWB non-compliance, use this to draft a structured response.

Related Guides and Articles

GST Invoice Management System (IMS) Complete Guide 2026 ➡️ IMS became mandatory from April 2026 and directly affects how ITC flows from EWB-backed transactions. Read this alongside the EWB changes.

How to Generate an E-Way Bill Step by Step ➡️ Full guide to EWB generation including Part A, Part B, extension, and cancellation.

GSTR-2B Reconciliation Tool Guide ➡️ EWB data feeds into your GSTR-2B reconciliation. Understand how the new Ship-To GSTIN requirement affects ITC matching.

GST 2.0 New Rate Structure 2025-26 ➡️ If you are updating your EWB process, also audit your GST rate classification under the new structure.

GSTAT Appeal Deadline 30 June 2026 ➡️ If any of your past EWB non-compliance resulted in a GST demand order, this deadline matters to you.

References

GSTN Advisory No. 661 dated 21 May 2026 Enhancements in E-Way Bill System ➡️ gst.gov.in

Rule 138 of CGST Rules, 2017 E-Way Bill generation requirements

Section 68 of CGST Act, 2017 Inspection of goods in movement

Section 122 of CGST Act, 2017 Penalty for misstatement in EWB

NIC API Update Documentation Sandbox release, May 2026 ➡️ ewaybillgst.gov.in

CBIC Instruction on Bill-To/Ship-To transactions Clarification on ITC eligibility

West Bengal Notification ₹50,000 intrastate EWB threshold effective 1 June 2026

Stay Ahead of Every GST Deadline

The 15 June e-Way Bill changes are confirmed. But GST portal updates do not stop here GSTN pushes advisories, CBIC issues circulars, and the GST Council meets regularly with new decisions that affect your business.

The SmartGST WhatsApp Channel covers every update within 24 hours explained in plain English with specific action steps for businesses.

No spam. No generic news. Just GST updates that require action from your business.

Content verified against GSTN Advisory No. 661 dated 21 May 2026 and CBIC e-Way Bill rules under Rule 138 of CGST Rules, 2017. Last updated: 8 June 2026. Verify current requirements at ewaybillgst.gov.in before making compliance changes.