A Surat Textile Exporter Filed Every Monthly Return on Time for 3 Years. Then His FY 2022-23 Annual Return Gap Came Back to Haunt Him.

His GSTR-1 and GSTR-3B were impeccable filed by the 11th and 20th every single month without fail. No late fees. No pending returns. His CA was satisfied.

What nobody had flagged: his GSTR-9 for FY 2022-23 was never filed. Not because he was non-compliant intentionally his turnover was below the then-mandatory threshold and he assumed optional meant ignorable.

In January 2026, the GST portal's 3-year filing cap went live. Returns more than three years past their due date were permanently blocked. GSTR-9 for FY 2022-23 was due December 31, 2023. January 2026 was exactly 25 months past that deadline well within the 3-year window.

But he had never filed it. The portal flag appeared in his AIS (Annual Information Statement). The Income Tax department cross-check against his GST data showed an unfiled annual return. A notice arrived in February 2026.

This story plays out across thousands of businesses every year. GSTR-9 is the return most businesses treat as optional until it becomes a problem. For FY 2025-26, the stakes are higher than ever a missed GSTR-9 now blocks your monthly GSTR-3B filings for the following year, making it impossible to run your normal compliance cycle.

This guide covers exactly who must file GSTR-9 for FY 2025-26, what changed in this year's form, the new blocking rule, the step-by-step filing process, and every common error that generates a post-filing notice.

What Is GSTR-9 And Why It Exists

GSTR-9 is the annual return under Section 44 of the CGST Act, 2017. It is a consolidated summary return that covers the entire financial year pulling together all outward supplies (from GSTR-1), all inward supplies and ITC (from GSTR-2B and GSTR-3B), and reconciling them into a single annual document.

Think of it as the annual accounts of your GST compliance. Your monthly GSTR-1 and GSTR-3B are the monthly ledger entries. GSTR-9 is the final balance sheet for the year.

The return exists for two reasons. First, it gives the department a single document to audit your entire year's GST activity rather than reviewing 24 separate returns. Second, it gives businesses a final opportunity to correct errors, undisclosed supplies, and ITC mismatches that accumulated across 12 months as long as those corrections happen before filing GSTR-9 and before the November 30 ITC expiry date.

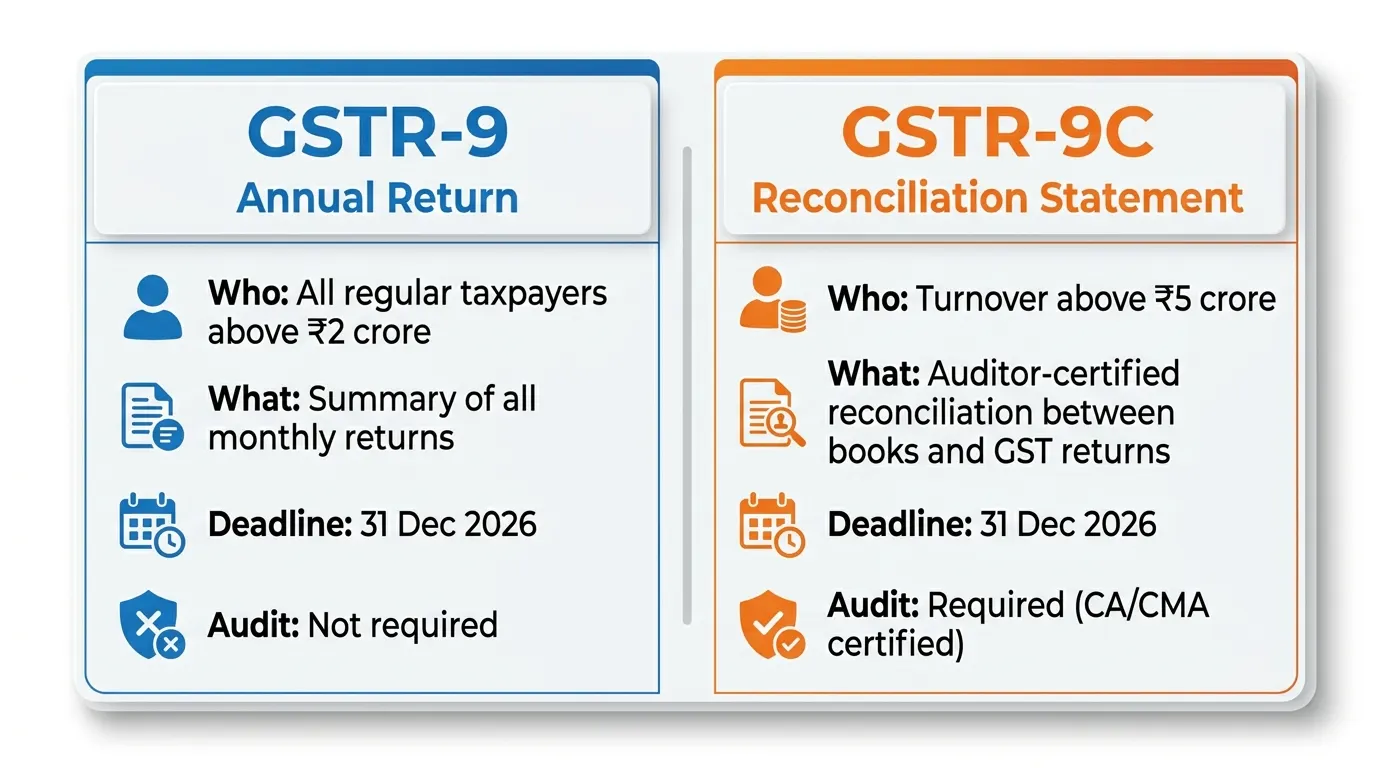

GSTR-9 vs GSTR-9C The Critical Difference

Feature | GSTR-9 | GSTR-9C |

|---|---|---|

What it is | Annual return GST-based summary | Reconciliation statement books vs GST |

Who files | All regular GST taxpayers above ₹2 crore | Taxpayers above ₹5 crore turnover |

Certification | Self-certified by taxpayer | Certified by CA or CMA |

Basis | GST portal data | Financial books of accounts |

Due date | 31 December 2026 (FY 2025-26) | 31 December 2026 (same) |

Key content | Outward supplies, ITC availed, taxes paid | Reconciliation of turnover, ITC, tax between books and returns |

GSTR-9C is filed along with GSTR-9 they are not separate submissions. If you are above ₹5 crore, your CA prepares GSTR-9C and you upload it as part of the GSTR-9 filing process.

Who Must File GSTR-9 for FY 2025-26

Mandatory (No Choice)

Turnover above ₹2 crore: GSTR-9 is mandatory. Based on CBIC Notification 14/2024 and the pattern of annual notifications, the ₹2 crore threshold has been maintained for FY 2025-26. Filing is compulsory.

Composition dealers: File GSTR-9A (not GSTR-9) regardless of turnover. GSTR-9A is the composition-specific annual return.

GSTR-9C (additional for turnover above ₹5 crore): A CA or CMA-certified reconciliation statement is required alongside GSTR-9.

Optional (But Strongly Recommended)

Turnover up to ₹2 crore: GSTR-9 is optional. But "optional" does not mean "useless" three strong reasons to file even below ₹2 crore:

The GSTN portal cross-references AIS data against GST filings. A missing annual return for a business with significant turnover activity flags in automatic analytics even if turnover is technically below mandatory threshold

ITC discrepancies identified during the year can only be formally reconciled in GSTR-9. Without filing, the discrepancy stays open and can generate notices years later

From FY 2025-26 onwards, a pending annual return blocks your FY 2026-27 GSTR-3B filings even for taxpayers who are technically in the optional bracket (the portal system does not always distinguish)

Who Does NOT File GSTR-9

Taxpayers under the Composition Scheme (they file GSTR-9A instead)

Input Service Distributors (ISD)

Non-resident taxable persons

Casual taxable persons

Persons paying TDS under Section 51

E-commerce operators paying TCS under Section 52

The New Rule That Changes Everything Annual Return Now Blocks Monthly Returns

This is the most significant change for FY 2025-26 and onwards:

From April 2026, a pending GSTR-9 (Annual Return) and GSTR-9C (Reconciliation Statement) for FY 2025-26 will block all FY 2026-27 monthly GSTR-3B filings on the portal.

Let that sink in. If you do not file GSTR-9 for FY 2025-26 by 31 December 2026, the GST portal will prevent you from filing your GSTR-3B for January 2027, February 2027, and every subsequent month until the annual return is filed.

A blocked GSTR-3B means:

Your output tax is undeclared you are technically non-compliant from January 2027

Late fee: ₹50/day per return (₹25 CGST + ₹25 SGST), capped at ₹5,000 per return

18% interest per annum on any unpaid tax from the due date

E-Way Bill generation blocked after two consecutive GSTR-3B defaults under Rule 138E your goods movement halts

The cascade effect of a missed annual return hitting monthly compliance is new as of FY 2025-26. Previous years allowed annual return delays with only direct late fees. Now the secondary impact cascading monthly filing blocks makes December 31 a truly hard deadline.

The 3-Year Filing Cap What Irreversible Losses Look Like

From FY 2025-26 onwards, the GST portal now prevents filing any return more than three years past its due date.

This cap, implemented on the portal from January 2026, means:

Financial Year | GSTR-9 Due Date | 3-Year Cap Date | Status (June 2026) |

|---|---|---|---|

FY 2022-23 | 31 Dec 2023 | 31 Dec 2026 | Still fileable but deadline approaching |

FY 2023-24 | 31 Dec 2024 | 31 Dec 2027 | Fileable |

FY 2024-25 | 31 Dec 2025 | 31 Dec 2028 | Fileable |

FY 2025-26 | 31 Dec 2026 | 31 Dec 2029 | Currently open for filing |

Critical: If your GSTR-9 for FY 2022-23 is still unfiled, you have until 31 December 2026 six months from now. After that, it is permanently blocked. Any ITC reconciliation, turnover correction, or tax adjustment for that year becomes impossible.

Any pending returns from FY 2022-23 or earlier the ITC and reconciliation in them is permanently gone.

If you have any unfiled annual returns from FY 2022-23 onwards, file them immediately before tackling FY 2025-26.

What Is New in GSTR-9 for FY 2025-26

Several changes make the FY 2025-26 GSTR-9 meaningfully different from previous years:

Change 1 ➡️ GST 2.0 Rate Changes Must Be Correctly Reported

The 12% slab is effectively gone under GST 2.0. For businesses that had supplies straddling the September 22, 2025 rate change date, GSTR-9 must correctly bifurcate:

Supplies at old rates (April 2025 to September 21, 2025)

Supplies at new rates (September 22, 2025 to March 31, 2026)

Mixing these in a single rate column creates a rate-wise supply declaration error that GSTN's analytics will flag against your GSTR-1 data.

Change 2 ➡️ IMS Actions Reflected in Annual ITC

For the first time, GSTR-9 for FY 2025-26 will carry ITC data that flows from IMS-accepted invoices through GSTR-2B. The annual ITC declared in Table 6 must match the sum of monthly ITC accepted through IMS. Any ITC claimed that was not formally accepted in IMS will create a Table 6 vs GSTR-2B mismatch.

Change 3 ➡️ HSN-wise Summary Now Strictly Enforced

HSN-wise summary is mandatory. Common errors include: using 2-digit HSN for supplies above ₹5 crore (requires 6-digit), misclassifying services under goods HSN codes, and omitting inward HSN summary for capital goods and inputs above the threshold.

For FY 2025-26, GSTN has enhanced the automatic validation of HSN data against GSTR-1 filings. Errors at the HSN level now generate automatic advisories rather than just being flagged in the annual return summary.

Change 4 ➡️ Tables 10 and 11 Amendments Window

Any GSTR-1 amendment filed in April–November 2026 that relates to FY 2025-26 data must appear in Tables 10 and 11 of GSTR-9 for FY 2025-26. In practice, CAs often focus exclusively on April 2025 to March 2026 filings and miss these subsequent amendments entirely. The GSTN cross-checks Table 10 against GSTR-1A amendment data automatically.

If you amended any FY 2025-26 invoice in your April, May, June, or subsequent GSTR-1A filings, those amendments must be captured in Tables 10 and 11 of GSTR-9.

Change 5 ➡️ ITC Expiry Window Compressed

Unclaimed ITC can still be claimed in GSTR-3B filed before November 30, 2026 (for FY 2025-26 data), after which it lapses permanently.

This means: if your GSTR-2B for any month in FY 2025-26 showed ITC that you did not claim, you have until your GSTR-3B for October 2026 (filed by November 20/22/24) to claim it. After that, the ITC is gone regardless of what GSTR-9 shows.

The GSTR-9 Form Structure All 6 Parts

Understanding what goes where prevents the most common filing errors:

Part | Tables | What It Covers |

|---|---|---|

Part I | 1-3 | Basic details GSTIN, legal name, trade name, FY |

Part II | 4-5 | Outward supplies taxable, zero-rated, exempt, nil-rated, non-GST |

Part III | 6-8 | ITC availed, reversed, ineligible. Table 8 = ITC reconciliation with GSTR-2B |

Part IV | 9 | Tax paid details CGST, SGST, IGST, cess, interest, late fee |

Part V | 10-14 | Amendments and adjustments made after end of FY (April-November window) |

Part VI | 15-19 | Demand and refunds, HSN summary (outward + inward), late fees payable |

Table 8 deserves special attention. It reconciles ITC availed in GSTR-3B against ITC available in GSTR-2B. The difference ITC available in GSTR-2B but not claimed goes in Table 8D. This unclaimed ITC can still be claimed in GSTR-3B filed before November 30, 2026.

Step-by-Step Filing Process

Before You Start Gather These:

All 12 months' GSTR-1 data (April 2025 to March 2026)

All 12 months' GSTR-3B data

Annual GSTR-2B summary (download from portal)

Books of accounts turnover figure (for GSTR-9C if applicable)

Any DRC-03 payments made during the year

IMS acceptance/rejection records

Step 1 ➡️ Login to GST portal gst.gov.in → Login → Services → Returns → Annual Return → Select FY 2025-26 → GSTR-9 → Prepare Online.

Step 2 ➡️ Review auto-populated data The portal auto-populates most tables from your previously filed returns. Review each table carefully before accepting. Auto-populated figures are based on filed returns they will miss any corrections your books show.

Step 3 ➡️ Complete Tables 4 and 5 (Outward Supplies) Verify total taxable turnover matches your GSTR-1 aggregate. Separate correctly:

Taxable supplies (with correct rate-wise split including GST 2.0 pre/post September 22)

Zero-rated exports (with LUT or with payment of IGST two separate lines)

Exempt supplies

Nil-rated supplies

Non-GST supplies

Step 4 ➡️ Complete Table 6 (ITC Availed) This is the most scrutiny-prone section. The total ITC in Table 6 must match the sum of GSTR-3B Table 4A entries across all 12 months. Any discrepancy must be explained or corrected. Classify ITC correctly:

Inputs (goods purchased)

Input services

Capital goods

Imports IGST on Bill of Entry

ISD credits

RCM credits

Step 5 ➡️ Complete Table 7 (ITC Reversed) All ITC reversals made during the year — Rule 37 (180-day non-payment), Rule 42/43 (proportionate reversal), TRAN credit reversals, and any other reversals. Match against your GSTR-3B Table 4B entries.

Step 6 ➡️ Table 8 Reconciliation The system calculates Table 8 automatically from 8A (total ITC in GSTR-2B) and 8C (ITC claimed in GSTR-3B). If 8D shows a positive number (ITC available in GSTR-2B but not claimed), consider whether to claim it in October 2026 GSTR-3B before the November 30 window closes.

Step 7 ➡️ Table 9 (Tax Paid) The system auto-fills from GSTR-3B payment data. Verify the breakup of CGST, SGST, IGST, and cess matches your records. Include any DRC-03 voluntary payments made during the year.

Step 8 ➡️ Tables 10 and 11 (Amendments) Manually add any FY 2025-26 supply amendments made in GSTR-1A during April to November 2026. This is the most commonly missed section.

Step 9 ➡️ Table 17/18 (HSN Summary) Table 17: HSN-wise summary of outward supplies. Table 18: HSN-wise summary of inward supplies. Use 4-digit HSN for turnover below ₹5 crore, 6-digit above ₹5 crore. Do not use 2-digit HSN regardless of turnover — it will be flagged.

Step 10 ➡️ Compute and pay any shortfall If GSTR-9 reveals any additional tax liability not covered by monthly returns, pay the shortfall via DRC-03 before filing GSTR-9. GSTR-9 itself does not accept direct tax payment.

Step 11 ➡️ Upload GSTR-9C (if turnover above ₹5 crore) Your CA prepares GSTR-9C in offline utility, certifies it, and you upload the JSON file before submitting GSTR-9.

Step 12 ➡️ File GSTR-9 Preview, verify, and file. E-verify with DSC or EVC.

Late Fee and Penalty Structure

Delay | Late Fee |

|---|---|

Per day of delay | ₹200 (₹100 CGST + ₹100 SGST) |

Maximum cap | 0.25% of turnover in the state |

Interest on additional tax (if payable) | 18% per annum from due date |

GSTR 9 last date for FY 2025-26 is 31st December 2026.

For a business with ₹3 crore turnover, the late fee cap is ₹75,000 (0.25% of ₹3 crore). For a business with ₹10 crore turnover, it is ₹2.5 lakh. These are significant amounts — but the secondary impact (monthly return blocks) is even more expensive.

7 Common GSTR-9 Errors That Generate Notices

Error 1 ➡️ Including FY 2026-27 invoices in FY 2025-26 returns Including invoices from FY 2026-27 (April–November 2026) in FY 2025-26 GSTR-9 is a data contamination error. The invoice date determines which financial year a transaction belongs to, not the date of GSTR-1 filing.

Error 2 ➡️ Missing Tables 10 and 11 amendments Amendments to FY 2025-26 invoices filed in April–November 2026 go in Tables 10 and 11. Most businesses and CAs focus only on April 2025-March 2026 filings and miss the post-year-end amendment window entirely.

Error 3 ➡️ Wrong HSN digit level Using 2-digit HSN codes in Table 17 when your turnover requires 6-digit codes. This creates a classification validation mismatch.

Error 4 ➡️ Not reconciling DRC-03 payments Any voluntary tax payments made via DRC-03 during the year must be reflected in Table 9 under tax paid. Missing these creates a tax payment mismatch.

Error 5 ➡️ ITC claimed exceeds GSTR-2B Table 8 will show a negative figure if ITC claimed in GSTR-3B exceeds what was available in GSTR-2B. This is an automatic notice trigger.

Error 6 ➡️ Incorrect bifurcation of exempt vs nil-rated supplies Exempt supplies and nil-rated supplies are different classifications in GSTR-9 (Tables 4F and 4G). Clubbing them creates a declaration inconsistency.

Error 7 ➡️ Not paying shortfall before filing GSTR-9 reveals additional liability that was not covered by monthly returns. If you file GSTR-9 without paying this shortfall via DRC-03, the portal shows outstanding demand and you receive an automatic DRC-01 notice.

Tools for GSTR-9 Filing

GSTR-9 Estimator ➡️ Get an advance estimate of your annual return liability based on your monthly GSTR-3B data. Identify potential shortfalls before the December deadline.

GSTR-2B Reconciliation Tool ➡️ Table 8 of GSTR-9 requires GSTR-2B vs GSTR-3B ITC reconciliation. Use this tool to prepare the reconciliation before filing.

ITC Reversal Calculator ➡️ Calculate any ITC reversals required for Table 7, including 180-day Rule 37 reversals and proportionate reversals under Rules 42/43.

ITC Eligibility Checker ➡️ Verify each ITC head before declaring in Table 6. Blocked credits under Section 17(5) that were incorrectly claimed will show as mismatch in GSTR-9.

Due Date Calendar ➡️ Track the 31 December 2026 GSTR-9 deadline alongside all monthly return dates to ensure no blocking cascades.

GST Health Score ➡️ Get an overall compliance risk assessment before starting GSTR-9 preparation. Identifies gaps in monthly return consistency that will surface in annual return reconciliation.

Penalty Calculator ➡️ Calculate the late fee and interest for any filing delay or tax shortfall identified during GSTR-9 preparation.

GST Notice Reply Generator ➡️ If a DRC-01 or scrutiny notice has been issued based on GSTR-9 discrepancies, draft your response here.

Related Articles

GSTR-2B Mismatch: ITC Blocked How to Fix It ➡️ GSTR-9 Table 8 is the annual reconciliation of what you see in this article's daily issue. Clean up monthly mismatches now so annual GSTR-9 is straightforward.

GST Invoice Management System (IMS) Complete Guide 2026 ➡️ IMS acceptance data feeds directly into GSTR-9 Table 6 ITC declarations. Clean IMS management across all 12 months = clean GSTR-9.

GST Composition Scheme 2026 Complete Guide Composition dealers file GSTR-9A, not GSTR-9. Understand the difference and the correct annual return for your scheme.

GST 2.0 New Rate Structure 2025-26 ➡️Rate changes from September 22, 2025 must be correctly bifurcated in GSTR-9 Table 4. This article explains the new rate structure in full.

GSTAT Appeal Deadline 30 June 2026 ➡️ If GSTR-9 reconciliation reveals a past demand order, GSTAT is your appeal forum but only until June 30, 2026 for backlog cases.

References

Section 44, CGST Act, 2017 ➡️ Annual return filing requirement

CGST Notification 14/2024 dated 10 July 2024 ➡️ Optional GSTR-9 for turnover below ₹2 crore for FY 2023-24

GSTN Advisory ➡️ 3-year filing cap implementation, July 2025

CBIC Circular No. 183/15/2022-GST ➡️ GSTR-9 reconciliation and ITC claims

Rule 138E, CGST Rules ➡️ EWB blocking for GSTR-3B defaulters

Section 47(2), CGST Act ➡️ Late fee for annual return

Rule 37, CGST Rules ➡️ ITC reversal on non-payment (180-day rule)

Rules 42 and 43, CGST Rules ➡️ Proportionate ITC reversal

GSTR-9 Form Instructions ➡️ AY 2025-26, CBIC

ClearTax Advisors GSTR-9 Guide FY 2025-26, May 2026

31 December 2026 Is Six Months Away. File by October.

The GSTR-9 deadline is December 31. But the GST portal becomes painfully slow in December not because GSTN cannot handle traffic, but because most of India files in the last two weeks. OTP failures, portal timeouts, and last-minute CA availability crunches are annual certainties.

The November 30 ITC expiry date is actually your real operational deadline. Any unclaimed ITC from GSTR-2B for FY 2025-26 must be claimed in your October GSTR-3B. File GSTR-9 before that by October to know exactly what ITC you need to claim before the window closes.

Every GST deadline, portal update, and compliance change explained the day it happens:

Content verified against Section 44 of CGST Act 2017, CGST Notification 14/2024, and GSTN Advisory on 3-year filing cap. Last updated: 12 June 2026. Consult a CA for GSTR-9C preparation and complex reconciliation situations.