Two Businesses. Same ₹80 Lakh Turnover. One Pays ₹3.6 Lakh in Tax. The Other Pays ₹18,000.

Both are GST-registered traders in Pune. Both had ₹80 lakh in sales last financial year. Both are fully compliant GST returns filed on time, income tax paid.

The first trader maintains full books of accounts, hired a CA to prepare a detailed P&L statement, and declared ₹20 lakh as actual net profit. Income tax on ₹20 lakh (after standard deductions): approximately ₹3.6 lakh.

The second trader filed ITR-4 under Section 44AD, declared 6% of ₹80 lakh as income (₹4.8 lakh), claimed the basic exemption limit, and paid approximately ₹18,000 in income tax.

Same turnover. Same business type. Tax savings of ₹3.42 lakh per year legally.

The second trader is not doing anything wrong. Section 44AD of the Income Tax Act, 1961 exists precisely for this purpose to give small businesses a simplified, low-paperwork option that reduces both the compliance burden and the effective tax rate. The government built in a presumptive income rate that is typically lower than actual profit margins, making it attractive for small GST dealers.

But Section 44AD has a trap that nobody mentions clearly: a five-year lock-in that, if violated, bars you from the scheme for five more years. And a GST-vs-ITR turnover reconciliation requirement that, if missed, generates an income tax notice that lands six months after you think filing season is over.

This guide covers everything: who qualifies, how the 6% vs 8% rule works, the lock-in trap, how to reconcile your GST turnover with your ITR, and the exact steps to file ITR-4 before the 31 August 2026 deadline.

What Is Section 44AD The Presumptive Taxation Scheme

Section 44AD of the Income Tax Act, 1961 is a presumptive taxation scheme that allows eligible small businesses to declare income at a fixed percentage of turnover without maintaining detailed books of accounts, without preparing a profit and loss statement, and without requiring a tax audit.

The word "presumptive" means the government presumes your income is a certain percentage of your turnover. You declare that percentage as your income, pay tax on it, and the tax department accepts it without asking for supporting documentation of actual expenses.

For a GST-registered trader or manufacturer with genuine profit margins that exceed the presumptive rate, this is an enormous benefit. For a business with thin margins where actual profit is lower than the presumptive rate it can result in paying more tax than necessary.

Who Can Use Section 44AD Eligibility for FY 2025-26

Eligible

Individual residents → salaried person with a side business, sole proprietor, independent contractor dealing in goods

Hindu Undivided Families (HUFs) → family-run trading or manufacturing businesses

Partnership firms (excluding Limited Liability Partnerships) traditional partnership shops and businesses

Eligible Business Types

Any business other than the following specifically excluded categories:

Transport businesses under Section 44AE (they have their own scheme)

Agency businesses (commission agents, brokers)

Businesses earning brokerage or commission income

Professionals doctors, lawyers, CAs, architects, engineers (they use Section 44ADA instead)

Turnover Limits for FY 2025-26 (AY 2026-27)

Receipt Type | Turnover Limit |

|---|---|

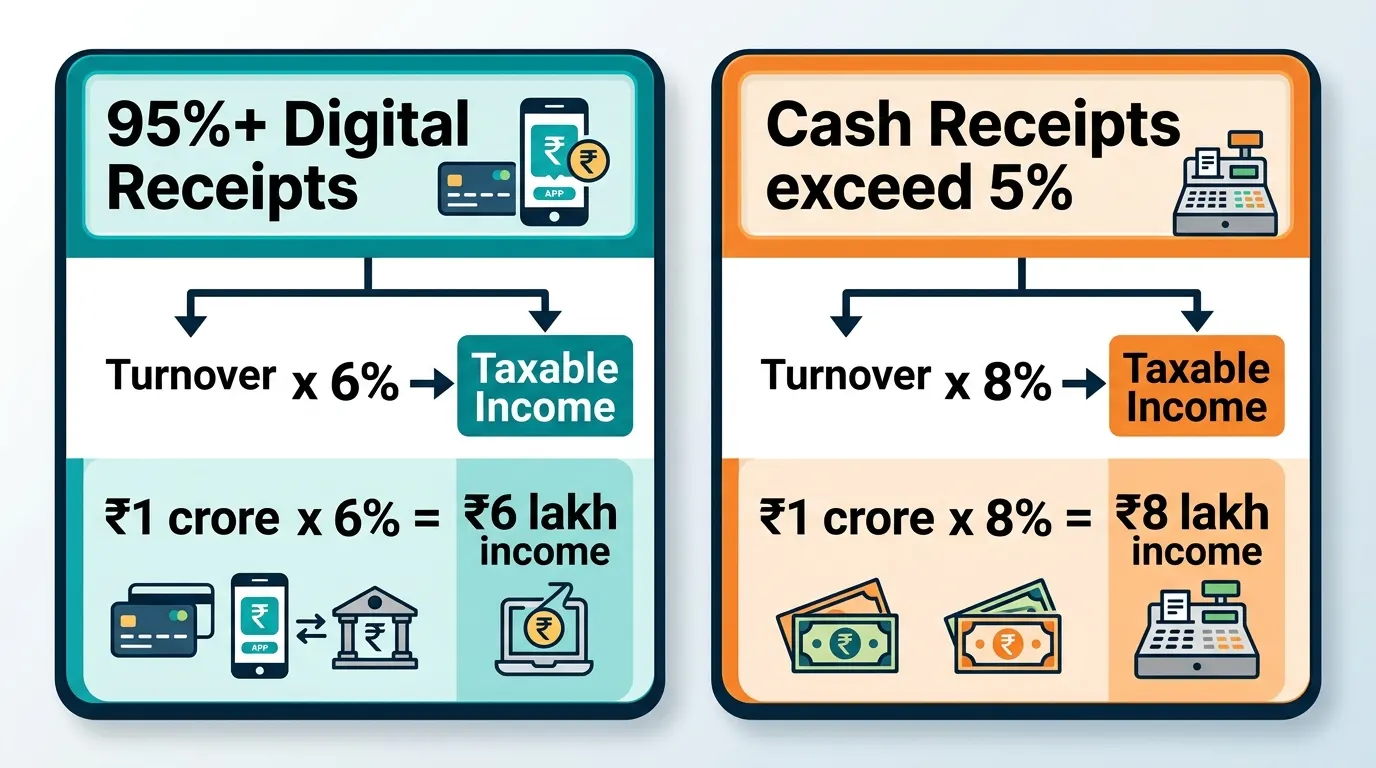

95% or more digital receipts (UPI, NEFT, RTGS, cheque, card) | ₹3 crore |

Cash receipts exceed 5% of total receipts | ₹2 crore |

This means a GST-registered trader who receives most payments digitally can use Section 44AD up to ₹3 crore turnover covering the vast majority of small and medium-sized GST dealers.

Who Is NOT Eligible

LLPs (Limited Liability Partnerships) must use regular taxation

Businesses that opted out of Section 44AD in any of the previous 5 years and declared income lower than the presumptive rate

Businesses with turnover exceeding the applicable limit

Persons claiming deductions under Sections 10A, 10AA, 10B, 10BA, 80HH to 80RRB

Anyone who filed ITR-3 (with detailed accounts) in the previous year on the basis of maintaining books they must continue on ITR-3

The 6% vs 8% Rule Which Applies to Your Business?

The presumptive income rate under Section 44AD has two tiers:

6% of turnover → if 95% or more of your total receipts during the year were received through banking channels (NEFT, RTGS, cheque, UPI, debit/credit card, online payment).

8% of turnover → if more than 5% of your receipts were in cash.

This split was introduced to incentivise digital transactions. The government effectively offers a 2 percentage point tax rate reduction as a reward for going cashless.

How to calculate:

Turnover | Receipt Type | Presumptive Income | Tax (New Regime, individual) |

|---|---|---|---|

₹50 lakh | 95%+ digital | 6% = ₹3 lakh | Nil (below ₹3L threshold) |

₹50 lakh | Cash > 5% | 8% = ₹4 lakh | ₹10,000 approx |

₹1 crore | 95%+ digital | 6% = ₹6 lakh | ₹30,000 approx |

₹1 crore | Cash > 5% | 8% = ₹8 lakh | ₹50,000 approx |

₹2 crore | 95%+ digital | 6% = ₹12 lakh | ₹2,28,600 approx |

₹3 crore | 95%+ digital | 6% = ₹18 lakh | ₹4,68,600 approx |

Tax calculated under new tax regime for individual. Deductions under 80C, 80D etc. not available under new regime.

Practical check: Look at your bank statements and payment records for the year. Add up all cash receipts (money received as physical notes). Divide by total turnover. If cash is more than 5%, you are on 8%.

Use the SmartGST GST Calculator to quickly cross-check turnover figures from your GST returns before plugging them into your ITR-4.

The Five-Year Lock-In The Trap Most Small Businesses Walk Into

This is the rule that causes the most confusion and the most long-term damage from Section 44AD.

Under Section 44AD(4):

If you opt for the presumptive scheme, you must continue declaring income under the scheme for five consecutive assessment years.

If you declare income lower than the presumptive rate (lower than 6% or 8% of turnover) in any year within those five years, or if you opt out entirely:

You lose eligibility for Section 44AD for the next five assessment years.

You must maintain detailed books of accounts under Section 44AA.

If your income exceeds the basic exemption limit, your accounts must be audited under Section 44AB.

Real example of the trap:

A textile trader opted for 44AD in AY 2022-23. In AY 2024-25, he had a bad year actual profits were below 6% of turnover. He decided to declare actual income (lower than 6%) and file ITR-3 instead. Result: he cannot use Section 44AD until AY 2030-31. For six years, he must maintain full books and face audit risk if turnover exceeds the threshold.

The right approach: If you are having a bad year and actual profit is below 6%, you have two choices either still declare 6% (pay slightly more tax than actual profit warrants, but keep your 44AD eligibility), or consciously opt out knowing the five-year consequence. Do not stumble into the opt-out by accident.

Exception: The lock-in does not apply if you become ineligible for reasons outside your control for example, your turnover crosses the ₹3 crore limit. In that case, you exit the scheme due to ineligibility, not by choice, and the five-year bar does not apply.

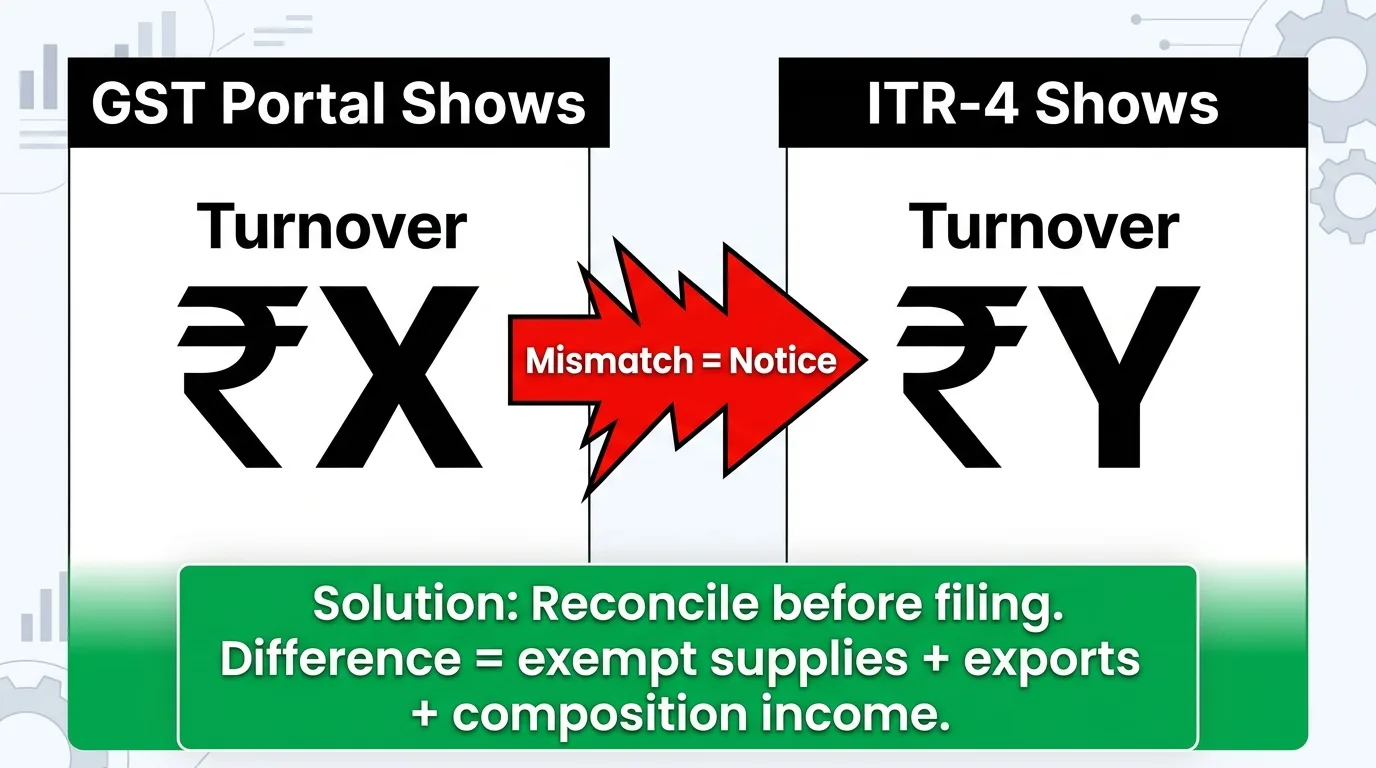

GST Turnover vs Income Tax Turnover The Reconciliation That Prevents Notices

This is the most important section in this guide for GST-registered businesses. The Income Tax department cross-checks your ITR-4 turnover against your GST return data automatically. The AIS (Annual Information Statement) now pulls your GST-reported supply data directly from the GST portal.

If your ITR-4 turnover differs from your GST turnover without explanation, you receive an automatic notice.

Why the Figures Legitimately Differ

GST turnover and income tax turnover are calculated differently. They will almost never match exactly, and that is expected but the difference must be explainable.

Item | Included in GST Turnover? | Included in IT Turnover? |

|---|---|---|

Taxable outward supplies | Yes | Yes |

Exempt supplies (0% GST items) | Yes (as aggregate turnover) | Yes |

Export supplies (zero-rated) | Yes | Yes |

Composition scheme income | Reported in GSTR-4 | Yes, in IT return |

GST amount collected | Separate from value | Not included (GST is a pass-through) |

Advance receipts not yet supplied | May appear in GST | Depends on recognition basis |

Returns and credit notes | Reduce GST turnover | Reduce IT turnover |

The most common legitimate difference: GST turnover includes the GST amount collected on sales. Income tax turnover is on the base value (exclusive of GST). On ₹1 crore GST-inclusive sales at 18%, your GST turnover = ₹1 crore, IT turnover = ₹84.75 lakh (base value).

How to Prepare the Reconciliation

Before filing ITR-4, prepare a one-page reconciliation statement:

GST Annual Turnover (from GSTR-9 or aggregate of GSTR-3B) ₹X

Less: GST component collected (output GST) (₹Y)

Less: Exempt supplies included in GST but not in IT (₹Z)

Add: Any income not reported in GST (interest, etc.) ₹A

= Income Tax Turnover (as reported in ITR-4) ₹B

Keep this reconciliation saved. If a notice comes, this document is your defence. If the figures reconcile clearly, no further explanation is needed.

Step-by-Step: Filing ITR-4 Under Section 44AD

Before you start:

Gather your GST returns summary (GSTR-3B totals or GSTR-9 for FY 2025-26)

Confirm your receipt pattern (digital vs cash) for the 6% vs 8% determination

Prepare the GST-IT turnover reconciliation

Have your PAN, Aadhaar, and bank account details ready

Step 1 → Login to Income Tax e-Filing Portal Go to incometax.gov.in → Login with PAN and password → e-File → Income Tax Returns → File Income Tax Return.

Step 2 → Select assessment year and form Assessment Year: 2026-27 (for income earned in FY 2025-26, April 2025 to March 2026). Return type: ITR-4 (Sugam). Filing mode: Online (recommended for straightforward cases).

Step 3 → Confirm pre-filled data The portal pre-fills your name, PAN, bank accounts, TDS details, and some income data from AIS. Review carefully pre-filled figures can have errors. Correct anything wrong before proceeding.

Step 4 → Fill Business Income under Presumptive Scheme In the Business Income section → Presumptive Business Income (Section 44AD):

Enter your total turnover for FY 2025-26 (from your GST records)

Select 6% or 8% based on your receipt pattern

The system calculates your presumptive income automatically

Enter the income figure (confirm it matches the calculation)

Step 5 → Enter other income if applicable If you have salary income, rental income, interest income, or capital gains enter each in the relevant section. ITR-4 allows combination of presumptive business income with up to one house property income and other sources.

Step 6 → Claim deductions (old tax regime only) If you are under the old tax regime: enter deductions under 80C (PPF, LIC, ELSS), 80D (health insurance), 80TTA (savings interest), etc. Under the new regime (default from AY 2024-25): no deductions available.

Step 7 → Enter tax paid Enter advance tax payments (if any), TDS deducted on payments received, and TCS collected (for e-commerce sellers).

Step 8 → Compute tax and verify The system computes your total tax liability, subtracts taxes already paid, and shows the net amount payable or refundable.

Step 9 → Verify and submit E-verify using Aadhaar OTP (instant) or net banking. Physical ITR-V is the alternative but requires courier to CPC Bengaluru within 30 days.

The 31 August 2026 Deadline And What Missing It Costs

The ITR-4 filing deadline for FY 2025-26 (AY 2026-27) for non-audit cases is 31 August 2026.

Section 44AD users do not require a tax audit, so the audit deadline (31 October) does not apply. Your deadline is 31 August.

If you miss 31 August:

Action | Consequence |

|---|---|

File between 1 Sept – 31 Dec 2026 | Belated return. Late fee ₹5,000 (₹1,000 if income below ₹5 lakh). |

File between 1 Jan – 31 Mar 2027 | Late fee ₹5,000 + loss of certain carry-forward deductions |

After 31 March 2027 | Return cannot be filed at all. Assessment by IT department. |

The ₹5,000 late fee is a fixed penalty it applies even if your net tax due is zero. If you are due a refund, filing late delays the refund by several months.

Advance Tax The Obligation Most 44AD Filers Miss

Section 44AD has a specific advance tax rule that differs from regular taxpayers.

Regular taxpayers pay advance tax in four installments: June 15, September 15, December 15, March 15.

Section 44AD taxpayers must pay 100% of their estimated tax in a single installment by March 15.

If you miss March 15 and pay the full tax only at filing time (in July-August), interest under Section 234C applies 1% per month on the unpaid advance tax from April 1 to the filing date.

On ₹6 lakh presumptive income with ₹30,000 tax liability: missing the March 15 advance tax and paying in August means 5 months × 1% = 5% interest = ₹1,500 in avoidable interest.

Section 44ADA For Professionals Using ITR-4

If you are a professional doctor, lawyer, CA, engineer, architect, interior designer, technical consultant rather than a trader or manufacturer, Section 44ADA is your version of the presumptive scheme.

Key differences from 44AD:

Feature | Section 44AD (Businesses) | Section 44ADA (Professionals) |

|---|---|---|

Eligible types | Traders, manufacturers | Specified professionals |

Turnover limit | ₹3 crore (digital), ₹2 crore (cash) | ₹75 lakh |

Presumptive rate | 6% or 8% | 50% of gross receipts |

ITR form | ITR-4 | ITR-4 |

Five-year lock-in | Yes | No |

The 50% rate under 44ADA sounds high but it is intentional — professionals typically have higher profit margins than traders, and 50% is set to reflect that.

Tools to Prepare Your ITR-4 Filing

GST Calculator → Quickly compute your net turnover exclusive of GST (base value) from your GST-inclusive sales figures. The IT turnover figure goes into ITR-4; this tool separates base value from GST component.

GST Health Score → Before filing ITR-4, check your GST compliance profile. Ensure all GSTR-3B returns are filed and there are no outstanding demands that could affect your turnover declaration.

Due Date Calendar → Track both GST filing deadlines and income tax advance tax dates (March 15 for 44AD filers) in one place.

Penalty Calculator → Calculate the late fee and interest if you missed the March 15 advance tax deadline or are considering a late ITR-4 filing.

GSTR-9 Estimator → Get an advance summary of your annual GST turnover — the same figure you will use as the basis for your ITR-4 presumptive income calculation.

GST Registration Limit Calculator → For new businesses deciding whether to register for GST and simultaneously opt for 44AD, this tool checks both thresholds.

Related Articles on SmartGST

GST Composition Scheme 2026 Complete Guide → Many composition scheme taxpayers also use Section 44AD for income tax. The interaction between the two schemes has important turnover reconciliation implications.

GSTR-2B Mismatch: ITC Blocked How to Fix It → If your GST compliance has gaps, the IT department will see them when they cross-check your ITR-4 against GST data.

How to Check and Respond to a GST Notice → IT-GST turnover mismatches can generate income tax notices, not just GST notices. The response process is similar.

GST for Freelancers India 2026 → Freelancers who are GST registered and under ₹50 lakh receipts use Section 44ADA (50% presumptive) the professional version of this scheme.

GST 2.0 New Rate Structure 2025-26 → Rate changes under GST 2.0 affect the GST component in your sales. This changes the base value calculation for your ITR-4 turnover figure.

References

Section 44AD, Income Tax Act, 1961 → Presumptive taxation for small businesses

Section 44ADA, Income Tax Act, 1961 → Presumptive taxation for professionals

Section 44AB, Income Tax Act, 1961 → Tax audit requirements

Section 234C, Income Tax Act, 1961 → Interest for non-payment of advance tax

CBDT Notification → ITR-4 Form for AY 2026-27 and Instructions

Section 139(1), Income Tax Act→ Return filing due dates

Finance Act 2023 Enhancement of Section 44AD limit to ₹3 crore for digital receipts

Section 115BAC, Income Tax Act → New tax regime (default from AY 2024-25)

ITR-4 eligibility: individuals, HUFs and firms with total income up to ₹50 lakhs under presumptive taxation schemes Sections 44AD, 44ADA, or 44AE

GSTN-AIS Integration → Income Tax Department cross-verification framework, 2025

31 August 2026. That Is Your Deadline. File Before July.

The ITR-4 deadline is 31 August 2026. But "before the deadline" is not a strategy. The Income Tax portal becomes genuinely slow in the last week of August every year → crashing at peak hours, failing OTP verifications, delaying e-verification.

File by July 31. Use the time you save to verify your GST-IT reconciliation is clean and you are not walking into an advance tax notice.

Every tax deadline, GST circular, and compliance change explained the day it happens:

Content verified against Section 44AD of the Income Tax Act, 1961, CBDT AY 2026-27 ITR-4 instructions, and GSTN-AIS data-sharing framework. Last updated: 9 June 2026. Consult a CA for complex multi-source income, capital gains, or carry-forward loss situations.