Your Office Rent Agreement Does Not Mention GST. That Does Not Mean You Don't Owe It.

A Delhi-based marketing agency rented a commercial office from an unregistered landlord for ₹80,000 per month. The rent agreement had no mention of GST. The landlord had no GSTIN. The agency paid rent every month, claimed no ITC, filed their GSTR-3B, and assumed everything was fine.

In October 2024, a new CBIC notification made it mandatory for GST-registered tenants to pay 18% GST directly to the government on rent paid to unregistered landlords under the Reverse Charge Mechanism.

The agency had been underpaying tax for months. No one told them. The landlord did not know either. When the scrutiny notice arrived, the underpaid GST was ₹1.44 lakh. The interest at 24% per annum added another ₹28,000. Total outgo from one overlooked notification: ₹1.72 lakh.

GST on rent is one of the most genuinely confusing areas in Indian tax law because the rules are different depending on property type, who the tenant is, whether the landlord is registered, and how the property is actually used. This guide walks through every scenario with exact rates, SAC codes, ITC rules, and the specific notifications that govern each situation.

The Core Framework Why Rent Gets Complicated Under GST

Under GST, renting property is treated as a supply of service. That makes it potentially taxable — but not always. The GST treatment depends on four variables that interact with each other:

Property type → residential or commercial

Who is the tenant → individual for personal use, or a registered business

Whether the landlord is registered → determines forward charge vs RCM

Annual rental income → determines whether registration is even required

Get any of these wrong as a landlord, as a business tenant, or as an accountant handling the accounts and you face underpaid tax, interest at 24% per annum, and a GST notice.

The SAC code for all rental income is 997212 (rental or leasing services involving own or leased non-residential property) for commercial property and 997211 for residential property rental.

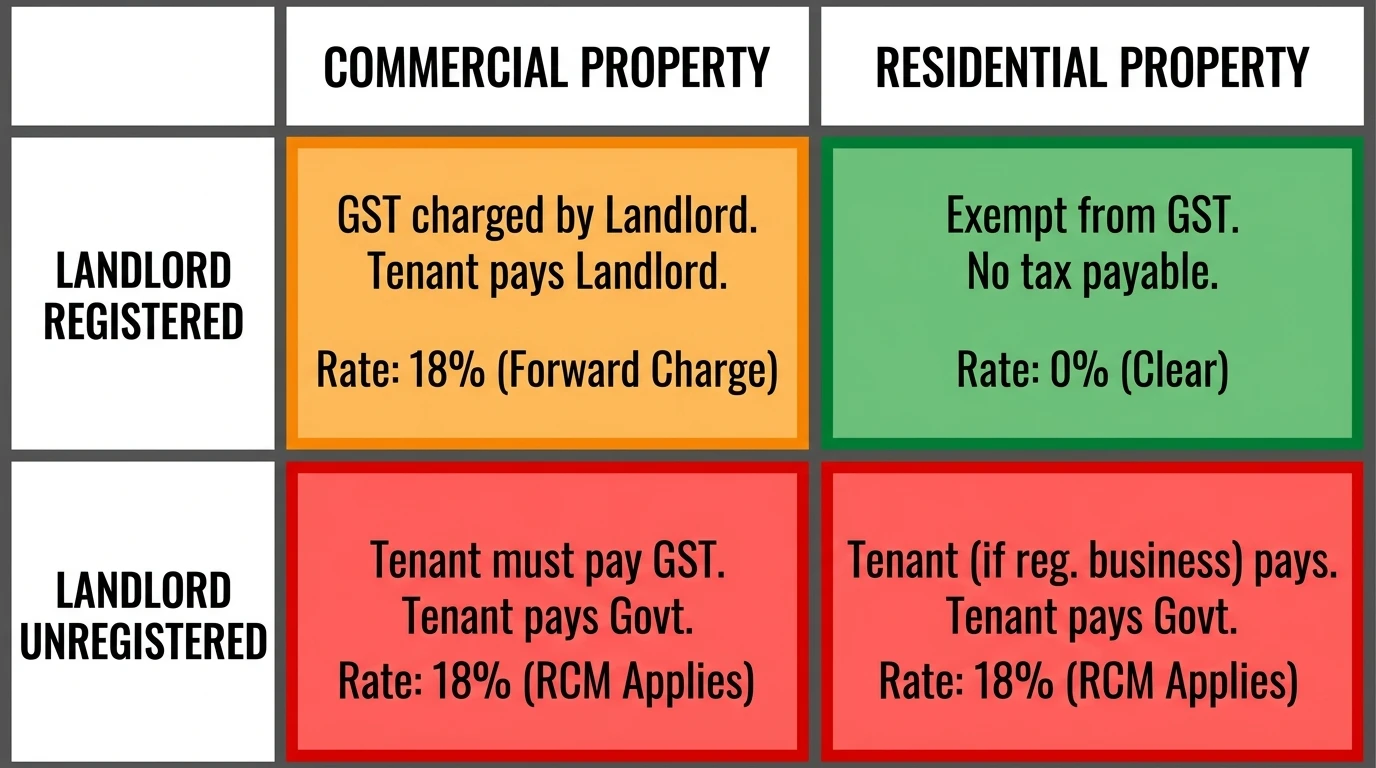

Scenario 1 Residential Property Rented to an Individual (Most Common)

Rule: Fully exempt from GST. No tax. No registration required for the landlord solely due to this income.

This is the scenario that covers the vast majority of rental transactions in India a family renting a flat, an individual paying PG accommodation, a student renting a room. As long as the property is a residential dwelling and the tenant is using it for personal residential purposes, GST does not apply at any income level.

This exemption has no upper limit. A landlord earning ₹2 crore annually from residential rentals to individual tenants owes zero GST on that income (though their aggregate turnover calculation may require registration if they have other business income).

ITC: Not applicable no GST was charged.

Key rule: The use determines the exemption, not the property type. A residential flat used as an office loses the exemption.

Scenario 2 Residential Property Rented to a Registered Business (The Trap Most Businesses Fall Into)

Rule: 18% GST under Reverse Charge Mechanism (RCM), payable by the tenant directly to the government.

This is the rule introduced by Notification No. 05/2022-IT(R) dated 18 July 2022 and it has caught hundreds of businesses off guard since then.

If a GST-registered company, LLP, partnership firm, or proprietorship rents a residential flat even for use as an employee residence, guest house, director's accommodation, or company office the tenant must pay 18% GST under RCM.

Critically: the landlord does not need to be GST-registered for this obligation to apply. The obligation sits entirely with the tenant.

Exception carved out: If a registered sole proprietor rents a residential property in their personal capacity for personal residential use not for the business RCM does not apply. This exception was clarified to prevent the rule from taxing a self-employed person's own home rent.

Real calculation:

A tech startup rents a 3BHK flat in Bengaluru for ₹50,000/month as employee housing:

Monthly rent: ₹50,000

GST under RCM (18%): ₹9,000

Payable to government by the company each month: ₹9,000

Annual RCM liability: ₹1,08,000

Can the company claim ITC on this? No. ITC on accommodation and employee housing is blocked under Section 17(5)(b) of the CGST Act. The ₹9,000 per month RCM payment is a pure cost it cannot be offset against output tax.

This is what makes this scenario particularly painful: you pay RCM you cannot recover.

Scenario 3 Commercial Property Rented to a Registered Tenant (Landlord Also Registered)

Rule: 18% GST under Forward Charge Mechanism. Landlord charges GST, collects it from the tenant, and remits to government via GSTR-3B.

This is the standard commercial rent scenario. A GST-registered landlord leases out an office, shop, warehouse, showroom, or industrial space to a GST-registered business.

The applicable rate is 18% under SAC code 997212. The landlord must register for GST and charge 18% GST on rent invoices only if their total annual rental income exceeds ₹20 lakh.

Example:

A landlord rents a shop at ₹60,000/month:

Taxable rent: ₹60,000

GST at 18%: ₹10,800

Total invoice to tenant: ₹70,800

Landlord deposits ₹10,800 in GSTR-3B

Can the tenant claim ITC? Yes fully, provided the space is used for business purposes. The ₹10,800 GST paid by the tenant becomes ITC, offsetting their own output tax liability.

SAC code on invoice: 997212 Type of GST: CGST 9% + SGST 9% (intrastate) or IGST 18% (interstate)

Scenario 4 Commercial Property Rented to a Registered Tenant (Landlord Unregistered)

Rule: 18% GST under Reverse Charge Mechanism, payable by the registered tenant.

This rule was extended significantly by Notification No. 09/2024-IT(R) dated 8 October 2024. Before this notification, RCM on commercial rent applied only in specific situations. From October 2024, any GST-registered tenant renting commercial property from an unregistered landlord must pay 18% GST under RCM.

This is the scenario that caught the Delhi marketing agency from the opening of this article.

The key distinction from Scenario 3: The landlord does not issue a tax invoice. The tenant self-invoices (raises a self-invoice under Rule 47A of CGST Rules) and pays the RCM liability directly in GSTR-3B.

Can the tenant claim ITC? Yes unlike the residential RCM scenario, commercial RCM is ITC-eligible. The tenant pays ₹14,400 RCM on ₹80,000 commercial rent, but can claim that ₹14,400 back as ITC. The net cash outflow is zero if the tenant has sufficient output tax liability.

Why businesses miss this:

Landlord does not know about the rule (unregistered, so not in the GST ecosystem)

Rent agreement has no GST clause

Accountant treats rent as a non-GST expense

No alert from the GST portal (the system cannot know you are paying rent to an unregistered party)

Scenario 5 Residential Property Used as Office/Commercial Premises

Rule: 18% GST applies treated as commercial use regardless of the physical property type.

Even if the building is residential in nature but rented out for business purposes, GST applies. The moment a residential property is used for commercial activities, the residential exemption is lost.

This covers:

A flat converted into a call centre

A house used as a small factory or trading unit

A residential apartment used as a registered office address with actual business operations

In such cases, if the landlord is registered forward charge at 18%. If the landlord is unregistered and the tenant is registered RCM at 18% on the tenant.

The Complete Decision Matrix

Property Type | Tenant Type | Landlord Status | Who Pays GST | Rate | ITC Available? |

|---|---|---|---|---|---|

Residential | Individual (personal use) | Any | No GST | 0% | N/A |

Residential | Registered business | Any | Tenant (RCM) | 18% | No blocked |

Commercial | Registered business | Registered | Landlord (Forward) | 18% | Yes |

Commercial | Registered business | Unregistered | Tenant (RCM) | 18% | Yes |

Commercial | Individual/unregistered | Registered | Landlord (Forward) | 18% | N/A |

Residential (used commercially) | Registered business | Unregistered | Tenant (RCM) | 18% | Yes |

GST Registration Threshold for Landlords

A landlord must register for GST and charge GST on commercial rent only if their aggregate annual turnover exceeds ₹20 lakh (₹10 lakh in special category states).

Aggregate turnover includes all rental income plus any other business income under the same PAN. A landlord earning ₹18 lakh from commercial rentals and ₹5 lakh from freelance consulting has an aggregate of ₹23 lakh crossing the threshold.

Below this threshold, a landlord cannot voluntarily charge GST on commercial rent to avoid having to register. But the tenant's RCM obligations (Scenarios 2 and 4) exist regardless of the landlord's registration or turnover.

How to Account for RCM on Rent Step by Step

If you are a registered business paying rent to an unregistered landlord (commercial) or any landlord (residential as employee housing), here is the monthly process:

Step 1 → Raise a self-invoice Under Rule 47A of CGST Rules, you must raise a self-invoice on your own GST number for the RCM transaction. The self-invoice should show:

Your GSTIN as both supplier and recipient

SAC code 997211 (residential) or 997212 (commercial)

Rental value

18% GST as RCM liability

Note: "Tax payable on Reverse Charge Basis"

Step 2 → Pay RCM liability in GSTR-3B In GSTR-3B → Table 3.1(d) "Inward supplies liable to reverse charge" declare the rental value and RCM tax. Pay through the Electronic Cash Ledger.

Step 3 → Claim ITC (only for commercial RCM) For commercial rent RCM: In GSTR-3B → Table 4A(3) "Inward supplies liable to reverse charge (other than above)" claim the ITC. This offset happens in the same return, so the net cash impact is often zero.

For residential rent RCM: Do NOT claim ITC it is blocked under Section 17(5).

Step 4 → Maintain records Keep the rent agreement, payment receipts, and self-invoices for each month. These are required documentation if any notice is raised.

Use the SmartGST RCM Calculator to calculate your exact monthly RCM liability on rent based on the property type and rental amount.

ITC Rules on Rent What You Can and Cannot Claim

Scenario | ITC Eligible? | Section/Reason |

|---|---|---|

Commercial office rent, forward charge | Yes, fully | Business use |

Commercial rent under RCM (unregistered landlord) | Yes, fully | Business use, ITC allowed on RCM |

Residential property as employee housing (RCM) | No | Section 17(5)(b) blocked credit |

Residential flat as company's registered office (actual use is commercial) | Yes but scrutiny risk | Depends on actual use evidence |

Co-working space membership (GST charged) | Yes | Business use, not blocked |

The RWA (Resident Welfare Association) angle: If you live in a society managed by a Resident Welfare Association, maintenance up to ₹7,500 per month per flat is exempt. If maintenance exceeds ₹7,500, GST at 18% applies on the full amount.

Worked Example Multi-Property Business Owner

Consider a business owner in Mumbai who has:

One commercial office (own property) rented out to a company for ₹1.5 lakh/month landlord is GST-registered

One residential flat rented to a company for employee housing at ₹50,000/month landlord not registered

One shop rented from an unregistered landlord for ₹40,000/month for own business

Property 1 (owns, rents commercially): Charges 18% GST (₹27,000/month) to tenant on invoice. Deposits in GSTR-3B. Annual GST collected and remitted: ₹3,24,000.

Property 2 (owns residential, rents to company): Tenant pays RCM of ₹9,000/month. Landlord does not collect or remit. Tenant cannot claim ITC. This is the tenant's problem, not the landlord's.

Property 3 (rents shop from unregistered landlord): The business owner pays ₹40,000 rent. Must pay RCM of ₹7,200/month. But can claim ₹7,200 as ITC. Net cash impact: zero.

Three properties, three different GST treatments, three different parties responsible.

Key GST Notifications on Rent Reference List

Notification | Date | What It Did |

|---|---|---|

Notification No. 12/2017-CT(R) | 28 June 2017 | Original exemption for residential dwelling rental for residential use |

Notification No. 05/2022-IT(R) | 18 July 2022 | RCM on residential property rented to registered businesses |

Notification No. 09/2024-IT(R) | 8 October 2024 | RCM extended to commercial property rented from unregistered landlords |

Tools to Handle GST on Rent

RCM Calculator → Enter your monthly rent, property type, and landlord registration status. Get your exact RCM liability, monthly and annual, with ITC eligibility breakdown.

GST Calculator → Calculate the 18% GST on any rent amount forward charge or RCM instantly.

GSTIN Validator → Verify your landlord's GSTIN status before deciding whether forward charge or RCM applies.

GST Registration Status → Check if your landlord is Active, Suspended, or Cancelled this determines your GST treatment.

GST Notice Reply Generator → If you have received a scrutiny notice for missed RCM on rent, draft a structured response here.

Penalty Calculator → Calculate interest and penalties on underpaid RCM since the applicable notification date.

ITC Eligibility Checker → Verify whether the RCM you paid on commercial rent is ITC-eligible or blocked before filing GSTR-3B.

Related Articles on SmartGST

Reverse Charge Mechanism Under GST Complete Guide → RCM on rent is declared in GSTR-3B Table 3.1(d). This guide covers the complete GSTR-3B filing process with RCM sections explained.

GST for Freelancers India 2026 → If you are a freelancer working from home or a co-working space, understand how rent GST affects your ITC claims.

How to Verify a Fake GST Invoice → Before paying any rent invoice with GST, verify the landlord's GSTIN is active and correctly registered.

GSTR-2B Mismatch: ITC Blocked How to Fix It → If your commercial rent ITC is not showing in GSTR-2B because the landlord hasn't filed, this guide explains your options.

GST 2.0 New Rate Structure 2025-26 → GST on rent was not changed under GST 2.0, but verify if any service bundled with your rental (maintenance, security) changed rates.

References

Section 7(1), CGST Act, 2017 → Definition of supply (includes renting of immovable property)

Section 9(3), CGST Act, 2017 → Reverse Charge Mechanism on specified supplies

Notification No. 12/2017-CT(R) dated 28 June 2017 → Exemption for residential dwelling rental

Notification No. 05/2022-Integrated Tax (Rate) dated 18 July 2022 → RCM on residential rent to registered businesses

Notification No. 09/2024-Integrated Tax (Rate) dated 8 October 2024 → RCM on commercial rent from unregistered landlords

Rule 47A, CGST Rules, 2017 → Self-invoice requirement for RCM transactions

Section 17(5)(b), CGST Act, 2017 → Blocked credits including employee accommodation

CBIC FAQ on GST on Real Estate and Rental Services, 2024

SAC 997211, 997212 → Classification of rental services under GST

AAR Karnataka → Ruling on residential property used as commercial office, 2023

Don't Let a Landlord's Ignorance Become Your Tax Notice

The October 2024 RCM extension on commercial rent from unregistered landlords affected hundreds of thousands of businesses most of whom had no idea until notices started arriving in early 2026. The rule did not come with an alert from the GST portal or a message from your landlord. It came as a notification in the official gazette, which most business owners never read.

That is the nature of GST compliance in India. Rules change. Notifications come. Businesses pay the price of not knowing.

The SmartGST WhatsApp Channel publishes every CBIC notification that affects your business → explained in plain English within 24 hours of release.

Content verified against Notification No. 05/2022-IT(R), Notification No. 09/2024-IT(R), and Section 9(3) of CGST Act, 2017. Last updated: 9 June 2026. Consult a CA for your specific rental structure and ITC eligibility.