HRA Exemption Calculation: Complete Guide With Examples (2025-26)

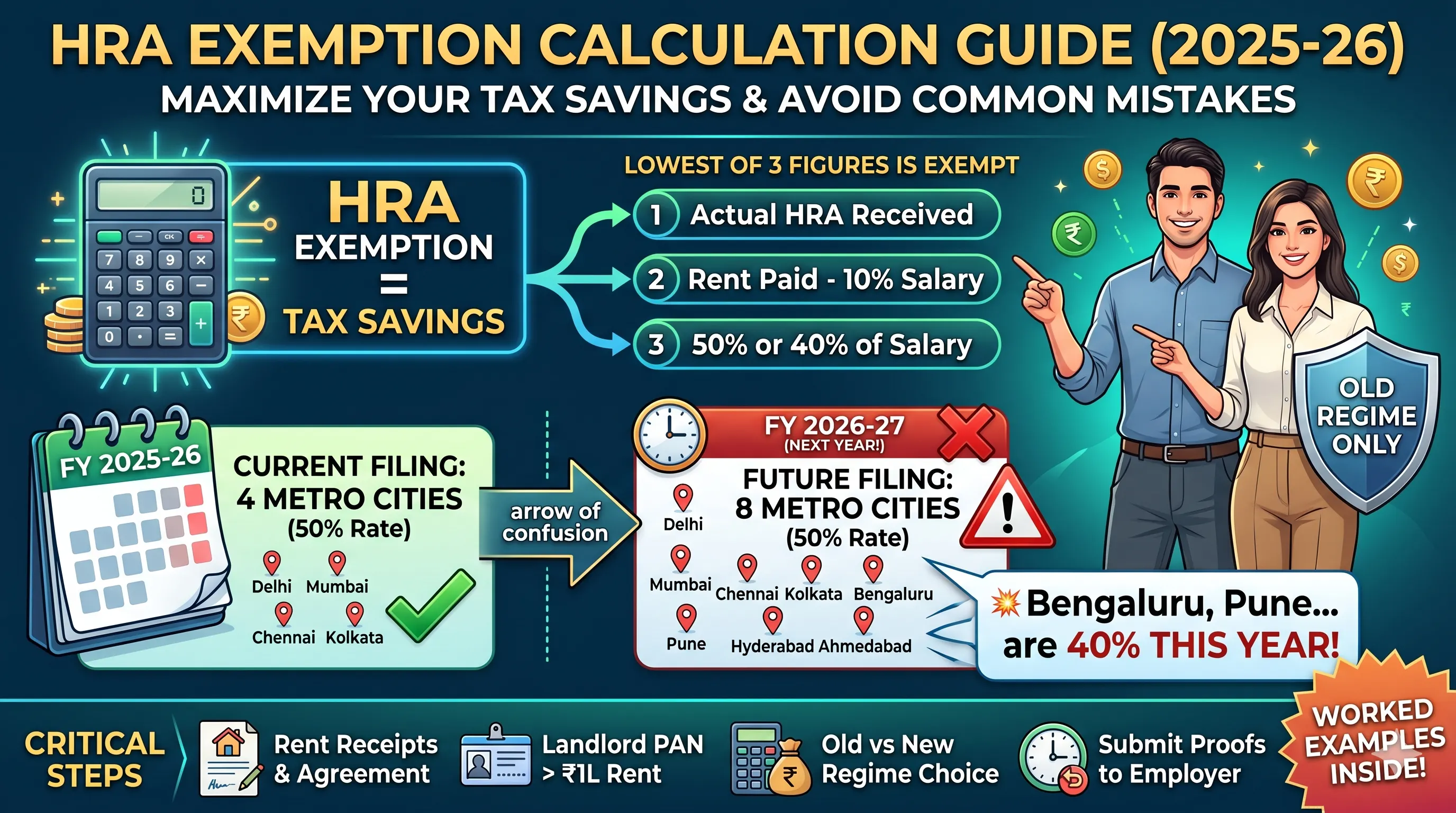

If you are filing your return for FY 2025-26 right now, you might have already seen the news that eight cities qualify for the higher 50% HRA exemption instead of four. That update is real, but it does not apply to the return you are filing today. It takes effect from FY 2026-27 onward. Mixing up the two years is the single most common HRA mistake we are seeing this filing season, and it can mean claiming an exemption you are not yet entitled to. This guide walks through both timelines clearly, with the exact formula and two full worked examples.

Quick Answer: What Is HRA Exemption?

House Rent Allowance (HRA) exemption lets a salaried employee who lives in rented accommodation and receives HRA as part of their salary exclude part of that allowance from taxable income, under the old tax regime only. The exempt amount is the lowest of three figures: the actual HRA received, the rent paid minus 10% of basic salary plus dearness allowance, and 50% of salary for metro cities or 40% for other cities. It is governed by Section 10(13A) of the Income-tax Act, 1961, read with Rule 2A of the Income-tax Rules.

Key Facts Table

Item | Detail |

|---|---|

Governing provision (FY 2025-26) | Section 10(13A), Income-tax Act, 1961, read with Rule 2A |

Governing provision (FY 2026-27 onward) | Schedule III, Income-tax Act, 2025 |

Available under | Old tax regime only, not available under the new tax regime |

Exemption formula | Least of: actual HRA received, rent paid minus 10% of salary, 50%/40% of salary |

Salary definition for HRA | Basic salary + Dearness Allowance (if part of retirement benefits) + commission as a fixed % of turnover |

Metro cities, FY 2025-26 (4 cities, 50% rate) | Delhi, Mumbai, Chennai, Kolkata |

Metro cities, FY 2026-27 onward (8 cities, 50% rate) | Delhi, Mumbai, Chennai, Kolkata, Bengaluru, Pune, Hyderabad, Ahmedabad |

Non-metro rate | 40% of salary |

PAN of landlord required if | Annual rent exceeds ₹1,00,000 |

No HRA component / self-employed alternative | Section 80GG deduction, subject to its own limits and Form 10BA |

Step-by-Step: How to Calculate Your HRA Exemption

Confirm you are on the old tax regime. HRA exemption is not available under the new tax regime at all, regardless of how much rent you pay or how much HRA your employer gives you. If you have not actively chosen the old regime for the year, check your Form 12BB submission or your regime selection on the e-filing portal.

Confirm HRA is part of your salary structure. Check your salary slip or Form 16. If HRA is not a listed component, you cannot claim this exemption, but you may be able to claim a deduction under Section 80GG instead.

Gather your three input numbers: actual HRA received during the year, actual rent paid during the year, and your basic salary plus dearness allowance (if it forms part of retirement benefits) for the same period.

Identify which city rate applies to you. For FY 2025-26 returns, only Delhi, Mumbai, Chennai and Kolkata qualify for the 50% rate; every other city, including Bengaluru, Pune, Hyderabad and Ahmedabad, uses 40% for this filing year. From FY 2026-27 onward, all eight cities use 50%.

Calculate all three components of the formula:

(a) Actual HRA received from your employer during the year

(b) Actual rent paid minus 10% of your basic salary plus DA for the same period

(c) 50% of basic salary plus DA (metro) or 40% (non-metro)

Take the lowest of the three. That figure, not the highest, is your exempt HRA. The remainder of your HRA, if any, is added to your taxable salary.

Collect supporting documents. Rent receipts, a signed rent agreement, and the landlord's PAN if annual rent exceeds ₹1,00,000. If you live with family and pay them rent, keep proof of an actual rent arrangement and ensure the family member reports it as rental income in their own return.

Report the exempt figure in the salary schedule of your ITR. Submit proofs to your employer during the year through Form 12BB so your monthly TDS reflects the correct figure, and if your employer did not factor it in, you can still claim the correct exemption directly while filing your return.

Worked Example 1: A Mumbai Employee (Metro, 50% Rate)

Rohan works in Mumbai, where the 50% rate applies for both FY 2025-26 and FY 2026-27, since Mumbai has always been on the metro list. His annual figures:

Basic salary + DA: ₹9,00,000 per year

HRA received from employer: ₹4,50,000 per year

Actual rent paid: ₹4,20,000 per year

Component (a): Actual HRA received = ₹4,50,000

Component (b): Rent paid minus 10% of salary = ₹4,20,000 − (10% × ₹9,00,000) = ₹4,20,000 − ₹90,000 = ₹3,30,000

Component (c): 50% of salary (metro) = 50% × ₹9,00,000 = ₹4,50,000

The lowest of ₹4,50,000, ₹3,30,000 and ₹4,50,000 is ₹3,30,000. Rohan can claim ₹3,30,000 as exempt HRA. The remaining ₹1,20,000 of his HRA (₹4,50,000 minus ₹3,30,000) is taxable as part of his salary.

Worked Example 2: A Bengaluru Employee Filing for FY 2025-26 (Non-Metro Rate Still Applies)

Ananya works in Bengaluru. This is the case where the year matters most. For her FY 2025-26 return, filed in 2026, Bengaluru is not on the 50% list yet, since the expanded eight-city list only takes effect from FY 2026-27. Her figures for FY 2025-26:

Basic salary + DA: ₹12,00,000 per year

HRA received from employer: ₹6,00,000 per year

Actual rent paid: ₹6,60,000 per year

Component (a): Actual HRA received = ₹6,00,000

Component (b): Rent paid minus 10% of salary = ₹6,60,000 − (10% × ₹12,00,000) = ₹6,60,000 − ₹1,20,000 = ₹5,40,000

Component (c): 40% of salary, since Bengaluru uses the non-metro rate for FY 2025-26 = 40% × ₹12,00,000 = ₹4,80,000

The lowest of ₹6,00,000, ₹5,40,000 and ₹4,80,000 is ₹4,80,000. Ananya's exempt HRA for FY 2025-26 is ₹4,80,000.

Now project the same figures forward to FY 2026-27, when Bengaluru moves to the 50% rate. Component (c) becomes 50% × ₹12,00,000 = ₹6,00,000. The lowest of ₹6,00,000, ₹5,40,000 and ₹6,00,000 is now ₹5,40,000, an increase of ₹60,000 in exempt HRA purely from the city reclassification, assuming her salary and rent stay the same. That is real money: at a 30% marginal tax slab, that single change saves roughly ₹18,720 in tax (including 4% cess) for the year, without Ananya doing anything differently.

The Eight-City Update: What Actually Changed and When

For years, only four cities, Delhi, Mumbai, Chennai and Kolkata, qualified for the 50%-of-salary HRA exemption rate, while every other city in India, regardless of actual rental costs, was capped at 40%. This meant an employee paying Mumbai-level rent in Bengaluru, Pune, Hyderabad or Ahmedabad was structurally capped at a lower exemption ceiling, even though market rent in these cities has risen sharply over the past decade.

From FY 2026-27 (Tax Year 2026-27) onward, under the new allowance structure that accompanies the Income-tax Act, 2025, four more cities, Bengaluru, Pune, Hyderabad and Ahmedabad, join the 50% list, bringing the total to eight. This change does not apply retroactively. If you are filing your return for FY 2025-26 right now, the old four-city list governs your calculation, and Bengaluru, Pune, Hyderabad and Ahmedabad still use the 40% rate for that specific filing year. The expanded list only becomes relevant from the financial year that began on 1 April 2026.

There is also a related compliance tightening worth knowing about. From FY 2026-27, employees claiming HRA under the old regime may need to clearly disclose their relationship with the landlord, particularly relevant if you pay rent to a parent, spouse or other relative, to support the genuineness of the rental arrangement.

HRA Under the New Tax Regime: There Is No Exemption

The new tax regime, the default regime since FY 2023-24, does not permit the HRA exemption at all. If you are on the new regime, your entire HRA received is added to taxable salary regardless of how much rent you actually pay or which city you live in. The new regime instead offers a flat standard deduction of ₹75,000 and a wider basic exemption structure, but no allowance-specific exemptions like HRA, LTA or Section 80C investments.

This is the central decision point for salaried employees every year: if you pay significant rent, particularly in one of the eight cities now eligible for the 50% rate, the old regime with HRA exemption, combined with other deductions like Section 80C and home loan interest, frequently produces a lower total tax outflow than the new regime's lower slab rates without exemptions. The only way to know for certain is to compute both regimes side by side using your actual numbers, since the better choice depends heavily on your specific salary structure and deduction profile.

If You Do Not Receive HRA: Section 80GG

Self-employed individuals and salaried employees whose salary structure does not include an HRA component are not without options. Section 80GG allows a deduction for rent paid, subject to the lowest of: ₹5,000 per month, 25% of total income, or actual rent paid minus 10% of total income. This deduction is only available under the old tax regime and requires filing Form 10BA. It is meaningfully smaller than HRA exemption in most cases, but it is the correct route if HRA was never part of your compensation structure.

Common HRA Mistakes to Avoid

Claiming the new eight-city list for an FY 2025-26 return. This is the mistake we expect to see most often this filing season, given how widely the city expansion has been reported. Check which financial year you are actually filing for before applying the 50% rate to a non-traditional metro city.

Forgetting to disclose landlord PAN above ₹1 lakh annual rent. If your annual rent crosses ₹1,00,000, you must report the landlord's PAN. Missing this can lead to your employer disallowing the exemption in TDS computation, even if you eventually claim it correctly in your ITR.

Claiming HRA while living in a self-owned house. HRA exemption requires actual rent payment for accommodation you do not own. If you live in your own house and do not pay rent, the entire HRA is taxable, with no exemption available.

Paying rent to a relative without documentation. HRA paid to parents or other relatives is allowed, but only with genuine rent receipts, a documented arrangement, and that family member declaring the rent as income in their own return. Without this, the claim is at high risk of disallowance on scrutiny.

Using gross salary instead of basic salary plus DA. The 50%/40% calculation and the 10% deduction in component (b) both use basic salary plus dearness allowance forming part of retirement benefits, not your full gross CTC, which typically includes many other allowances that do not enter this formula.

How HRA Interacts With a Home Loan

You can claim both HRA exemption and home loan interest deduction under Section 24(b) in the same year, provided the situations are genuinely different: for example, you own a house in one city but rent accommodation in another city for work reasons, or your owned property is still under construction or not yet habitable. Both claims require maintaining the relevant documentation independently, since tax authorities scrutinise combined HRA-plus-home-loan claims more closely than either claim alone.

References

Income Tax Department, Government of India, Section 10(13A) and Rule 2A guidance: incometax.gov.in

Income Tax Department, official income tax slab and allowance notifications: incometaxindia.gov.in

Calculate this for your own numbers

HRA Exemption Calculator, enter your salary, rent and city to get your exact exempt amount for the correct financial year

Related read: New Income Tax Rules 2026, every change to allowances and HRA explained

Related read: Form 121 income tax, the new TDS exemption declaration

Income tax aur GST dono ke updates ek hi jagah chahiye? Hamara WhatsApp channel join karo, naye rules aur deadline reminders seedha aapke phone par, bilkul free.