Advance Tax: Due Dates, Instalments and Calculation (2025-26)

Advance tax does not wait for you to file your return. If your total tax liability for the year, after subtracting TDS and TCS already deducted, crosses ₹10,000, the law expects you to pay it in instalments through the year, not as a single payment in July. Miss an instalment, and interest under Section 234B or Section 234C starts accumulating automatically, with no notice and no warning. This guide lays out the exact due dates, who is exempt, and a complete worked calculation so you know precisely what to pay and when.

Quick Answer: What Is Advance Tax?

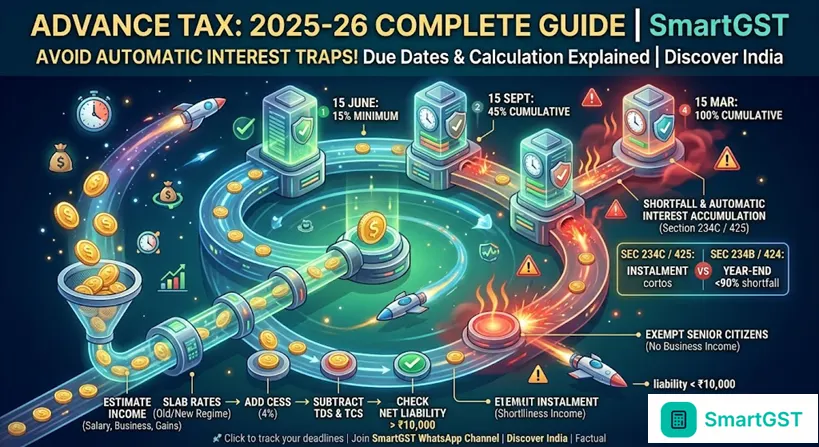

Advance tax is income tax paid during the financial year itself, in instalments, rather than as a lump sum after the year ends. It applies to any taxpayer, salaried, business owner, freelancer or professional, whose estimated tax liability for the year, after reducing TDS and TCS already deducted, is ₹10,000 or more. It must be paid in four instalments by 15 June, 15 September, 15 December and 15 March, with specific cumulative percentages due at each date.

Key Facts Table

Item | Detail |

|---|---|

Who must pay | Any taxpayer with estimated tax liability of ₹10,000 or more after TDS/TCS |

Old Act reference (FY 2025-26) | Sections 207 to 219, Income-tax Act, 1961 |

New Act reference (Tax Year 2026-27 onward) | Sections 403 to 410, Income-tax Act, 2025 (threshold under Section 404) |

1st instalment | 15 June, at least 15% of total tax liability |

2nd instalment | 15 September, at least 45% of total tax liability (cumulative) |

3rd instalment | 15 December, at least 75% of total tax liability (cumulative) |

4th instalment | 15 March, 100% of total tax liability (cumulative) |

Presumptive taxpayers (Section 44AD / 44ADA) | 100% in a single instalment by 15 March, no quarterly split |

Senior citizen exemption | Resident individuals aged 60+ with no business or professional income are fully exempt |

Interest for shortfall by year-end | Section 234B (old) / Section 424 (new), 1% per month on the shortfall below 90% of assessed tax |

Interest for instalment deferment | Section 234C (old) / Section 425 (new), 1% per month for each missed instalment threshold |

Step-by-Step: How to Calculate and Pay Your Advance Tax

Estimate your total income for the financial year. Include salary, business or professional income, capital gains, rental income, interest income and any other source. This is necessarily an estimate early in the year, refine it as the year progresses and your actual income becomes clearer.

Apply the applicable slab rates or special rates. Use either the old regime or new regime slabs, whichever you have chosen, and apply the correct rate for income types taxed separately, such as short-term or long-term capital gains.

Add surcharge and cess. Apply the applicable surcharge if your income crosses the relevant threshold, and add 4% health and education cess on the tax plus surcharge.

Subtract TDS and TCS already deducted or expected to be deducted during the year. This includes TDS on salary, TDS on FD interest, TDS deducted by clients on professional payments, and any TCS collected on your purchases.

Check if the remaining liability is ₹10,000 or more. If it is below this threshold, you do not need to pay advance tax at all for the year.

Calculate each instalment using the cumulative percentage schedule. Work out 15%, 45%, 75% and 100% of your estimated total liability for the four due dates, and pay only the incremental amount due at each stage if you have already paid an earlier instalment.

Pay through the income tax e-filing portal using Challan 280 (or its equivalent under the new portal structure), selecting "Advance Tax" as the payment type and the correct assessment year or tax year.

Revise your estimate at each instalment date. If your income estimate changes significantly, for example a large bonus, capital gain, or a drop in business income, recalculate your remaining instalments based on the updated figure rather than sticking to your original estimate.

Reconcile at year-end. Compare your total advance tax paid against your final assessed tax liability when you file your return. Any shortfall becomes self-assessment tax, payable with interest if applicable. Any excess is refunded.

Worked Example: A Freelancer With Mixed Income

Vikram is a freelance consultant who also earns rental income. For FY 2025-26, he estimates his figures as follows:

Professional income (after expenses): ₹14,00,000

Rental income (after standard deduction): ₹2,40,000

TDS already deducted by clients during the year: ₹1,40,000

He opts for the new tax regime

Step 1: Estimate total income. ₹14,00,000 + ₹2,40,000 = ₹16,40,000

Step 2: Apply new regime slab rates for FY 2025-26. ₹0 to ₹4,00,000: Nil ₹4,00,000 to ₹8,00,000: 5% of ₹4,00,000 = ₹20,000 ₹8,00,000 to ₹12,00,000: 10% of ₹4,00,000 = ₹40,000 ₹12,00,000 to ₹16,00,000: 15% of ₹4,00,000 = ₹60,000 ₹16,00,000 to ₹16,40,000: 20% of ₹40,000 = ₹8,000

Tax before cess = ₹20,000 + ₹40,000 + ₹60,000 + ₹8,000 = ₹1,28,000

Step 3: Add 4% cess. ₹1,28,000 × 1.04 = ₹1,33,120

Step 4: Subtract TDS already deducted. ₹1,33,120 − ₹1,40,000 = a negative figure, meaning his TDS actually exceeds his estimated liability.

In this scenario, Vikram has no advance tax obligation at all, since his TDS already covers his estimated tax in full, and he may even be due a refund when he files his return. This example illustrates why Step 4 matters so much: many freelancers assume they owe advance tax simply because they have business income, without first netting off TDS already deducted by their clients.

Now consider a variant. If Vikram's TDS for the year was only ₹70,000 instead of ₹1,40,000, his remaining liability would be ₹1,33,120 − ₹70,000 = ₹63,120, which exceeds ₹10,000, so advance tax applies. His instalment schedule would then be:

Due Date | Cumulative % | Cumulative Amount | Instalment Due |

|---|---|---|---|

15 June 2025 | 15% | ₹9,468 | ₹9,468 |

15 September 2025 | 45% | ₹28,404 | ₹18,936 |

15 December 2025 | 75% | ₹47,340 | ₹18,936 |

15 March 2026 | 100% | ₹63,120 | ₹15,780 |

Each instalment after the first is the cumulative amount due at that date, minus what was already paid in the previous instalment, not the full cumulative figure again.

The Four-Instalment Schedule, Explained

Due Date | Minimum Cumulative Tax Paid | Applies To |

|---|---|---|

On or before 15 June | 15% of estimated tax liability | All taxpayers except those under presumptive taxation |

On or before 15 September | 45% of estimated tax liability | All taxpayers except those under presumptive taxation |

On or before 15 December | 75% of estimated tax liability | All taxpayers except those under presumptive taxation |

On or before 15 March | 100% of estimated tax liability | All taxpayers, including presumptive taxpayers (single instalment) |

If you pay any tax on or before 31 March of the financial year, even after the 15 March due date, it still counts as advance tax for the year, though you may still owe interest under Section 234C for the shortfall against the 15 March threshold specifically.

Who Is Exempt From Paying Advance Tax

Resident senior citizens without business or professional income. If you are 60 years or older, resident in India, and your income consists only of salary, pension, interest, rent or capital gains, with no income from business or profession, you are fully exempt from advance tax, even if your total tax liability exceeds ₹10,000.

Taxpayers below the ₹10,000 threshold. If your estimated tax liability after TDS and TCS is below ₹10,000 for the year, advance tax does not apply to you at all, regardless of your income level, since the entire liability falls below the trigger amount.

Presumptive taxpayers, with a modified obligation rather than a full exemption. If you have opted for Section 44AD or Section 44ADA, you are not exempt from advance tax, but your obligation is simplified: you pay 100% of your estimated liability in a single instalment by 15 March, rather than following the four-instalment schedule. For the full mechanics of this scheme, see our guide on Section 44AD for GST dealers.

Interest for Missing or Underpaying Advance Tax

Two separate interest provisions apply, and they are frequently confused with each other since both charge 1% per month, but they are triggered by different failures.

Section 234B (old Act) / Section 424 (new Act): shortfall at year-end. If the advance tax you paid by 31 March is less than 90% of your final assessed tax liability, interest at 1% per month applies from 1 April following the financial year until the date you actually pay the balance, calculated on the assessed tax or the shortfall amount, as applicable.

Section 234C (old Act) / Section 425 (new Act): missed instalment thresholds. If you paid less than the required cumulative percentage at any of the four due dates, interest at 1% per month applies on the specific shortfall for that instalment, generally for three months for the first three instalments and one month for the final instalment, regardless of whether you catch up by year-end.

Both provisions can apply in the same year for different reasons: you might catch up to 95% of your liability by the 15 March deadline, avoiding Section 234B entirely, but still owe Section 234C interest for an instalment you underpaid back in September.

Note for taxpayers spanning the transition year: if your advance tax obligation and any related default arose during FY 2025-26, the consequential interest calculation continues to be governed by the old Income-tax Act, 1961, under Sections 234B and 234C, even if the interest is actually computed or levied after 1 April 2026. The new Sections 424 and 425 apply to obligations and defaults arising in Tax Year 2026-27 and later.

A Note on Estimating Income Through the Year

Advance tax is inherently a forecasting exercise, especially for business owners and freelancers whose income is not as predictable as a fixed salary. A few practical habits reduce the risk of significant interest charges:

Revisit your estimate at each instalment date, not just once at the start of the year. Income from freelance work, business operations, and capital gains can change substantially over a few months. Recalculating at each due date, rather than carrying forward your June estimate unchanged through December, keeps your instalments closer to your actual liability.

Account for capital gains and one-off income as they arise. If you sell shares, property, or other capital assets partway through the year, that gain typically needs to be factored into your very next advance tax instalment, not deferred to the final 15 March payment, to avoid Section 234C interest on that specific instalment.

Do not ignore TDS already reflected in Form 26AS. Cross-check the TDS your clients or employer have actually deposited against what you expect, since a mismatch here directly changes how much advance tax you genuinely owe.

How Advance Tax Connects to Your GST Filings

If you run a GST-registered business, your GST output liability and your income tax advance tax obligation are computed on entirely different bases, GST on the value of taxable supplies made, and advance tax on your estimated net taxable income, but both require the same underlying discipline of tracking your numbers through the year rather than scrambling at year-end. Use our Annual Summary tool to get a monthly breakdown of your GST liability, which is often a useful proxy for estimating how your turnover, and therefore your likely business income, is trending through the year. And if you have ever missed a GST filing deadline alongside a tax due date, our GST Late Fee and Penalty guide walks through the exact penalty calculation so you know what you are dealing with on that side too.

References

Income Tax Department, Government of India, advance tax payment guidance: incometax.gov.in

Income Tax Department, Section 234B and Section 234C statutory text: incometaxindia.gov.in

Calculate and track your own deadlines

Advance Tax Calculator, enter your estimated income and TDS to get your exact instalment-wise schedule

Due Date Calendar, track every GST and tax filing deadline in one place

Related read: Section 44AD for GST dealers, presumptive tax explained

GST aur income tax dono ki deadlines ek jagah track karni hain? Hamara WhatsApp channel join karo, reminders aur fresh updates seedha aapke phone par, bilkul free.