HSN Code for Mobile Phones 2025: 8517 Rate, 8-Digit Codes, Accessories, and ITC Rules

India sells over 15 crore smartphones every year. Every single one of those transactions requires a correct HSN code on the invoice. And yet, in most small mobile shops, repair centers, and e-commerce seller accounts across the country, the wrong code gets used routinely.

Getting the HSN code wrong does not just mean a filing issue. It means your buyer cannot claim accurate ITC, it means a mismatch in GSTR-1, and depending on the code used, it can mean the wrong GST rate was applied either excess tax collected from the customer or short tax paid to the government. Both create problems.

This guide gives you every HSN code in the mobile category, the correct GST rates, which codes changed under GST 2.0, and how ITC works for business phone purchases.

What is an HSN Code and Why Does It Matter on Your Invoice

HSN stands for Harmonized System of Nomenclature. It is an internationally standardized product classification system. Under India's GST law, every business must mention the correct HSN code on their tax invoices so that the government can identify the product, apply the right tax rate, and track trade data.

HSN codes have different digit requirements depending on your turnover:

Turnover below Rs. 5 crore: 4-digit HSN on B2B invoices (optional for B2C)

Turnover Rs. 5 crore to Rs. 50 crore: 6-digit HSN mandatory

Turnover above Rs. 50 crore: 8-digit HSN mandatory

For a mobile phone shop or electronics distributor, the 4-digit or 6-digit HSN is often enough for GST compliance. But for large distributors and manufacturers, the full 8-digit code is required and must be exact.

Use the SmartGST HSN Code Finder to search any product name and get the correct HSN code and current GST rate instantly.

HSN Code 8517: Mobile Phones and Telecom Equipment

The primary HSN heading for mobile phones is 8517. This heading covers:

"Telephone sets, including smartphones and other phones for cellular networks or for other wireless networks; other apparatus for the transmission or reception of voice, images or other data, including apparatus for communication in a wired or wireless network."

Everything you sell in a standard mobile shop iPhones, Androids, 5G phones, 4G phones, feature phones, basic calling-only handsets falls under this heading.

GST Rate on HSN 8517: 18%

The HSN code for mobile phones in India is 8517 and the applicable GST rate is 18%. This applies uniformly to all smartphones and feature phones. However, mobile accessories have different codes chargers fall under 8504 and earphones under 8518. Using 8517 for everything is a common mistake that leads to ITC rejection.

6-Digit and 8-Digit HSN Sub-Codes for Mobile Phones

For businesses that need the more detailed codes, here is the breakdown under Chapter 85:

HSN Code | Description | GST Rate |

|---|---|---|

8517 12 | Telephones for cellular or wireless networks (smartphones, mobile handsets) | 18% |

8517 12 11 | Mobile phones other than push-button type (touchscreen smartphones) | 18% |

8517 12 19 | Mobile phones push-button type (basic feature phones, keypad phones) | 18% |

8517 14 | Base stations (mobile towers, repeaters) | 18% |

8517 62 | Machines for the reception, conversion, and transmission of voice/data | 18% |

8517 69 | Other communication apparatus (includes some routers and modems) | 18% |

For most mobile retailers, 8517 12 11 covers smartphones and 8517 12 19 covers feature phones. If you are not sure which sub-code applies to your specific model, the 4-digit 8517 is safe at your turnover level. Confirm with your CA if you are a large distributor required to use 8-digit codes.

HSN Codes for Mobile Accessories These Are NOT 8517

This is where most businesses make the mistake. Mobile accessories are NOT classified under 8517. Each type of accessory has its own HSN code. Putting chargers or earphones under 8517 on your invoice is technically a misclassification.

Here is the correct HSN code for every major mobile accessory:

Chargers and Adapters HSN 8504

Mobile phone chargers fall under HSN 8504, which covers "Electrical transformers, static converters, and inductors." This includes wall chargers (both standard and fast-charge), USB power adapters, wireless chargers (inductive charging pads), and multi-port USB hubs used for charging.

GST Rate: 18%

The rate matches the phone, so on a bundled invoice (phone plus charger in box), the effective tax is the same. But when you sell chargers separately, HSN 8504 must appear on that invoice, not 8517.

Earphones, Earbuds, and Headphones HSN 8518

HSN 8518 covers "Microphones and their stands; loudspeakers, whether or not mounted in their enclosures; headphones and earphones; audio-frequency electric amplifiers; electric sound amplifier sets."

All wired earphones, wireless earbuds (like AirPods and Galaxy Buds), over-ear headphones, and gaming headsets fall here.

GST Rate: 18%

Power Banks HSN 8507

Power banks are classified under HSN 8507 which covers "Electric accumulators, including separators therefor, whether or not rectangular (including square)."

GST Rate: 18%

Phone Cases, Covers, and Protective Accessories

This depends on the material:

Plastic or silicone phone covers: HSN 3926 (articles of plastic) GST 18%

Leather or PU leather cases: HSN 4205 or 4206 GST 12% (these stayed at 12% under GST 2.0 for genuine leather; check specific sub-heading)

Fabric pouches: HSN 6307 GST 5%

This is where getting it wrong costs money. A leather phone case is not 18% GST. Using 8517 for it and charging 18% means you over-collected tax. Using the wrong code in GSTR-1 creates a product classification mismatch.

Screen Protectors and Tempered Glass HSN 7007 or 3920

Tempered glass screen protectors fall under HSN 7007 (safety glazed glass). Plastic film protectors fall under HSN 3920 (other plates, sheets, film of plastics).

GST Rate: Both at 18%

Selfie Sticks and Tripods HSN 9620

Tripods and selfie sticks are classified under HSN 9620 monopods, bipods, tripods, and similar articles.

GST Rate: 18%

Memory Cards and Storage HSN 8523

MicroSD cards, SD cards, and USB pen drives fall under HSN 8523 discs, tapes, solid-state non-volatile storage devices.

GST Rate: 18%

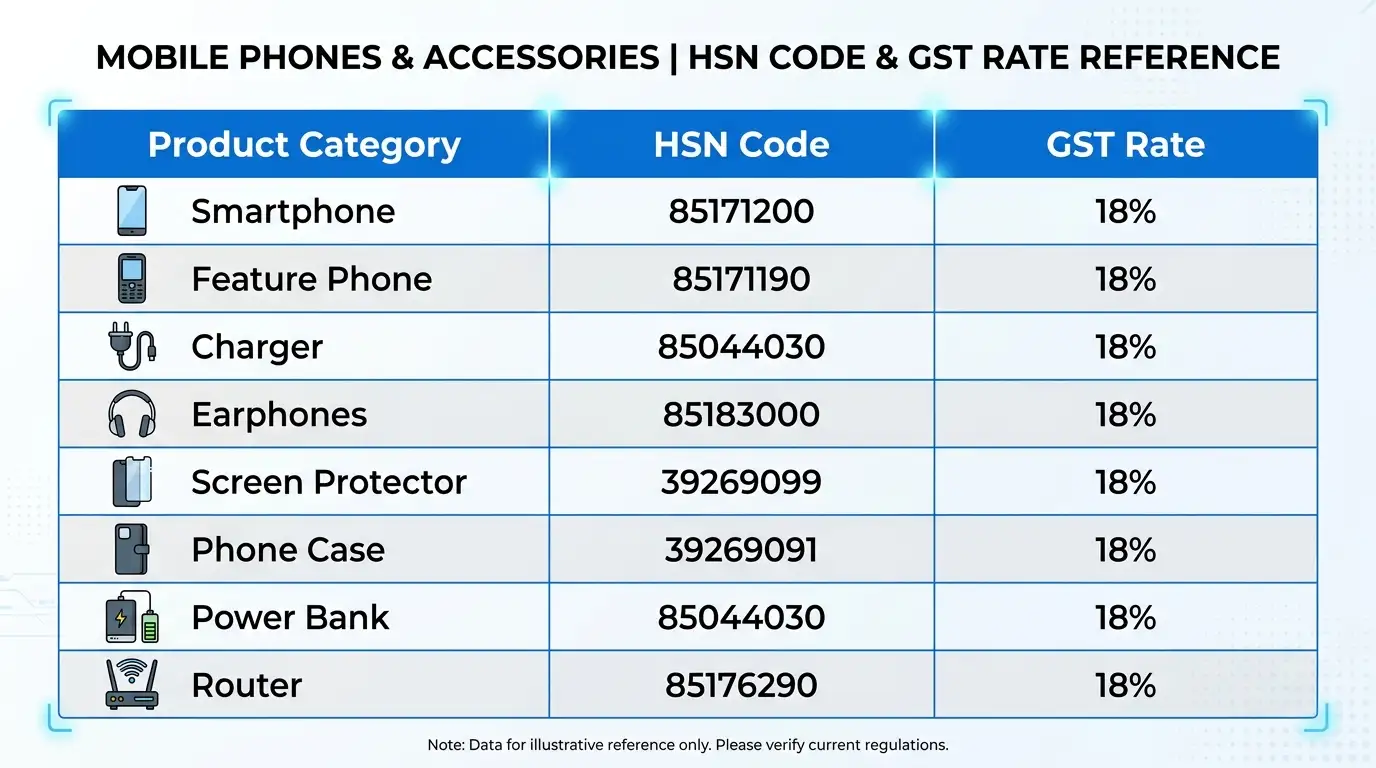

Complete Quick-Reference Table

Product | HSN Code | GST Rate |

|---|---|---|

Smartphones (touchscreen) | 8517 12 11 | 18% |

Feature phones (keypad) | 8517 12 19 | 18% |

Charger / USB adapter | 8504 | 18% |

Wireless charger / charging pad | 8504 | 18% |

Wired earphones | 8518 | 18% |

Wireless earbuds / AirPods type | 8518 | 18% |

Over-ear headphones | 8518 | 18% |

Power bank | 8507 | 18% |

Plastic / silicone phone case | 3926 | 18% |

Leather phone case | 4205/4206 | 12%* |

Fabric phone pouch | 6307 | 5% |

Tempered glass screen protector | 7007 | 18% |

Plastic film screen protector | 3920 | 18% |

Memory card / MicroSD | 8523 | 18% |

USB pen drive | 8523 | 18% |

Selfie stick / tripod | 9620 | 18% |

Mobile router / portable WiFi | 8517 69 | 18% |

Mobile tower / base station | 8517 14 | 18% |

*Leather case rate — verify specific sub-heading with your CA. GST 2.0 moved most leather goods to 18%, but some sub-categories may differ. Confirm before invoicing.

To check the current rate on any product instantly, use the SmartGST HSN Finder or the GST Rate Checker 2026.

How IGST, CGST, and SGST Work on Mobile Sales

Understanding the tax split matters for your invoice and your GSTR-1 filing.

Intra-state sale (seller and buyer in the same state): Total GST = 18% split as 9% CGST + 9% SGST

So a Rs. 20,000 phone sold from a Delhi shop to a Delhi customer: Rs. 1,800 CGST + Rs. 1,800 SGST = Rs. 3,600 total GST. Invoice shows Rs. 20,000 + Rs. 1,800 CGST + Rs. 1,800 SGST = Rs. 23,600.

Inter-state sale (seller in one state, buyer in another): Total GST = 18% as IGST only (no split)

A phone shipped from a Mumbai warehouse to a Bengaluru buyer: Rs. 3,600 IGST on a Rs. 20,000 phone.

This classification also determines how you report the sale in GSTR-1 intra-state goes into one table, inter-state into another. Getting this wrong creates a Table 3.2 mismatch in GSTR-3B.

ITC on Mobile Phone Purchases for Businesses

If your business buys mobile phones for official use, you can generally claim ITC on the GST paid. But the rules are specific.

When ITC is allowed:

Phones purchased for employees to use in official work (client calls, field operations, delivery tracking, etc.)

Phones purchased as stock for trading (mobile shops and distributors claim full ITC)

Phones purchased for use in providing taxable services

When ITC is blocked (Section 17(5) of CGST Act):

Phones purchased as gifts or free samples given to customers or staff

Phones purchased for personal use of directors, owners, or employees where the business is not obligated to provide them

Phones included in any plan where the employer provides the device as a perquisite that is specifically excluded

The ITC rule for phones is the same as for most business assets the phone must be used for business purposes and the invoice must be in your business name with your GSTIN. The supplier must have uploaded the invoice in their GSTR-1 for it to appear in your GSTR-2B.

For mobile retailers and distributors, ITC on stock purchases is fully available. The GST paid on phones you buy to sell is credited against the GST you collect when you sell them.

Calculate your eligible ITC using the SmartGST ITC Calculator.

GST on Mobile Phone Imports

Imported mobile phones are subject to IGST at 18% on the assessable value, which includes the cost of the phone, insurance, freight charges, and applicable customs duty.

This means the 18% IGST on an imported phone applies on a higher base than the domestic sale price, because customs duty has already been added into the value before IGST is calculated.

For businesses importing phones commercially (distributors, authorized importers), IGST paid at customs is eligible as ITC against output GST on domestic sales. This is an important cash flow consideration. The ITC on imports gets reflected in GSTR-2B once the Bill of Entry is filed.

Composite Supply vs Mixed Supply in Bundled Mobile Deals

This comes up most often when phones are sold with accessories in a box, or when a retailer creates bundle offers.

Composite supply: A phone sold with its charger and earphones in the original manufacturer box. The principal supply is the phone (8517 at 18%). Since the charger and earphones are naturally bundled with the phone and sold together, the entire bundle is taxed at the phone rate 18%.

Mixed supply: A retailer creates their own bundle: a phone plus a power bank plus a phone case (from different manufacturers, assembled for a promotional offer). Here, each item has its own HSN and rate. You cannot apply a single rate to the whole bundle. Each product in your invoice must show its own HSN code and GST rate.

Mishandling this distinction is a common audit point for mobile retailers running festival sales bundles.

Mobile Repair Services GST Rate

If you run a mobile repair center, the service you provide attracts GST separately from the parts used.

Repair services (SAC Code 9987): 18% GST on the service charge

Spare parts supplied during repair: Charged at the applicable GST rate for that part generally 18% for most electronics components.

When both service and parts are billed together on one invoice, it is typically treated as a composite supply where the principal supply determines the rate. If the repair service is the principal supply and the parts are incidental, 18% on the total is the standard practice. Confirm with your CA for large-value repair jobs with expensive parts.

How to Show HSN Code on Your Invoice Correctly

The HSN code must appear in the "HSN/SAC" field on your GSTR-compliant tax invoice. For your billing software:

B2B sales: HSN is mandatory based on your turnover (4, 6, or 8 digits)

B2C sales below Rs. 2.5 lakh: HSN optional for businesses under Rs. 5 crore turnover

B2C sales above Rs. 2.5 lakh: HSN mandatory regardless of turnover

E-invoice: HSN is mandatory in the e-invoice JSON schema for all B2B supplies regardless of item value

If your billing software pre-fills HSN codes from a product master, audit the product master periodically to ensure codes are current. HSN rate schedules do get updated by the GST Council and using an outdated code can result in wrong rates being applied.

Data Accuracy Disclaimer

All HSN codes and GST rates in this article are based on the CBIC GST Rate Schedule under Chapter 85 and the CBIC Notification dated September 17, 2025 implementing GST 2.0 rate changes effective September 22, 2025. HSN classifications and GST rates are subject to revision by the GST Council. Always verify with the official CBIC website at cbic-gst.gov.in or the GST portal rate finder before invoicing large transactions. This article is for reference and information purposes and does not constitute professional tax advice.

References:

CBIC GST Rate Schedule, Chapter 85, Heading 8517

56th GST Council Meeting, September 3, 2025 Rate rationalization decisions

CBIC Notification September 17, 2025 (GST 2.0 rate changes, effective September 22, 2025)

HSN Code notification under Customs Tariff Act, Chapter 85

GST Council Fitment Committee report on electronics, 2025

Get Instant HSN Codes for Any Product Free

Not sure about the HSN code for a specific product you sell? Use the SmartGST HSN Code Finder search by product name and get the correct HSN code and current GST rate in under 10 seconds. No signup needed.

For all upcoming GST updates, rate changes, and HSN amendments, join the SmartGST WhatsApp Channel and get notified the moment CBIC issues a new notification.

Join SmartGST WhatsApp Channel Free GST Updates

No spam. Only GST updates that affect your business.