GST DRC-07 Notice Received? Here Is Exactly What It Means and What You Must Do in the Next 90 Days

By SmartGST Editorial Team | Updated: April 2026 | 13 min read

If you just received a DRC-07 notice on your GST portal, stop what you are doing and read this first. Most businesses panic, delay, and end up paying 3x more than they should. I am going to walk you through exactly what this notice means, why you got it, and the precise steps to take — whether you agree with the demand or want to fight it.

What Is a GST DRC-07 Notice? (And Why It Is Different From Every Other GST Notice)

I have seen thousands of businesses confuse DRC-07 with a routine GST query. It is not.

DRC-07 is the GST department's final demand order. Full stop.

It stands for Demand and Recovery Certificate Form 07. When the GST Proper Officer issues a DRC-07 against you, it means the adjudication process is complete. The officer has reviewed your case, considered any reply you may have filed, and passed a final order confirming the exact amount you owe — tax, interest, and penalty combined.

The entire GST notice journey looks like this:

plaintextcopyASMT-10 (Scrutiny Notice)

↓

DRC-01 (Show Cause Notice — SCN)

↓

Your Reply (or no reply)

↓

DRC-07 (Final Demand Order) ← You are here

↓

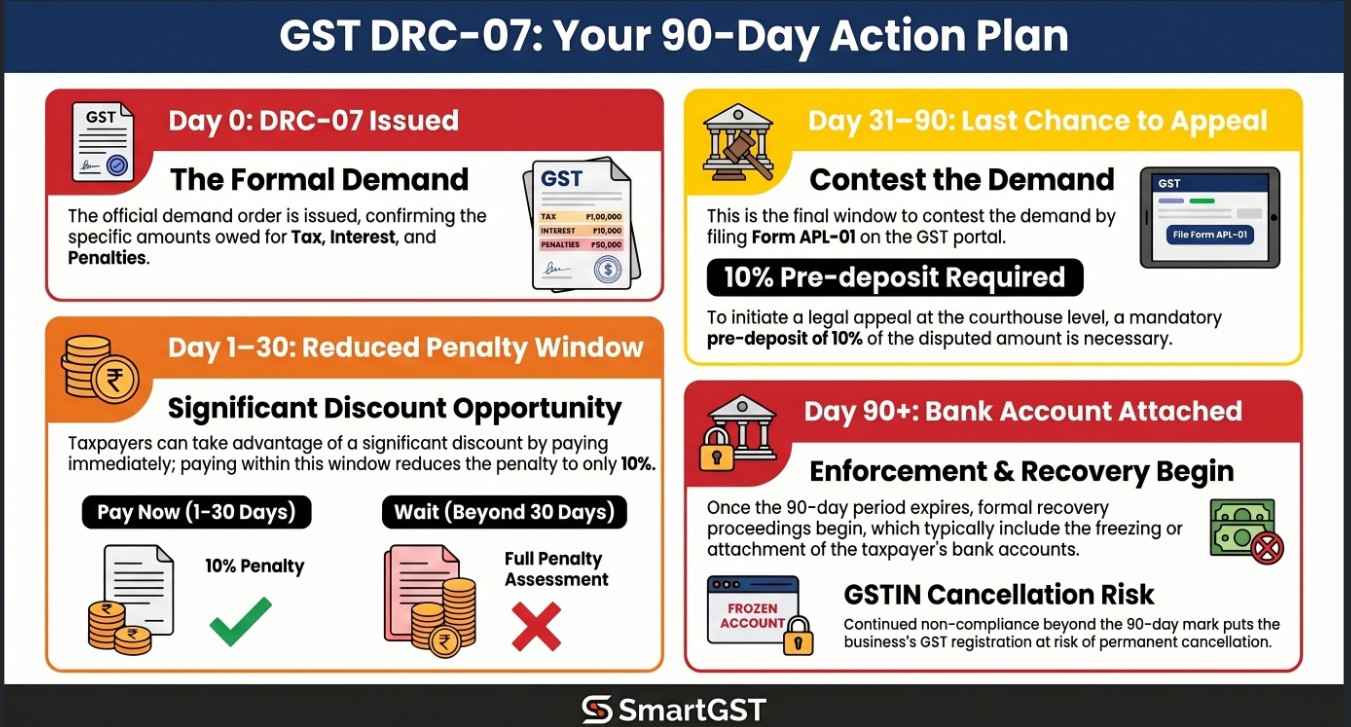

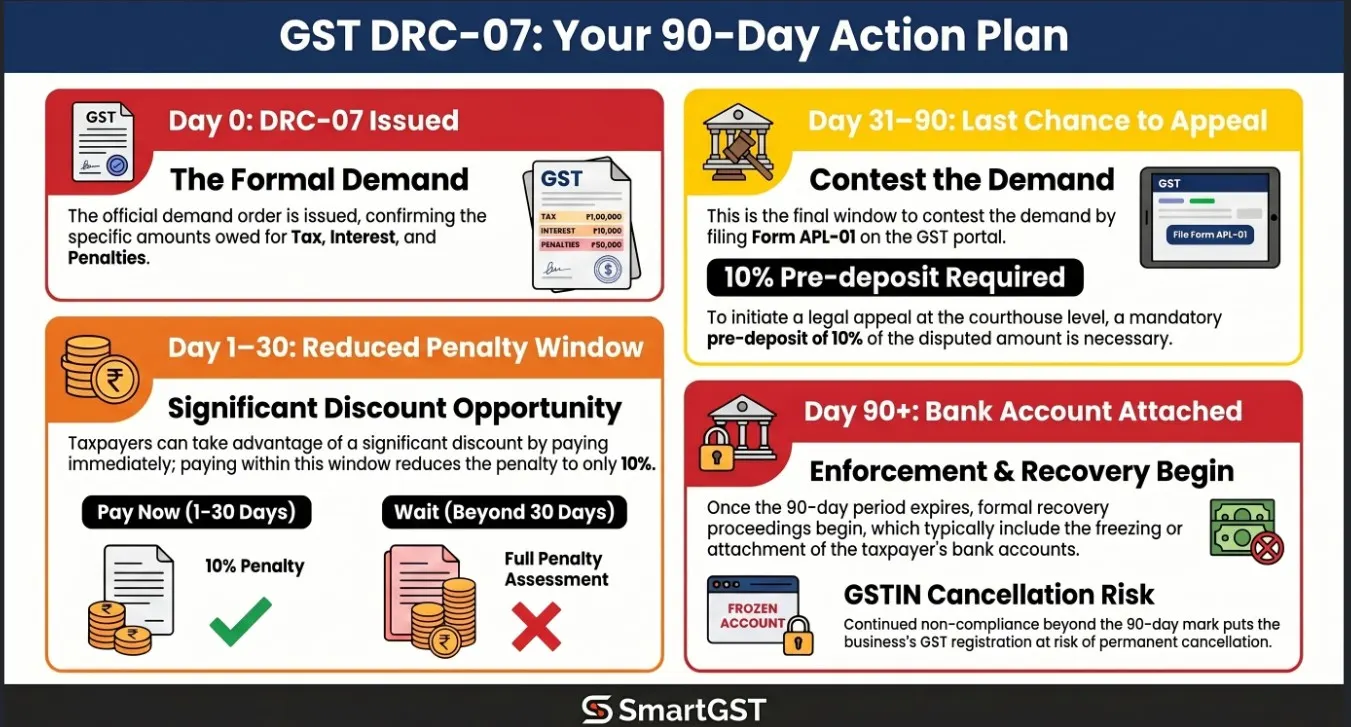

Recovery Proceedings if ignoredOnce DRC-07 lands in your GST portal, the department considers the matter closed from their end. You now have exactly 3 months to either pay the demand or file an appeal. Not 3 months from when you notice it 3 months from the date of the order.

What Does a DRC-07 Notice Contain?

Every DRC-07 order contains these specific details:

Field | What It Means |

|---|---|

Order Number | Your unique case reference note this down first |

Tax Period | Which financial year / month the demand relates to |

Nature of Issue | ITC mismatch, short payment, excess refund, etc. |

Tax Demanded | The base GST amount the officer says you owe |

Interest u/s 50 | 18% per annum calculated from due date to current date |

Penalty | 10% of tax (Section 73) or up to 100% (Section 74 for fraud) |

Total Payable | Tax + Interest + Penalty combined |

The interest alone can be brutal. On a ₹5 lakh demand that has been pending for 2 years, the interest adds up to ₹1.8 lakh just sitting there compounding every day you delay.

💡 Use the SmartGST GST Interest Calculator to instantly calculate how much interest has accumulated on your demand before you decide whether to pay or appeal.

7 Real Reasons Businesses Receive DRC-07 (With Examples)

1. ITC Mismatch Between GSTR-2B and GSTR-3B

This is the most common reason I see. You claimed Input Tax Credit in GSTR-3B based on what your vendor told you but that vendor never actually filed their GSTR-1. The system auto-matches your ITC claim against GSTR-2B, finds a gap, and initiates proceedings.

Real example: A Delhi-based manufacturer claimed ₹4.2 lakh ITC in GSTR-3B for FY 2022-23. Three vendors accounting for ₹1.8 lakh of that ITC never filed their returns. Result: DRC-07 for ₹1.8 lakh + interest + 10% penalty = ₹2.3 lakh total demand.

🔍 Before your next payment to any vendor, always verify their GSTIN is active using the SmartGST GSTIN Validator. A payment to a vendor with a fake or cancelled GSTIN means your ITC claim fails entirely.

2. GSTR-1 and GSTR-3B Mismatch

Your outward supplies declared in GSTR-1 do not match what you reported in GSTR-3B. Happens constantly in businesses where the sales team and accounts team work in silos.

3. Non-Reply to an Earlier DRC-01 Notice

This is the most avoidable reason on this list. If you received a Show Cause Notice (DRC-01) and ignored it or your CA forgot to reply the officer passes an ex parte order and issues DRC-07 directly without hearing your side. You lose your chance to explain before the demand is confirmed.

4. Short Payment of Output Tax

Tax calculated in your returns does not match tax actually paid. Even a ₹200 gap can trigger proceedings if it crosses a financial year boundary.

5. Excess ITC Under Section 17(5) Blocked Credits

You claimed ITC on categories that are completely blocked under GST law personal use vehicles, food and beverages, club memberships, health insurance for employees in most cases. The system flags these during scrutiny.

6. Income Tax vs GST Turnover Mismatch

Your ITR shows ₹80 lakh turnover. Your GST returns show ₹65 lakh. The system auto-detects this gap and your case gets picked up for scrutiny. Common among freelancers, consultants, and eCommerce sellers who mix exempt and taxable supplies.

7. Excess Refund Already Released

If you claimed a GST refund that was sanctioned but later found to be incorrect the department issues DRC-07 to recover the excess amount.

What Happens If You Ignore a DRC-07 Notice?

I want to be direct here because this is where people make catastrophic mistakes.

Ignoring DRC-07 does not make it go away. It makes it exponentially worse.

Here is the escalation chain the department follows after issuing DRC-07:

Day 1–90: You are expected to pay or file an appeal. Interest keeps running at 18% per annum on the outstanding amount.

After 90 days (no action): Recovery proceedings begin under Section 79 of the CGST Act. The department can:

Deduct money directly from any GST refund you are owed

Issue recovery notice to your bank under Section 79(1)(c) your bank account gets attached and funds are recovered without your permission

Attach your property, plant, or equipment

Issue notice to your debtors to pay outstanding amounts directly to the government instead of you

Extreme cases: Provisional attachment of all business assets under Section 83. GSTIN cancellation under Section 29.

A ₹2 lakh demand ignored for 6 months can balloon to ₹3.5–4 lakh by the time recovery proceedings conclude plus the operational chaos of a frozen bank account.

You Have Two Options After Receiving DRC-07

Option 1: Pay the Demand (If You Agree With It)

If after reviewing the DRC-07 order you agree the demand is correct or the amount is small enough that fighting it costs more than paying it here is how you pay:

Step 1: Log into the GST portal at gst.gov.in

Step 2: Go to Services → User Services → View Notices and Orders

Step 3: Find your DRC-07 order. Click View.

Step 4: Click Payment towards demand to pay through the Electronic Cash Ledger.

Step 5: Pay the full amount tax + interest + penalty. Note: you cannot use ITC balance to pay interest and penalty. Those must be paid in cash.

Important: If you pay within 30 days of the DRC-07 order date and the case is under Section 73 (non-fraud), the penalty is often reduced to 10% of the tax amount. After 30 days, full penalty applies.

💡 Calculate your exact late fee and penalty before paying using the SmartGST GST Penalty Calculator.

Option 2: File an Appeal (If You Disagree With the Demand)

If you believe the demand is wrong wrong calculation, duplicate demand, ITC mismatch due to vendor error that has since been corrected you have the right to appeal.

Where to appeal: First Appellate Authority (Joint/Additional Commissioner of GST Appeals)

Time limit: 3 months from the date of the DRC-07 order. A 1-month extension can be granted in genuine cases.

Pre-deposit required: You must deposit 10% of the disputed tax amount before the appeal is admitted. This is non-negotiable.

Step 1: Go to Services → User Services → My Applications → New Application → Appeal to Appellate Authority

Step 2: Fill Form GST APL-01 with full details of your grounds of appeal

Step 3: Attach supporting documents reconciliation statements, corrected returns, vendor confirmations, purchase registers, invoices

Step 4: Pay the 10% pre-deposit through the cash ledger

Step 5: Submit with DSC or EVC

The Appellate Authority must pass an order within 1 year of filing your appeal.

⚠️ If you miss the 3-month appeal window, your options become severely limited. Do not wait.

How to Check Your DRC-07 Notice on the GST Portal Right Now

Many businesses are not even aware a DRC-07 has been issued against them. Here is how to check immediately:

Log into gst.gov.in with your credentials

Go to Services → User Services → View Notices and Orders

All notices and orders appear in descending date order

Look for any order of type DRC-07

Click View to see the full demand details

📅 Never miss a GST deadline again. Use the SmartGST Free Due Date Calendar to track all your GST return due dates in one place no signup required.

DRC-07 Under Section 73 vs Section 74 The Difference Matters

The section under which your DRC-07 is issued directly determines your penalty exposure:

Section 73 | Section 74 | |

|---|---|---|

Applies to | Non-fraud cases genuine errors, clerical mistakes, interpretation differences | Fraud, wilful misstatement, suppression of facts |

Penalty | 10% of tax demanded | Up to 100% of tax demanded |

Time limit for notice | 3 years from due date of annual return | 5 years from due date of annual return |

Reduced penalty window | Pay within 30 days of DRC-07: penalty stays at 10% | Pay before SCN: 15% penalty; before order: 25%; within 30 days of order: 50% |

From FY 2024-25 onwards, Section 74A has replaced both Sections 73 and 74 as a single unified provision with a 42-month notice period. If your DRC-07 relates to FY 2024-25 or later, check which section applies before calculating your liability.

5 Critical Mistakes to Avoid After Receiving DRC-07

Mistake 1: Waiting to "see what happens"

Nothing positive happens from waiting. Interest compounds daily and recovery proceedings begin at the 90-day mark.

Mistake 2: Paying without verifying the calculation

I have seen cases where the officer's interest calculation had errors. Always verify the numbers independently before paying. Use the SmartGST GST Interest Calculator to cross-check.

Mistake 3: Trying to respond informally

DRC-07 is a formal legal order. All responses must go through the GST portal. Phone calls and emails to the department have no legal standing.

Mistake 4: Missing the 30 days reduced penalty window

If you are going to pay, pay within 30 days of the order date. Beyond that, full penalty applies — that can be a meaningful amount on large demands.

Mistake 5: Filing an appeal without professional help on large demands

For demands above ₹5 lakh, always engage a CA or GST practitioner to draft the appeal. A poorly drafted appeal with missing documents gets dismissed and you lose your pre-deposit.

DRC-07 and the GST Notice Flow The Complete Picture

Understanding where DRC-07 sits in the full GST notice system helps you respond correctly:

Notice | Stage | What It Means |

|---|---|---|

ASMT-10 | Scrutiny | Department found discrepancy in your returns |

DRC-01 | Formal demand proposed, your reply invited | |

DRC-01A | Pre-SCN intimation | Informal intimation before SCN in some cases |

DRC-07 | Final Demand Order | Adjudication complete, demand confirmed |

DRC-08 | Rectification Order | Correction to an earlier order |

APL-01 | Appeal | Your challenge to the DRC-07 order |

📖 If you received a DRC-07 and want to understand the full GST notice system, read the SmartGST GST Late Fee and Penalty Complete Guide 2026 it covers every penalty scenario with real numbers.

Frequently Asked Questions

Q1. Is DRC-07 a final order or can it be modified?

DRC-07 is a final demand order. It can only be changed through a rectification application (for clerical errors in the order itself) or through an appeal. You cannot simply ask the officer to revise it informally.

Q2. Can I pay DRC-07 demand using my ITC balance?

You can use ITC to pay the tax portion of the demand. But interest and penalty must be paid in cash only ITC cannot be used for these components. This catches many businesses off guard.

Q3. What is the time limit to respond to DRC-07?

You have 3 months from the date of the order to file an appeal. For payment with reduced penalty under Section 73, the window is 30 days from the order date. Do not confuse the two timelines.

Q4. What if I partially agree with the DRC-07 demand?

You can pay the undisputed portion immediately (to stop interest on that amount) and file an appeal for the disputed portion. The 10% pre-deposit for appeal is calculated only on the disputed amount.

Q5. Can the department issue DRC-07 without issuing DRC-01 first?

Generally no Section 73/74 mandates a show cause notice before a demand order. However, in summary assessment cases under Section 64, or where the taxpayer fails to appear after due notice, the officer can proceed ex parte and issue DRC-07 without a formal hearing.

Q6. What happens to my GSTIN after DRC-07?

A DRC-07 alone does not cancel your GSTIN. But if you ignore it and recovery proceedings escalate, the department can cancel your registration under Section 29 as part of broader enforcement action.

Q7. I received DRC-07 for FY 2018-19. Is it time-barred?

Demands under Section 73 for non-fraud cases must be issued within 3 years of the due date of the annual return for that year. For FY 2018-19, the GSTR-9 due date was December 31, 2019. Three years from that = December 31, 2022. If the DRC-07 is dated after that, you have a strong time-bar argument in your appeal. Get professional advice immediately.

Q8. Can I check GST demand status online?

Yes. Log into the GST portal → Services → User Services → View Notices and Orders. All demand orders including DRC-07 appear here with current status.

The Bottom Line

DRC-07 is serious but it is manageable if you act within the timelines.

If you agree with the demand: Pay within 30 days of the order date to keep the penalty at minimum. Use cash for interest and penalty components.

If you disagree with the demand: File an appeal within 3 months with a 10% pre-deposit and solid documentation. Do not miss this window.

If the demand is large (above ₹5 lakh): Do not handle this alone. Engage a CA or GST practitioner immediately.

The worst thing you can do is nothing. Every day you wait costs you more money and fewer options.

🛠️ Tools You Need Right Now:

GSTIN Validator → Verify any GSTIN before making payments

GST Interest Calculator → Calculate exact interest on your demand

GST Penalty Calculator→ Know your exact penalty before paying

GST deadline → Track all your GST notices in one place

GSTR-2B Reconciliation Tool → Reconcile ITC to avoid future DRC-07s

This article is for informational purposes only and does not constitute legal advice. For demands above ₹5 lakh or complex cases, consult a qualified CA or GST practitioner.

Last updated: April 2026 | Sources: CGST Act 2017, CBIC Circulars, GST Portal Official Documentation